The Critical Path is the plot over time of how much capital clients need that will permit them to achieve a must-achieve objective. (See chart 1.) The discount rate to use for plotting the Critical Path is that which is available on riskless investments. Where the client's portfolio is versus the Critical Path determines whether they can take risk in their portfolio. On or below the Critical Path only riskless investments should be used. Most advisors and investors don't follow this guidance. In 2008 there were probably millions of investors that were on or below the Critical Path and inappropriately were using risky portfolios. After incurring portfolio losses, they were forced into making undesirable changes in their life plans.

Investing in riskless investments is unappealing to many. Financial advisors can use the concept of the Critical Path to convince their clients to change their basic financial plans (e.g. how much they save, or how much retirement income they must have.) to effectively move them above the Critical Path and free themselves from the constraint of investing only in riskless investments.

Investment Implications Of Being Above, On Or Below The Critical Path

Investors who are above the Critical Path have tremendous flexibility. They can structure their portfolios using the wide variety of investment vehicles available to strive to achieve better than riskless returns. This is traditional investing to most.

If somebody is on or below the Critical Path, they are very constrained. They should invest at the riskless rate. To do otherwise means they are taking a course of action that risks not achieving a goal that they said was absolute and can not be compromised. There should be no ifs, buts or maybes. If they invest in a "normal" way, they risk underperforming the guaranteed rate, and not achieving their must-achieve objectives. If they are below the Critical Path, they risk digging themselves into a deeper hole. Many individuals, pension plans, and states are likely below the Critical Path, but none the less are investing in risky investments. They eventually could be forced to painfully change their objectives.

What strategies are available to an investor that is above the Critical Path? There are many but there should be one over-riding goal: to stay well above the Critical Path. Do not come close to the Critical Path with its severe investment restraints.

One investment strategy is to allocate enough to conservative investments to assure accomplishing critical needs regardless of how badly the rest of the portfolio does. Investing in bonds is the traditional approach. Once their critical needs are covered, investors are then in a position to invest the rest (or surplus) in a riskier manner, and to strive for higher returns. The strategy can be handled with two separate portfolios, or treated as one but with sufficient conservative investments to always assure critical needs will be provided for.

Another, but less reliable approach is to invest aggressively for higher returns, but plan to quickly restructure the portfolio to be more conservative should it lose value and begin to approach the Critical Path. This smacks of market timing. It is of course questionable whether an investor will be capable of taking this action when the need arises. Additionally, making a portfolio more conservative as it drops in value is counter to the traditional practice of periodic rebalancing to maintain the asset allocation. Rebalancing holds the portfolio risk (expected volatility) constant as the portfolio drops in value and is not consistent with the goal of making it more conservative to prevent it from approaching the Critical Path.

A third approach is to use a single balanced portfolio and limit the risk so there is little likelihood of ever approaching the Critical Path. This may be the best approach.

The benefits for staying above the Critical Path are so large that individuals should consider changing their basic financial plans as a way to get above the Critical Path. This may include changing their savings' rate, planning for a later retirement, or setting a lower minimum amount to live on in retirement. All of these move them upward versus the Critical Path and give them a greater margin of safety so they can invest in investments with potentially higher returns. Helping someone think through these options is a key role for financial advisors. The Critical Path is a good tool for stimulating such a conversation.

What strategies are available to someone on or below the Critical Path?

If they are not willing to change their objectives, they have no choice but to invest at the riskless rate. To invest in risky investments risks not achieving their must-achieve objectives, or if they are below the Critical Path, possibly becoming even worse off. For many who have been trained to use traditional investments, shifting to low returning, riskless investment may be challenging.

If they are willing to change their basic financial plans so as to move above the Critical Path, they can invest in risky investments and seek higher returns. Once again, this may mean convincing them to increase savings (spend less), retire later, or in retirement lower their standard of living. Making these changes gives them the ability to strive for a higher standard of living by investing in potentially higher returning investment. These are all changes financial planners already may be trying to convince their clients to undertake. Explaining the Critical Path may make this job easier.

Implications In Retirement

Where somebody is versus the Critical Path is probably more important in the distribution phase than the accumulation phase because most retirees have limited ways to recover if they drop to or below it.

One option to move up versus the Critical Path is to increase the size of the assets. For a retiree this is hard to do. Other than going back to work, winning the lottery or receiving a large inheritance later in life, flexibility is restricted.

A more practical option to lower the Critical Path is to reduce mandatory retirement expenses. This can be done by making some mandatory expenses discretionary. Examples are entertainment, vacations or gifts. The benefits of doing this are large. Lowering one's base living standard, or being willing to make discretionary certain expenditures, lowers the Critical Path and gives the retiree significant investment flexibility.

A third option to lower the Critical Path, and this is unique to retirement, is to transfer longevity risk to another party. This is an important option that many planners probably do not consider. Making sure a retiree always has enough money against the risk of living too long (e.g. living to age 90 or longer) ties up a lot of resources. The solution is to buy an immediate annuity or similar product from an insurance company that assumes the longevity risk. Purchasing such a product increases the cash distributions versus what an individual can achieve when self-insuring. Because of the higher payout rates from the immediate annuity, the Critical Path will drop more than the reduced value of the portfolio resulting from purchasing the immediate annuity. The net effect is to move upward versus the Critical Path.

Buying an immediate annuity can produce dramatic benefits. Retirees who are below the Critical Path may be able to move up versus the Critical Path when they receive guaranteed lifetime income. This becomes a nice safety net. Retirees who move above the Critical Path can invest to seek higher returns, and if successful, increase retirement income, a wonderful outcome.

How Does Length Of Time Before The Money Is Needed Affect The Investment Strategy?

The shorter the time, the more certain we are that we know the various parameters required to define the Critical Path. Therefore the Critical Path is likely to be more important for short planning periods and less meaningful for long planning periods. If wrong, with long lead times, there is more time to adjust (including changing objectives) and catch up. The must-achieve objectives may not be so absolute when planning for retirement. The Critical Path for a 35 year old may not be very meaningful, but it is likely to be very important for someone ten or five years from retirement. Other things being equal, the 35 year old's portfolio can be more aggressive (unconstrained by the Critical Path) than the individual with 10 years before retirement. No surprise here.

Charting The Critical Path

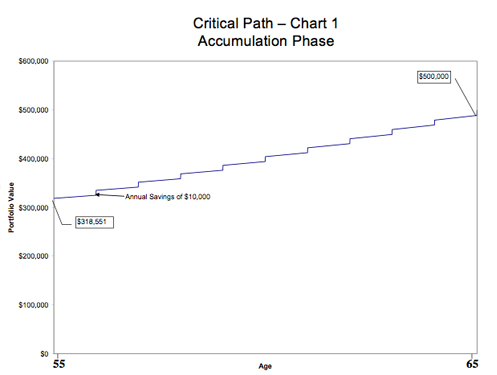

The Critical Path in the accumulation phase is upward sloping as assets grow. Here is an example of the calculation for the Critical Path for individuals in the accumulation phase when they are saving for retirement. You determine a client must have $500,000 in retirement in order to provide their minimum retirement income. They are sure they will save $10,000 per year for the next ten years. The riskless return is assumed to be 2%, which presumably is available through investment vehicles such as TIPs, other government bonds, or guaranteed annuities. Using net present value formulas you calculate $318,551 is needed today (plus their annual savings of $10,000) to grow to the $500,000 that can then provide their minimum retirement needs. The Critical Path from now till age 65 is graphed below.

If ten years before retirement, their financial assets are currently $318,551, they are on the Critical Path and should be able to achieve their critical goal if they invest at the riskless rate. They have no flexibility to take any risk for if they underperform they will not achieve their must achieve retirement objective. They can not save less than $10,000 a year. They can not earn less than 2%. They need to invest following the most conservative investment strategy and receive the 2% riskless return. This all assumes the objective must be achieved.

Each year one can update this Critical Path and determine where one is versus the Critical Path.

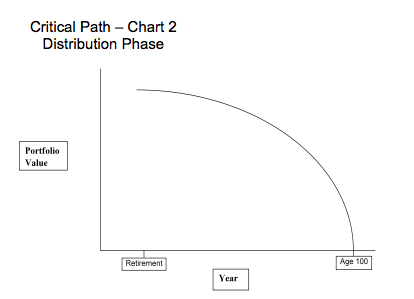

In retirement the Critical Path typically is a downward sloping curve as assets are consumed. This is shown in Chart 2. To calculate the Critical Path for a retiree, you must first determine essential retirement expenses. Then using a riskless interest rate, calculate the capital (NPV calculations) that is needed to provide the income to cover these expenses for a period of time that represents the longest they are most likely to live (e.g. age 100, not life expectancy, unless you want half your clients to run out of money). As the client grows older and life expectancy is shorter, less capital is needed and the line declines to zero. Having calculated the Critical Path, you can determine where somebody is versus the Critical Path and take appropriate action.

Investing using a riskless rate may be a hard concept to accept.

Advisors may question why someone should use an investment with a low, riskless return when over the long term a return from a risky investment is typically much higher. The answer is the higher long-term returns are not assured or guaranteed and the investor's objective by definition must be achieved. If this is the case and they are on or below the Critical Path, they have no choice but to invest at the riskless rate. It is an axiom in constructing the Critical Path. If the client says they are willing to take some risk to achieve an objective, then this is not a must-achieve objective and the Critical Path does not apply.

I suspect many advisors will have trouble accepting the concept that they should use a riskless investment. We have all seen illustrations for the efficient frontier that show a portfolio that is 75% in bonds and 25% in stocks should have a higher return with less volatility than a portfolio made up of 100% bonds. This implies taking risk pays off. Unfortunately, these are projections, risks remain, and the projections do not guarantee that the clients' must-achieve objectives will be met. This also implies "Risk" means portfolio volatility and not loss of capital (see insert).

Advisors may also argue that historically they personally have gotten better returns than the riskless rates and therefore the client need not use a low returning, riskless investment. However, risk remains and advisors can not and should not personally guarantee the higher return. The objective, by definition, can not be compromised and this means riskless investments are the only option.

The Critical Path should be thought of as a theoretical concept. In the real world, many of the parameters (for example objectives and rates of returns for risk-free investments) cannot be precisely and unequivocally determined. When faced with undesirable choices, a person may change their objectives. For example, a future retiree may say they must have $50,000 of income at age 65, but when told this will require saving more today or accept a guaranteed low 2 percent return on their portfolio, they may say they are willing instead to accept $30,000 as a floor. The lower number then defines the Critical Path.

Characteristics Of A Riskless Investment

A riskless investment is one guaranteed by a third party who is an absolutely reliable party. They may be guaranteeing:

Returns to some future date

Cash payments for a specified period of time

Cash payments for a lifetime to protect against outliving one's resources (longevity risk).

Protection against inflation

The guaranteed returns will be low because the organization making the guarantee does not want to be in position to lose capital and possibly risk its own survival. They may be hedging their position in the open market. In this paper I use a hypothetical 2 percent as the riskless rate. The actual rate fluctuates with market.

I recognize there really are no 100 percent reliable guarantees, and therefore there are no truly riskless investments. The areas where risk will always remain, even if we call it riskless, include:

Counter party risk, even when sovereign governments are involved

Future buying power for a specific individual.

The inability to receive absolutely risk free guarantees does not negate the benefits of the Critical Path concept. Just ask the millions who shouldn't have owned risky portfolios in 2008 and now can't retire as planned.

Modern Portfolio Theory May Not Apply To Individuals On The Critical Path

Since many individuals are on or below the Critical Path and should invest using a riskless rate, the appropriateness of all investors using Modern Portfolio Theory and models, such as Monte Carlo, to help structure portfolios is questionable. The expected outcomes of these models are based on probabilities, and typically the impact of tail events are assumed to be inconsequential. Individuals on or below the Critical Path should seek riskless returns and probably should not use advice based on these models. Recognition that some investors should be using riskless investments may require a major change in industry practices because many financial advisors and most financial institutions provide investment guidance without regard to where the investors are versus the Critical Path. There are probably large numbers of individuals on or below the Critical Path so this is not a trivial matter.

Conclusion

The Critical Path is introduced as a tool that advisors can use with clients to discuss the importance of risk capacity. Individuals on or below the Critical Path have no capacity to take risk. They should invest using riskless investments. To do otherwise means they are taking a chance of not reaching a must-achieve objective. Knowing they should use only riskless, low returning investments may provide an incentive for many investors to change their financial plans -- save more, plan to retire later, require less income in retirement -- any of which may raise them above the Critical Path and permit them to invest in a way to seek higher returns.

Sidebar

Understanding Risk

The events of the last several years are encouraging financial advisors to be sure they fully understand risk. Risk can be looked at in several different ways. One is to differentiate between risk tolerance and risk capacity. Most advisors and investors focus on risk tolerance; e.g. "Can an investor sleep at night if the portfolio drops 20%?" Risk capacity, on the other hand, is the ability to sustain a loss and still achieve key objectives, such as retiring at age 65 with sufficient income. Risk capacity is not a new concept. It just has not received the attention it deserves.

That which is most limiting, their risk capacity or risk tolerance, should determine the portfolio's construction. For someone coming upon retirement with a shortage of capital, risk capacity typically is the limiting factor. For the wealthy eighty year old with a large portfolio, but living an inexpensive life and afraid to see her portfolio drop at all, risk tolerance is the limiting factor. I believe the majority of investors have designed their portfolios around risk tolerance, not risk capacity, and this focus contributed to much of the damage they sustained over the last several years.

There is another way to look at risk. Risk can refer to either portfolio volatility or permanent loss of capital. Financial planners and investment specialists have been trained to consider risk to mean volatility (typically measured by standard deviation). The volatility definition is used in many professional journals and is behind much of the research. Apparently, this definition came into play with Modern Portfolio Theory. Eric Lonergan in his book, Money, points out that before the popularization of Modern Portfolio Theory, risk was considered to be the permanent loss of capital, not volatility.* For many investors, loss of capital, which relates to risk capacity, is what is important.

*Lonergan, Eric 2009 "Money", Acumen Publishing Limited, p 98-105.

Robert Kreitler, CFP, manages a New Haven, Conn., branch office of Raymond James Financial Services Inc. He spearheaded an effort with Ibbotson Associates and the FPA to create the "National Savings Rate Guidelines." He has written numerous articles on retirement planning and is the author of Getting Started in Global Investing, a John Wiley book that introduces the Island Principle. He is a regular guest on Connecticut Public Radio's "Faith Middleton Show.