The end of U.S. dollar dominance may be unfolding in front of our eyes. No, we don't think China's ascent is the key threat; instead, key to understanding the U.S. dollar may be to understand the money market fund you might hold. Let me explain what's unfolding in front of our eyes, and what it might mean for the U.S. dollar and global markets.

Typically, when we think about potential threats to the dollar, we think a different reserve currency might take over; or that foreigners might dump their dollar holdings. I will touch on these, but then dive into what may be a much bigger elephant in the room. Bear with me.

Foreigners holding U.S. debt

Yes, foreigners hold trillions in U.S. debt, and if they were to dump all their debt, borrowing cost in the U.S. might rise. Except it hasn't happened: in our analysis, as foreigners have been selling U.S. Treasuries, the dollar has neither plunged, nor have U.S. borrowing costs skyrocketed. Why is that? As we will discuss below, we believe, in the short-term, other market forces have been even stronger.

.jpg)

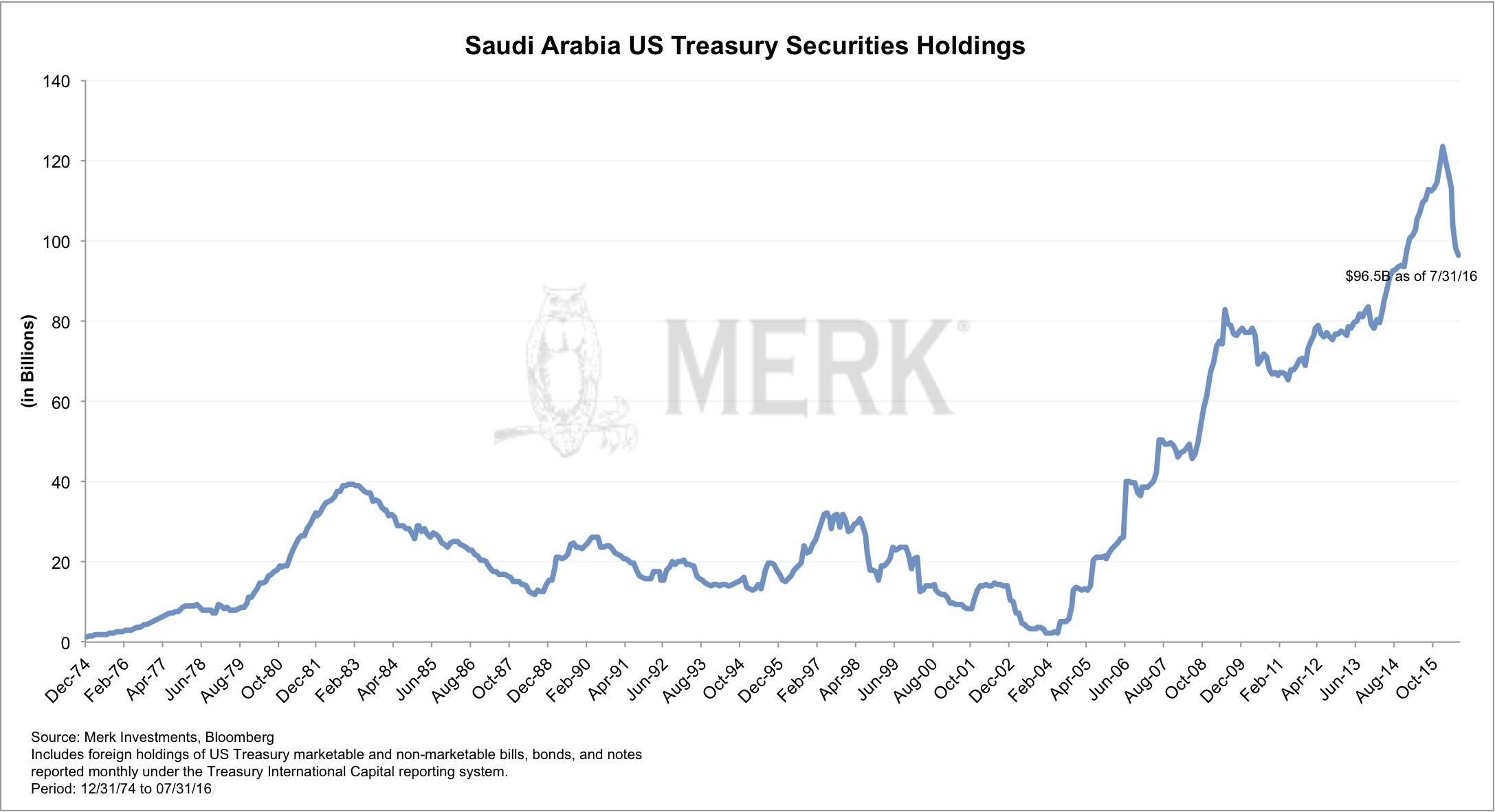

That said, the recent decision by Congress to override President Obama's veto to allow private citizens to sue Saudi Arabia should get our attention. Saudi Arabia has threatened to sell its U.S. assets in case this law passes, as it doesn't want a judge to freeze their assets. As this chart below shows, this may not be an empty threat:

I write "may be" because there might be other reasons for the Saudis to sell U.S. Treasuries, such as a need to raise cash to deal with the fiscal challenges that have resulted from lower oil prices.

Some say the inclusion of China's currency into the official basket of reserve currencies (SDRs) by the International Monetary Fund (IMF) is a clear sign that we have the beginning of the end of dollar dominance. In our assessment, this change is mostly symbolic. First of all, the new SDR basket barely changes the U.S. dollar weighting (other currencies were reduced to make space for the yuan); second, no large country manages its reserves according to the formula provided by the SDR; instead we allege that they manage them according to what they believe to be in their perceived self-interest. Where SDRs come into play is when the IMF provides a loan, as those are typically denominated in SDR. A belief in this theory suggests a great belief in the power of the IMF, an institution that has, ever since its inception, looked for reasons to be relevant. I'm not trying to discredit this theory, but am a firm believer that market forces playing out may well overwhelm the bureaucrats at the IMF for a long time.

It turns out, though, that those that predict the end of the dollar dominance might still be right; not because of the IMF, though, but because of what we believe are massive changes underway in how anyone from foreign governments to foreign banks to foreign and domestic corporations fund themselves.

Understanding Money Market Funds

At the peak of the Eurozone debt crisis in 2011, we cautioned that U.S. investors weren't immune from potential fallouts because prime money market funds, i.e. the typical money market fund that doesn't exclusively invest in U.S. government securities, at the time had incredible exposure to European banks. It turns out European banks historically have had great funding needs in U.S. dollars because they extended U.S. dollar denominated loans in emerging markets, amongst others. At the time, we calculated that the average prime money market fund had half of its investment in U.S. dollar denominated commercial paper issued by (often weak) European banks; our analysis showed one money market fund of a major brokerage firm had 75% of its holdings in such paper. We weren't the only ones warning about this, and, within months, we gauged that the overall quality of investments held by money market funds improved. Sure enough, though, "everyone" appears to be chasing yield, and your money market fund portfolio manager may not have been immune from it, either.

It turns out that this month, new rules for certain money market funds are being phased in. The regulations focus on institutional money market funds - you might not hold them in your retail brokerage account, but could be invested in one through your 401(k) plan. The new rules make it far less attractive for money market funds to invest in anything that's not U.S. government paper. Amongst others, institutional money market funds that invest in securities other than U.S. government paper must have a floating Net Asset Value rather than a fixed value of $1; they also must caution investors that their money might be held hostage for a few days in case of a panic in the market. Aside from a shift on how portfolio managers manage money market funds, investors are also thinking twice whether it's worthwhile to stuff money into money market funds when the returns are near zero, yet the risks are now higher (a floating NAV is riskier than a fixed one; so is the potential inability to withdraw money) than they used to be.