What should investors expect in the last quarter of the year? We see three themes that are likely to shape economies and markets in the months ahead as well as a number of key risks, as we write in our new Global Investment Outlook: Q4 2016.

1. Policy limits

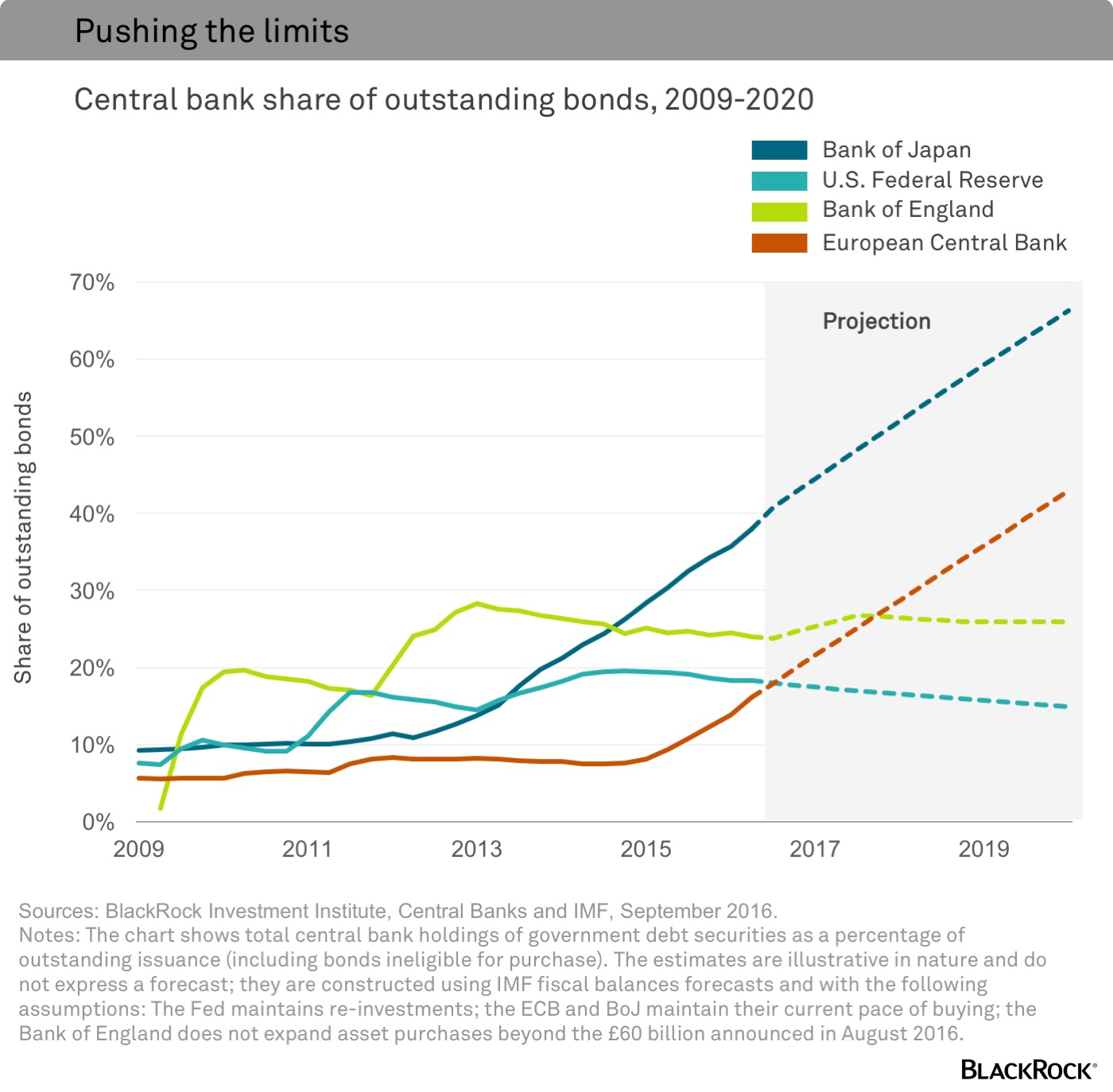

Central banks are nearing the limits of extraordinary monetary easing, as monetary policy is becoming less effective in boosting growth and additional easing measures may have diminishing returns—and unintended consequences.

We expect the U.S. Federal Reserve (Fed) to press on with slow interest rate increases, while other major central banks start to approach limits of their easy policies. The Bank of Japan, for example, already owns about 40% of Japanese government bonds (JGBs). At its current pace of buying, it would hold two-thirds of the JGBs by 2020, we estimate. See the chart below.

As monetary policy reaches its limits, some major economies appear on the verge of relying more on fiscal policy to boost growth. It is too soon to expect a big economic growth boost, but the change in tone could support risk sentiment. We see early signs of a regime change for market returns due to U.S. reflation, an end to deflation in China and a global pivot from monetary stimulus to fiscal support, even if the immediate economic impact is limited.

2. Low returns

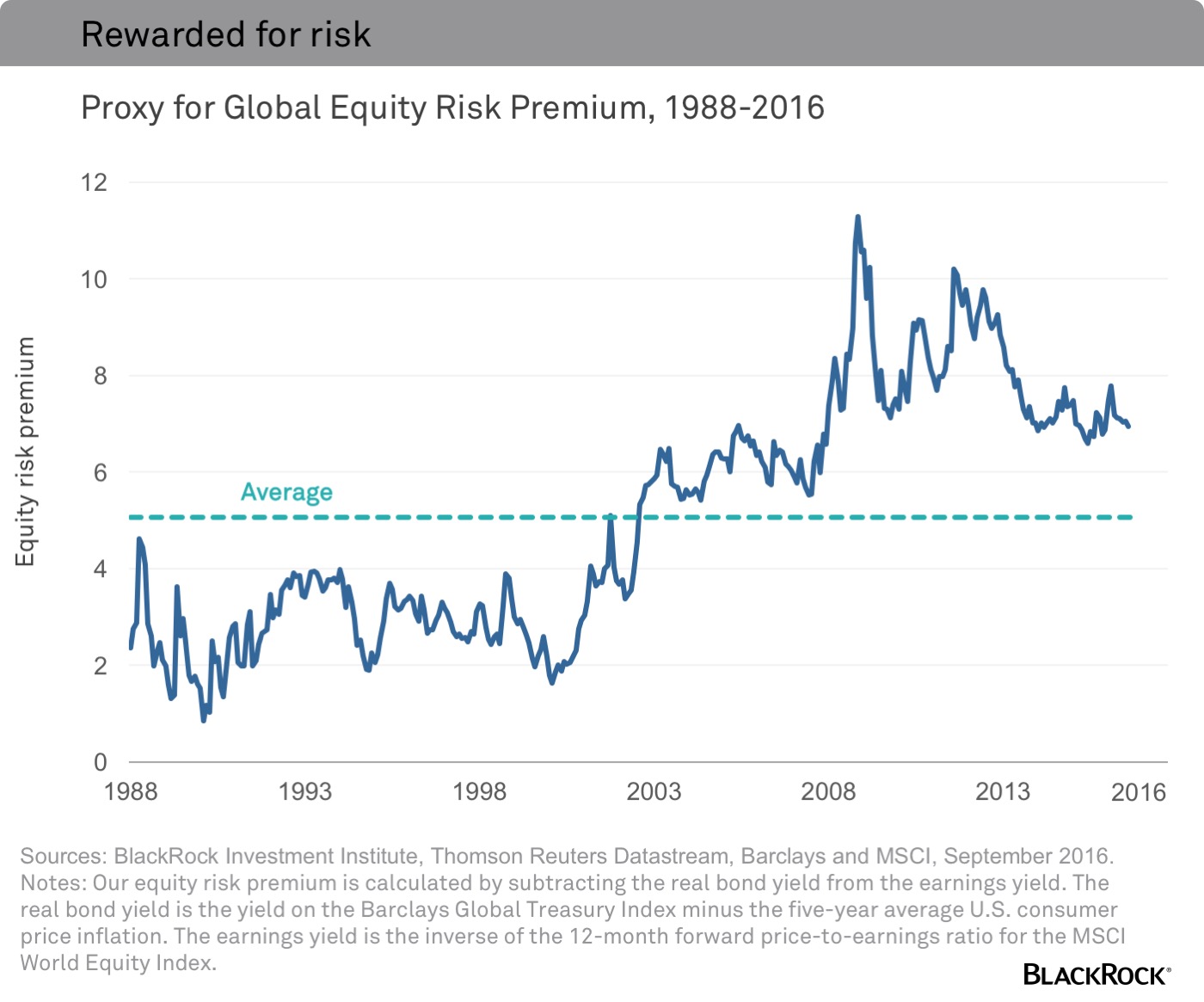

Our return expectations across most asset classes are at post-crisis lows, but we believe investors are getting compensated for taking on risk in equities, selected credit/emerging markets (EM) and alternatives.

Equities still look cheap on a relative basis due to the precipitous drop in bond yields. Our measure of the gap between expected returns on global equities and real government bond yields—a proxy for the equity risk premium—has fallen from recent peaks, yet still sits well above its long-term average. In other words, investors are still compensated for taking on equity risk in an environment where we expect very low returns across asset classes in the next five years. See the chart below.

High valuations versus history point to more muted returns in the future across asset classes. Yet low nominal gross domestic product growth and aging populations argue for lower bond yields than in the past—and sustained demand for high quality bonds. This structural shift changes the prism of assessing today’s valuations. It makes risk assets such as equities and local EM bonds look attractive on a relative basis. We see relative valuations mattering more in today’s low-growth, low-interest world.

3. Volatility