In the wake of economic pressures on financial advisory practices, some have chosen to dramatically downsize their firms, opting to fire staff, work without an office or even give up certain types of clients. While it seems to be a drastic move, some advisors have made a choice to be a mobile advisor. The question remains, though: Is this a viable business model or simply a reactionary trend?

To better understand what is meant by the term "mobile advisor," let's explore a definition. In the earlier days of the financial service profession, mobile advisors were the norm. Typically, the advisor would have a "kit" consisting of forms needed to transact business, service accounts and prospect for new clients. Additionally, they might have a box filled with brochures, prospectuses and the like. These might be kept in the trunk of a car. Then the advisor would travel to his or her client's home, place of business, etc. to conduct business, occasionally needing to step out to the trunk of the car to retrieve a needed form. It is likely that some of you reading this column may have, at one point or another, worked your practice in this way.

But with the introduction of computers, many more investment and other service offerings, the trend moved toward a professional office environment for those client and prospect meetings. It no longer was possible to carry around all the forms that would be needed, much less all the prospectuses, etc. Thus, more efficient means of doing business needed to be implemented. However, with those more efficient means came more expensive ways of managing a practice.

Office expenses, including staff expense, office space, equipment costs, advertising and other costs can quickly spiral out of control. So it makes sense to look at ways to reduce or perhaps share expenses.

The mobile advisor business model suggests that cost-cutting is taken to a new level by eliminating staff and office space, opting for a true "mobile" operation. To accomplish this successfully, some hard choices may need to be made.

One of those hard choices may require a reduction or elimination of staff. Turning to virtual assistant programs or retaining some staff in remote work environments (working out of the home, for instance) could be the realistic alternative. Some advisors have chosen to use virtual back office services to further cut down on staff needs.

The mobile advisor may also choose to eliminate conventional office space, opting for a virtual or executive office (temporary) as a suitable alternative. In this environment, the advisor could choose to use only a meeting or conference room space on an as-needed basis, rather than pay high monthly rent on office space. In this scenario, the advisor would most likely be doing his or her back office work out of the home.

Other hard choices involve deciding whom to keep as a client. Performing some analytics on a client base could prove helpful in determining this. In essence, what the advisor needs to do is determine who his clients need to be from a profit standpoint, given the new mobile business model.

To determine this, creating a metric that measures client profitability would be a good start. Given that there are always going to be exceptions to the rule (i.e., taking on a relative of a rich client as a favor, etc.), for the most part being able to identify your core group of clients from a profitability standpoint and then designing a fee and other pricing structures to best match up with that group could optimize the profitability of the practice and make the mobile advisor business model actually work.

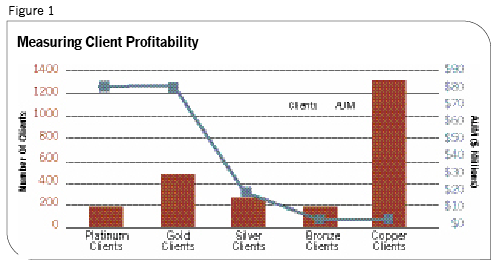

Looking at a typical analysis of a client base, we might see the following:

In the above example, this financial advisor has grouped clients into five different categories from Copper to Platinum, based on the size of assets managed for the clients (the green columns relate to the numbers on the left side of the chart, whereas the red line relates to the dollar amounts on the right side of the chart). In this example, we see that the clients with the lowest amount of AUM are actually in the largest group (Copper). This would suggest that most of the profit for the practice is coming from a relatively small group of clients in perhaps the top two categories (Platinum and Gold).

Thus, what this chart shows is an unbalanced practice with probably a lot of service work needed for a group of clients that do not produce much profit for the firm. In the above example, eliminating much of the lowest categories of clients might only cost the firm 10%-15% of its annual revenue, but potentially allow for substantial staff reductions and staff time in servicing the remaining accounts. It would also quite deftly set the stage for creating a mobile advisor business model, saving tens of thousands of dollars in monthly expenses while retaining most of the gross revenue of the firm. This translates into a much more profitable firm, as the net profitability by number and by percentage jumps substantially.

In the current world, the mobile advisor is again able to carry the forms and other material through the use of a laptop computer, a tablet computer or something similar. No longer does the advisor need to have a trunkload of forms and prospectuses. Depending on how the advisor works (and what her relationship with a broker/dealer or custodian might be), she may also be able to sign forms electronically, forgoing paper forms altogether.

On the one hand, it must be stated that this may not be the right move for everyone. This example presupposes that the firm is capable of letting go of a large number of unprofitable clients, which may not be possible, depending on the circumstances. If the firm, for instance, made its mark in the tax-sheltered annuity market (TSA), creating clients from the ranks of the teaching profession (as an example), then simply cutting out all clients with small accounts might do more harm than good. And while it might be technically possible to reduce expenses by cutting such clients, it could hurt the firm's credibility in that marketplace going forward.

On the other hand, there are always firms that carry a lot of smaller clients from way back when they got started. These clients, if they can't be cut, might be serviced by a junior advisor, if the firm was willing to go in that direction. Developing collaborative relationships with other advisors that might enjoy working with such clients is another option.

In a follow-up article, we will explore some advisors who have taken this step to be a mobile advisor. If you would like to be interviewed, please contact us at [email protected].

David L. Lawrence, RFC, ChFE, AIF, is a practice efficiency consultant and is president of EfficientPractice.com, a practice consulting firm based in San Diego, Calif. (www.efficientpractice.com). The Efficient Practice offers an advisor network and a monthly newsletter.