Executive Summary

This paper is intended to help advisors better serve their clients by opening a new dialogue about replacing the conventional investment approaches that have failed clients.

Now is the time for advisors and investors to rethink conventional buy and hold-growth stock focused approaches. The advisory and investment management community is struggling to let go of the conventional investment wisdom that is so deeply ingrained into our investment psyche. The first step is to accept the insanity of continuing to follow the same course while hoping for a better outcome in the future. What is required now are new investment approaches that help investors capture a more consistent return while also seeking to protect the capital invested in volatile securities. One of the first things we learn as advisors is the importance of the present value of a dollar or having the largest capital base possible working for you at all times. Yet the passive "buy-and-hold" approach inherently disregards the capital destruction caused by negative market cycles.

Unfortunately we know today after three decades of experience that investors don't really buy and hold and recent investor behavior underscores the fallacy of continuing to sell clients on this flawed idea. Investment approaches need to embrace a more active and responsive risk-managed investment approach that seeks to protect capital by controlling losses during negative market cycles providing a more efficient and consistent means of building investment wealth. Most importantly by controlling risk and loss we can help investors stay invested so they have the opportunity to earn the higher historic returns that investing has offered over long periods.

A careful review of the market return dynamics strongly suggest that dividend-paying stocks, not growth stocks, should be the building blocks of the portfolio construction process. Without dividends the return from price appreciation simply won't get the job done for investors, market history reveals that the return from growth in share price appreciation alone does not justify investing in volatile equities. Furthermore the persistent cash flow from dividends can help wary investors stay invested through good and bad market cycles. In addition to the contribution to total return, automatic dividend reinvesting unleashes the benefits of compounding and dollar cost averaging. This type of plan forces investors to buy low, something they rarely do on their own. "Just ask yourself how many clients were buying stocks in March of 2009 when it looked like the world was going to end?"

A recent Standard and Poors (S&P) study not only sheds light on the flaws in conventional growthfocused investment approaches, but also provides insight on dramatic benefits that dividends can provide.

The January 2010 issue of S&P Research Insight highlights the tremendous benefits of compounding with dividends. Excluding dividends, $1.00 invested in the S&P 500 index on January 1, 1930, would have grown to $49 by the end of 2009. Over the same time period, $1.00 invested with dividends reinvested would have dramatically increased value to $1,259.

To put the dramatic difference in perspective, $10,000 invested would have grown to $490,000 through price appreciation, but with dividends reinvested, it would have grown to $12,590,000 over the 79-year period.

As many clients are rethinking relationships with advisors, it becomes even more relevant to point out the need for new investment approaches that can work in both good and bad market cycles. This paper will reveal the flaws in today's conventional investment approaches and the real effect that continued failure can have on our practices and clients' most pressing needs.

A discussion like this is long overdue. It is the beginning of a new conversation about keeping Americans' wealth secure by finding a better way to invest at a time when the risk of failure is compounded by a wide spectrum of new challenges.

The True Cost Of Failed Theory

For the last 30 years or so investment pros have told investors to create buy-and-hold passive asset allocation portfolios, focused on growth stocks, to obtain the highest returns over the long run, while ignoring short-term loss of capital. These concepts are based on the investment theory developed by academics during the 1950s, 1960s and 1970s. Unfortunately, many of these investment approaches have failed to deliver an acceptable outcome for investors. Everything seemed to work just fine from 1982 through 1999 as the greatest bull market in history provided unprecedented returns from price appreciation. However the real test of conventional approaches started in 2000 as market momentum turned ugly with a Bear Market of historic proportions. American investors lost more than 10 Trillion in wealth, not once but twice in just the last decade. As a result of attempting to follow conventional passive approaches many investors find themselves with severely diminished capital after years of saving carefully to secure a comfortable financial future. Many approaching retirement now face the unpleasant reality of never being able to retire. Plus a growing number of already retired investors find themselves without enough income to pay their bills and need to return to work.

How Did We Get Here?

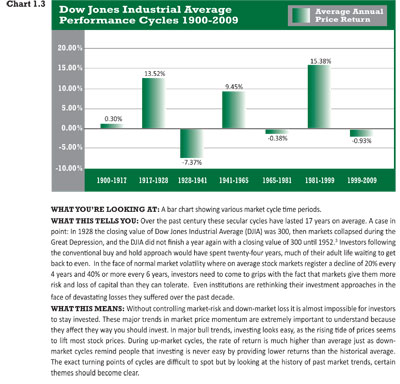

Extreme market events, like the Great Depression, tend to have significant influence on the development of subsequent investment theory. Harry Markowitz won a Nobel Prize in economic sciences in 1990 for his vast body of work covering nearly 40 years, including developing the basis for Modern Portfolio Theory (MPT), which focused on diversification of asset classes to reduce volatility and risk, while maximizing return. His greatest contribution was establishing a formal risk/return framework for investment decision-making. Markowitz gave investors a mathematical approach to asset-selection and portfolio management. He suggested that investors incorporate asset risk, return, correlation and diversification to determine the probable returns for an investment portfolio. By combining asset classes with low historical price correlation, he theorized a portfolio would have less volatility and provide higher average returns than with a collection of assets whose prices tend to behave in the same way (high correlation).1

Many other theories followed and built upon Markowitz's foundation. During the late 1960s and '70s the U.S. economy was in the grips of a recession, which deepened due to the Middle East Oil Embargo. Inflation was rampant even though economic output was falling. As you may imagine investors did not fair well as the U.S. Stock Market faltered along with the economy.

The 1973-74 bear market caused many investors who still had lingering memories of the Depression to bail on their mutual fund and stock positions. Hard hit by massive liquidations many mutual fund companies and money managers looked for new approaches to help

keep investors invested.

The Genesis Of Buy And Hold Investing

Academics went back to the drawing board in an attempt to find out why some investors failed while others seemed to win. They studied the approaches used by institutional pension fund managers. They noted that institutional managers focused more on a portfolios asset allocation model rather than the timing of buy and sell decisions. In their passive allocation approach, researchers found the majority of returns were determined by the allocation of assets, as Markowitz suggested.

Mutual Fund Company's embraced the passive allocation process as the solution to prevent individual investors from bailing during bear market trends. In the early 1980's their marketing campaigns strongly suggested that investors seek to replicate the passive institutional asset allocation approach by creating buy and hold portfolios.

Buy and hold theorists suggest that investors can't time the markets. By trying to avoid the down days they insist investors will miss the few major up days that provide most of the return. They believe the positive returns generated during market up-trends will always be sufficient to allow investors to not only recover lost capital, but to generate returns high enough to help them achieve their financial goals. But the devil is in the details, and as it turns out investors who follow the "buy and hold" mantra also expose their capital to the markets biggest losing days, which has an even greater effect on returns. At the time studies were conducted, there was also a very strong bias against active management due to the drag on performance caused by 4 Copyright © WBI Investments, Inc. 2010 the cost of executing trades. For decades stockbrokers made their income from the commissions charged for trading. At this time, the cost for an individual investor to make trades was approximately 1.0 - 1.5% of the total trade value, somewhat less for institutions. With a couple of buy's and sells in any year an active investor could find their trading costs eating up 4% or more of any return generated. However, today trading costs are not a material drag on performance. Competitive pressures from online Internet trading and discount brokers like Charles Schwab have reduced trading costs to a few cents or less per share.

Risk Really Does Matter!

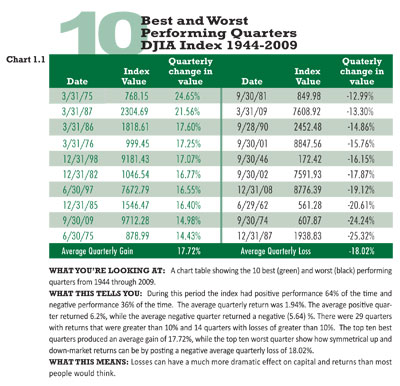

Conventional passive investment approaches were founded on the notion that if you missed the major upmarket days in an effort to reduce losses during down market cycles your performance would suffer. Our research indicates just the opposite. Returns can be magnified dramatically, not by capturing the best market days, but by avoiding the worst market declines. Prior best and worst return market studies have focused on the best or the worst 10 days to be invested in the markets over a long period of time. It seems almost laughable to focus on single day performance data. To my knowledge no one has a system that can reliably predict, much less capture returns for only the best or highest performing days. It's tough enough to spot an emerging trend that may take

weeks or months to develop and confirm.

Our best and worst performance analysis focuses on the 10 best- and worst-performing quarters for the Dow Jones Industrial Average index over the past 65 years.2

The Human Factor

Unfortunately we know today after three decades of experience that the assumption institutional investment approaches can be applied to individual investors is flawed. Individual investors are genetically predisposed to lose the buy-and-hold battle. When we invest, we all fight the "human factor," our survival instincts and emotions. These instincts were honed hunting for food to survive. If we encountered an animal that we could not fight off successfully we fled. Today we don't hunt for survival; we work and invest our savings to provide the things we need when we can no longer work.

Money in today's society is important to our basic survival and when account values fall due to declining markets our survival instincts kick in triggering a fear response. Individuals risk tolerances vary but fear will eventually trigger the need to "fight or flee". It's impossible to fight the "market" so the only course of action is to flee, which translates into selling low after money has been lost. Institutional fund managers often react differently to significant declines in account values because it's not their money. They also tie investment success to relative out performance against a benchmark. But relative performance to a benchmark holds little value to individual investors if their return is negative.

As the markets bottomed in March 9, 2009 the vast majority of investors had already moved to cash and were reluctant to believe that the risk to losing more capital had abated. Human nature and survival instincts will prevent investors from buying low when factors indicate that risk is still high. Instinct cautions investors to wait until conditions turn positive and markets have been rallying for some time before they invest. Unfortunately this completes the buy high-sell low cycle and sets them up to become bitterly disappointed once again as overvalued markets correct. After a decade of extreme market volatility, most investors are acutely aware that they really don't stay the course during severe market declines like we experienced from 2000 through 2002 and yet again in 2008. Not only do investors sell at or near market bottoms but they also sit on the sidelines missing the relief rallies that could have helped them recover lost capital.

It's Time For A Reality Check!

Unfortunately investors have had a brutal education trying to follow conventional buy and hold approaches through this 10-year secular bear market. One of the basic tenants of investing is to buy low and sell high, yet investors do the opposite as they buy and then sell low as volatile markets hand out more losses than they can stand. Now is the time for investors to back away from the conventional approaches they have been taught.

Why? Simply because they do not work! To be sure some of the conventional investment wisdom developed over the past three decades has merit. Every portfolio design should incorporate the fundamental principle of diversification as developed by Markowitz. However, it's been widely assumed diversification would sufficiently reduce risk and loss enough to enable investors to stay invested in down-market cycles. This may hold true in mild corrections but during the 2008's Financial Crisis asset values collapsed across the board and diversification failed to materially limit investor losses or prevent them from abandoning their investment plans.

Dividend Stock Performance in a Bear Market Cycle

In 1966, the markets moved into an underperformance cycle. At the time, the dividend yield on the DJIA was 3 percent-well below the historical average of 4.21 percent.4 The lower yield was a reflection of the inverse relationship yield has with stock price movements. As stock prices soared from 1941 through 1965, the yield on the DJIA fell. From 1966 through 1981, the economy and markets faltered as they were battered by a combination of rising interest rates and commodity prices. You may recall that the United States was in the grips of stagflation-an economic recession combined with soaring interest rates. The underperformance period that began in 1966 included the shocks of the 1970s. Investors had to cope with oil embargoes, gas lines, and falling stock prices. As if the grinding declines in the market and poor economic conditions weren't enough, at the same time the very fabric of our society was being tested by the political turmoil caused by the war in Vietnam.

This negative performance period turned out to be the second worst underperformance cycle of the 20th century. If you were invested in growth stocks that did not pay a dividend, you almost certainly lost money. But even during these very troubled times, companies did their best to keep their commitments to shareholders.

Surprisingly, the companies in the DJIA were actually able to increase dividend payouts by an average of 4.46 percent per year. If you had invested $100,000 in the DJIA Index in 1966, the value of your initial shares would have declined over 16 years to $90,275 by 1981.

Stock prices declined generating losses not gains. By reinvesting dividends, you would have acquired more shares at a time when prices were falling. Your reinvested dividends would have helped you accumulate additional shares worth $96,386, and your total account value would have increased to $186,661. If you had taken your dividends in cash instead of reinvesting, you would have received $64,978 in cash dividends over the period, and instead of losing almost $10,000 in value you would have netted almost $50,000.5

Dividend Stock Performance In A Bull Market Cycle

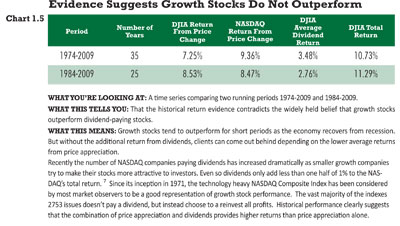

In contrast, let's look at how dividend-paying stocks perform during bull market cycles. One could argue that the period from 1982 through 1999 was an unusually good period for the economy and the markets. This nearly 17-year period provided the longest economic expansion and the greatest bull market in history. Stock market prices advanced from 875, the value of the DJIA at the start of 1982, to 11,497, its closing value in 1999.

But even during the great bull market, dividends played a major role in enhancing the already generous price appreciation returns. These tremendous returns from price appreciation caused many otherwise conservative dividend investors to abandon their tried-and-true strategy of investing in dividend stocks for the more glamorous growth stock sectors like technology and communications. This decision looked good for a while because these non-dividend growth stocks soared in value, outpacing the price appreciation of their dividend-paying counterparts. In 1999, the technologies-heavy NASDAQ Index advanced a whopping 85%, dwarfing the 25% advance in the DJIA. Many growth investors who forgot to factor risk into their investing equation were caught by surprise as the bull cycle faded in 2000.

But investors did not need to take more risk to get great returns; dividend-paying stock prices also increased, and their dividends enhanced the stunning returns from appreciation that the great bull market trend provided. If you had invested $100,000 in the DJIA during the great bull market from 1982 through 1999, the value of your original shares would have grown to $1,302,760 as a result of price appreciation, but with dividends reinvested the value would have been increased by an additional $753,348 to $2,056,109.

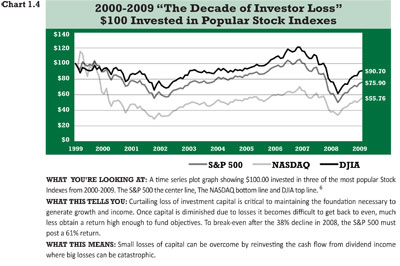

Investors experienced the benefits of dividends once again from 2000 - 2009 when the markets reverted to a negative price appreciation cycle. Even though the DJIA index performed dramatically better than the S&P 500 and NASDAQ an investor who held through this periods two bear market declines would have suffered a loss. Returns from price appreciation and dividends for the DJIA would have turned a $100,000 investment into $90,701. By comparison, the growth-oriented S&P 500 and NASDAQ would have turned $100,000 into $75,900 or $55,760. But here again dividends bailed investors out. By reinvesting dividends an investor would have unleashed the benefits of compounding and dollar cost averaging would have ended the period with $113,968.

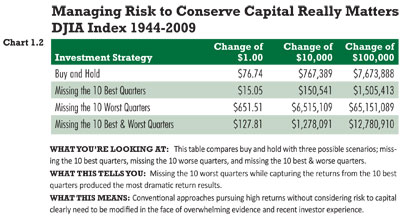

Control the Loss of Capital in Down-Market Cycles Basic math principals show that preventing a big loss of capital is more important than generating a big return. The conventional assumption that investors can ignore big losses is ridiculous. Over the last 10 years, conventional approaches have left investor "in the red," with less capital than they started with in 2000.

Do Growth Stocks Provide the Highest Returns?

In 1981 the U.S. Government created an arbitrary bias with investors for growth stocks when they lowered the tax on long-term capital gains in The Economic Recovery Act (ERTA). Since then, investors have focused on the tax breaks accorded to price appreciation rather than the historic evidence indicating that dividend paying stocks should be the foundation on which portfolios should be built. Growth companies choose to reinvest profits to expand the company and share price rather than distribute a percentage of profits to shareholders as dividends. Growth stocks, especially small companies, tend to outperform for a short period of time as the economy and markets recover from a recession. Moreover it has become widely accepted that growth stocks will persistently provide higher

returns even though statistical evidence contradicts that conclusion.

Use Market History To Develop A Better Way To Invest

The idea that you will "buy and hold" through any market decline secure in the knowledge that markets always recover as your portfolio value vanishes before your eyes is pure nonsense! This is evidenced by the rampant and dangerous "buy high, sell low" investor behavior over the past decade. But what if investors held stocks that provided return from two sources: price appreciation and dividends? Stock prices fluctuate; they always have and always will. While you may not be able to count on the return from stock price appreciation, you can bank on the return you will get from dividend payments. Dividends arrive every quarter, pretty much without fail. In addition, you do not have to sell the stock to get the dividend. Once received, the tangible dividend can be reinvested, used to diversify your investment position and risk, or used to support your lifestyle.

To clearly understand the dramatic benefits that dividends might have for us in the future, let's look at what an investor might have garnered in the past. With people living longer investors can look forward to 65 years of investing. We begin investing at about age 25 as we start to accumulate money from working. We save and invest for about forty years until we retire at age 65, and then we withdraw income for another 25 years to support our retirement lifestyle.

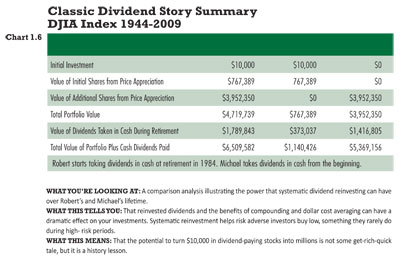

The Classic Dividend Story

The owner of a grocery store in New York City who saved most of what he made during his life, Joe was one of the fortunate people who came through the Depression with some cash. In 1944, he gave $10,000 to each of his 25-year-old twin sons, Robert and Michael. Though $10,000 was a princely sum in those days-almost enough to buy a modest home-his only proviso regarding the gift was that Robert and Michael not spend the money, but instead invest it against a rainy day.

It had been only a few years since the collapse of the stock market and many investors had lost everything. And, if that wasn't bad enough, we were fighting World War II.

Like everyone else, Robert and Michael didn't know where to invest the money. Their father suggested they buy big-name companies in the Dow Jones Industrial Average (DJIA) Index, those stocks that had survived the economic collapse. He also told his sons to let the dividends work for them by reinvesting them. In 1944, the DJIA offered a pretty generous dividend yield of 4.47 percent.8

Although Michael didn't spend the gift, he could not resist spending the dividend income his stocks provided in the first year. He had good intentions to reinvest his dividends in the future but always seemed to find a reason to spend them. Like a lot of people, Michael found that spending his dividends was easier than saving them. As the years went by, Michael enjoyed his lifestyle and the extra cash his dividends provided. His initial $10,000 investment continued to grow and by the end of 2009 it had reached $767,000, more than 76 times his initial investment! His dividends also continued to increase, providing him with more income to spend each year. The $483 in dividends that Michael received in his first year grew to more than $21,000 by 2009, providing him with 45 times more purchasing power! Amazingly, his stocks provided him with more than $370,000 in dividend income from 1944 through 2009!

The Effect Of Compounding And Dollar Cost Averaging With Dividends

Robert also took his Dad's suggestion and bought the companies that made up the DJIA, but unlike his brother Michael, he chose to follow his Dad's advice about reinvesting his dividends. He allowed his dividends to reinvest until he retired in 1984 when he needed his dividend income to help support his lifestyle.

By 2009, Robert's initial investment increased in value, just as Michael's had, to $767,000, but the additional shares he bought by reinvesting his dividends grew in value to more than $4.7 million.

Almost $5 million simply by letting his dividends work for him, Robert's initial gift increased in value from $10,000 to a total of $6.5 million, more than 650 times his initial investment. His annual dividend income also soared from $492 to more than $132,000! Since 1984 he has collected more than $1.7 million in dividends from his stocks. Now that's inflation protection.

Two Powerful Investment Forces

By reinvesting his dividends Robert unleashed two powerful investment forces-compounding and dollar-cost averaging-to build his wealth. Compounding builds your shares as dividends are reinvested to buy more shares each quarter. As the number of shares

increase, so does the dividend, which drives your share balance higher. Dollar cost averaging is the practice of systematically investing money (reinvested dividends) usually monthly or quarterly, over a long period of time.

Systematic investing leads to lowering the average purchase price of shares as stock prices fluctuate. When share prices are lower, you purchase more shares.

If you find these results almost unbelievable, join the club. Many people are still unaware of the benefits that dividend investing provides. And as good as this story may sound, it gets even better.

These results ignore the effect of taxes, but the 65 years covered by this story sported some of the highest income tax rates in history.

Taxes And Dividends

If we assume that Robert paid an average tax rate of 35% on his dividends, he would have paid almost $395,000 in taxes on his dividends.

He had to pay tax on his dividends even though he reinvested them. Michael had to pay tax on his dividends as he received them. As their dividends increased, so did their taxes. Although both came to love their dividend-paying stocks, they would always grumble at holiday parties about having to work just to pay the taxman. With the new lower tax rates on dividends under the Jobs and Growth Tax Relief Reconciliation Act of 2003 (JGTRRA), the highest tax rate is just 15%. This lower tax rate would have saved Robert more than $225,000 in taxes in our 65-year example. Robert and Michael are ecstatic about the reduction in tax on dividends that the new tax law provides! With taxes on dividends at historic lows many investors are wondering if dividends will continue to provide benefits in the future if the current administration chooses to raise taxes. Our 65-year history study illustrates the power of dividend returns even during the higher tax periods before 2003.

The benefits of dividend investing have been all but forgotten by many of today's growth-hungry investors. It's ironic that they equate dividend-paying stocks with the rocking chair set and miss out on a safe and reliable way to build wealth.

How Dividends Win Big in Both Bull and Bear Markets

Typically, dividend stocks fall much less than the overall equity market as investors flock to the safety net that dividends provide. During the recent 2000 through 2002 bear market, the DJIA, which is made up of large mature dividend-paying stocks, fell 37.85% while the more growth-oriented indexes like the NASDAQ and the S&P 500 fell 77.93% and 49.15%, respectively (from their highest closing values in 2000 to their lowest closing values in 2002).9

Both Robert and Michael were happy that their portfolios mirrored the DJIA instead of the more volatile indexes; an almost 38 percent decline in value was more than enough for them. Even with the declines, they felt lucky because their dividends provided them with additional return. Over the three-year bear market period, Michael collected almost $40,000 in dividend income, while Robert collected more than $250,000. Of course, Robert spent years reinvesting his dividends before the bear market started and Michael didn't. And even amid the financial crisis in 2008, they were both pleasantly surprised as the dividend-focused DJIA proved to be a less volatile bet, falling -33.84 percent, less than the more growth-oriented S&P 500 (-38.75%) and NASDAQ (-40.55%).10

Under just about any market conditions, history provides compelling evidence of the benefits of dividend-paying stocks, both for investors who are just starting out and for those already in retirement.

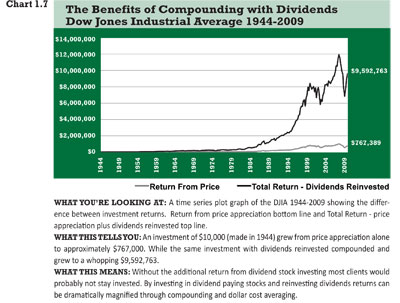

Without dividends, market performance would be truly disappointing. The return on the DJIA from price appreciation over the past century has averaged only 4.89 percent-certainly nothing to write home about.11

Not many investors would be excited about investing in stocks if they were to disregard the additional return from dividends. Yet in a bull market with inflated price appreciation, investors typically forget about the consistent return benefits from dividends.

With government deficits mounting and inflation looming rising dividend income streams will play a material role in helping the Baby Boom generation retire.

The combination of price appreciation and reinvested dividends promoting compounding and dollar-cost averaging can be a financial ally to investors with depleted capital accounts.

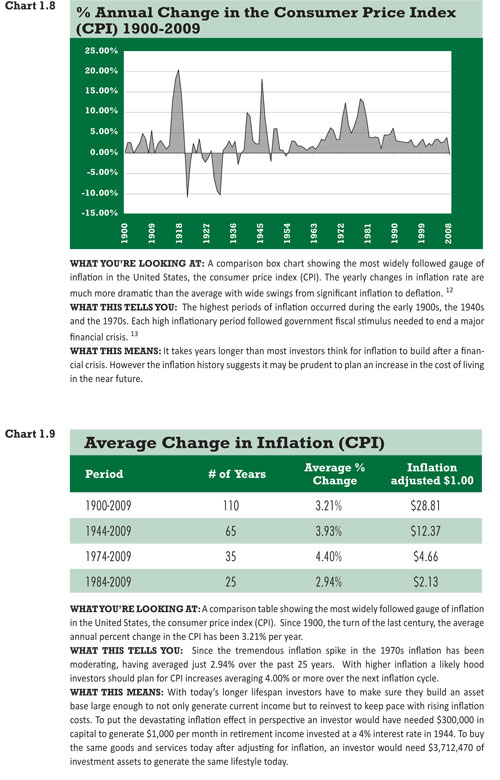

Inflation Is The Retired Investor's Greatest Enemy

Generating income in retirement to support lifestyle expenses is the primary objective for most investors. When we stop earning a living our investment assets need to provide income to supplement pension and social security payments. Inflation robs investors of their purchasing power as the cost of goods and services increase over time. If you live long enough, what once seemed like a princely sum can easily turn into a pauper's pittance as inflation causes prices to march relentlessly higher.

The Inflation Hurdle After a 10-Year Bear Market

The inflation hurdle seems daunting; especially after taking into account the serious capital losses that many investors have taken over the past decade. The challenge of helping these investors to build sufficient capital to generate the retirement income they crave seems almost insurmountable. Investing in equities to capture the higher returns offered through a combination of dividends and price appreciation is mandatory.

Dividend paying stocks offer retired investors two sources of inflation fighting protection. First, from price appreciation, (which can increase capital balances) and second, and more importantly, from rising dividend income streams as companies periodically increase dividend payments to shareholders to make their stock more attractive. When waging a battle against inflation, investors need to make sure that they are using the right tools. Over the past 65 years the 3.93% average inflation rate has been more than offset by the 6.29% average increase in cash dividends paid by Dow Jones Industrial Average Index companies. 14

Hope for Investors Building for Retirement:

For investors who have not yet retired dividends can also be reinvested to promote compounding and dollar cost averaging, dramatically increasing capital and the opportunity to enjoy a comfortable retirement.

Remember in our "Classic Dividend Story example; Robert started with a small $10,000 investment. The inflation adjusted equivalent today is just $123,000. So even with depleted account values investors still have a chance.

Robert reinvested his dividends for 40 years until his retirement in 1984 at age 65; he then started to take his quarterly dividends in cash to help support his lifestyle. His initial $10,000 investment in 1944 plus the $282,464 of reinvested quarterly dividends grew his capital base to more than $4.7 million by 2009. The cash dividends Robert received over 25 years of retirement totaled $1,790,000. Even more astounding is the fact that his initial $10,000 investment generated dividend income of $132,553 in 2009.

High Risk Growth Stock Systematic Withdrawal Plans Should Be Abandoned

During the 10-year bear market cycle, we witnessed the carnage inflicted upon scores of investors who were blinded by the illusion of easy gains during the 1990s Bull Market's spectacular run. They didn't fully appreciate the risk factors involved in chasing the high returns offered by growth stocks. Many of these investors were retired people who needed income to support their lifestyles,

yet they abandoned more conservative income - generating portfolios to get more growth.

They invested in growth stocks or funds and adopted systematic withdrawal plans to support their income needs. We call this process "dollar lost averaging" because it turns compounded growth into compound liquidation in negative market cycles and dollar cost averaging into a evil twin "dollar lost averaging" as more and more shares need to be sold at lower prices to fund income withdrawals.

During secular bear markets systematic withdrawal plans can cause investors to completely liquidate all of their capital to fund income before the next bull market begins. An investor who invested $100,000 in the growth stock focused NASDAQ in 2000; (the beginning of the current secular bear market trend) would have completely liquidated their account by January of 2009 by taking a 5% systematic withdrawal adjusted for 2.47% the average annual inflation rate for the period. Longterm bear market periods don't favor price appreciation and create the "dollar lost averaging" affect that leads to compound liquidation of investment capital. The S&P 500 Index faired only slightly better ending 2009 at $21,412, an 80% loss in value.15

Ideally retirement income solutions should be designed using a balanced blend of bonds and highyielding dividend paying stocks to generate interest and dividend income to support withdrawals. A balanced blend of 50% Dow Jones Corporate Bond Index and 50% S&P 500 stocks held up materially better at $75,710.

Portfolios should be managed to generate income to support lifestyle withdrawals while also attempting to control loss of capital in bear market cycles and prevent the dollar loss averaging effect. A lower risk balanced approach can give investors a chance to allow their account values to recover in the cyclical bull market rallies that follow bear market declines.

Quick-Read Summary

The investment industry has been using the wrong approaches to solve investors' problems. Instead of helping people, many advisors find themselves in the uncomfortable position of having put client's goals at risk using conventional investment approaches.

The training and education advisors received are mostly centered on the passive asset allocation approach.

Today many advisors find themselves bitterly disappointed with the conventional passive growth stock investment approaches they've been taught because they have not worked for the clients that they're trying to serve.

For the last 10 years investors have been buying high and selling low trying to use conventional approaches. That hasn't worked and they are looking for a better way to invest.

For the retired investors needing income they were told (conventional wisdom) to use a systematic withdrawal plan from growth funds. It was assumed that this approach would provide them with a higher level of current income and more growth of capital over time. However this approach also failed.

In order to get price appreciation your clients need a process that would have mitigated market volatility in order to help them stay invested. It's a very human problem. Human survival instincts are genetically hardwired to get out when the market drops, which is the central issues as to why investors always lose using the buy and hold approach to investing.

What has been missing is a focus on dividend paying stocks and a responsive methodology that would conserve capital as risk of capital loss increases in down market cycles. If you are ready to put aside the passive conventional approaches in light of its recent documented flaws, then please follow the recommendations in this next section.

Recommendations: Take Human Factor And The Emotion Out Of Investing

Now is the time for advisors and investors to re-think conventional buy and hold-growth stock approaches.

It's time to embrace dividend-paying stocks as the building blocks of the portfolio construction process.

Dividend-based portfolios can be expected to generate returns from price appreciation as well as from dividends.

Dividends provide a source of return independent of price appreciation, which can bolster portfolio performance even during bear market cycles.

A careful review of market history reveals that without dividends the return from price appreciation simply won't get the job done for investors. The persistent cash flow from dividends can help wary investors stay invested through good and bad market cycles. Dividend

payers not only tend to be less volatile in down market cycles, but the positive return from dividends is not dependent on price movements. In addition to the contribution to total return, dividend reinvesting automatically unleashes the benefits of compounding and dollar cost averaging. This type of plan forces investors to buy low, something they rarely do on their own.

Investors need to embrace a more active and responsive risk-managed approach that seeks to protect capital by controlling losses during negative market cycles. A strategy that can deliver downside protection in bear markets has the potential to build capital more consistently and to help investors stay invested. A larger invested capital base also enhances growth and income providing a more efficient and consistent means of expanding investment wealth.

New investment management approaches should incorporate a three-step process to help investors buy low and sell high by process.

First they should focus on value, which we define as buying stocks when they are cheap. Our experience indicates that normal price movements will take a stock's price from undervalued to overvalued and back to undervalued on average within 18 months. Instead of buy and hold we think its smart to attempt to buy low when the stock is cheap and then sell high after the stock has appreciated but before it falls again in value.

Second investors need to collect a significant cash flow return from dividends that is not dependent on price appreciation.

And third, investors should attempt to manage the risk to invested capital with a dynamic trailing stop-loss process to systematically harvest gains when available (sell high) while also attempting to limit losses during negative market cycles. In designing the management process care should be taken so that the stops and goals used result in an unemotional response to changes in risk at the individual security level and for changes in risk for the overall market.

Historical evidence supports the idea that investment capital is the engine of income and growth.

To be successful new investment approaches should attempt to capture returns during "up-market cycles", while limiting losses during "down-market cycles". A responsive risk managed strategy can deliver downside protection in bear markets, while having the potential to provide solid outperformance to conventional buy and hold strategies over long periods of time.

Don Schreiber, Jr., CFP

Chief Executive Officer and President

Don is also CEO and founder of WBI Investments, Inc. a money management firm offering unique riskmanaged portfolios focusing on value and dividends. Don is a member of WBI's Investment Committee. He is co-author of "All About Dividend Investing" released by McGraw Hill in December of 2005. The updated 2nd edition is due to be released August 2010.

Don is also the author of "Building a World-Class Financial Services Business: How to Transform Your Sales Practice into a Business Worth Millions" which was released by Dearborn Trade Publishing in July of 2001.

A popular speaker, Don is often called upon by the press to provide perspective on dividend investing and the investment markets. Don's media credits include major newspapers and magazines, as well as regular appearances on Bloomberg, CNBC and Fox News. Don attended Susquehanna University (Class of 1977) were he completed a Bachelor of Science Degree in Business with a major in Finance. He is a CERTIFIED FINANCIAL PLANNER practitioner since 1984, and is a member of the Financial Planning Association (FPA).

End Notes

1 Harry Max Markowitz research formed the foundation of Modern Portfolio Theory, from Wikipedia, http://en.wikipedia.org wiki Harry_Markowitz

2 Best and worst quarterly analysis, Dow Jones Industrial Average price return data source, 1944-2009: www.globalfinancialdata.com

3 Dow Jones Industrial Average Performance Cycle chart analysis, data source www.globalfinancialdata.com

4 Dow Jones Industrial Average historic average yield analysis since 1900, data source www.globalfinancialdata.com

5 Dow Jones Industrial Average return analysis form 1966-1981, data source www.globalfinancialdata.com

6 The Decade of Investor Loss chart analysis, data source for Dow Jones Industrial Average, S&P 500 and NASDAQ indexes Thomson Reuters Baseline

7 Evidence Suggest Growth Stocks Don't Outperform table analysis, NASDAQ Composite's current yield is .42%, data source www.nasdaq.com

8 Dow Jones Industrial Average yield in 1944, data source www.globalfinancialdata.com

9 Cyclical Bear Market Index returns 2000-2002, data source Thomson Reuters Baseline

10 Secular Bear Market Index returns 2000-2009, data source Thomson Reuters Baseline

11 Dow Jones Industrial Average price return analysis over the past century, data source www.globalfinancialdata.com

12 Dow Jones Industrial Average annual cash dividends 1944-2009 analysis, data source www.globalfinancialdata.com

13 Average change in the Consumer Price Index 1974-2009, data source U.S. Department Of Labor Bureau of Labor Statistics

14 Average change in the Consumer Price Index over the past 100 years, data source U.S. Department Of Labor Bureau of Labor Statistics

15 Systematic withdrawal "Dollar Lost Averaging" analysis for Indexes 2000-2009, data source Thomson Reuters Baseline