Still trying to define smart beta? Rest assured that you are in good company, as many investment managers may not realize they have run a smart beta fund for years—until they were informed by a marketing person! Perhaps that is why investors find the term “smart beta” to be confusing, misleading or even meaningless, which is compounded by the interchangeable use of the term “strategic beta” by many investment professionals.

As there is no universally agreed upon definition in the investment world, smart beta has become a catch-all category. Any new investment vehicle/fund seems to be labeled—or become—a smart beta product, rather than accurately referred to through the type of index at the foundation of the product. When firms utilize smart beta they may be referring to a product based on single or multiple factors, strategies, themes or any number of other ideas.

Defining smart beta often falls across a spectrum. On one side, some believe it only encompasses factor indexes, whereas on the other end, some believe it is simply any alternative to market cap indexes. The simple definition of “everything but market cap indexes” captures the many different types of strategies included in smart beta, but then excludes different types of indexes such as volatility, options based, risk control and hedging. The one common characteristic all smart beta indexes share is that they are rules based. While most investors only think about smart beta in equities markets, similar approaches also exist in other asset classes and are growing in commodities and fixed income.

Smart Beta Background

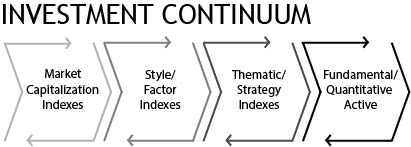

In the 1960s, leading academics identified “factors” as drivers of equity returns. Shortly after, factor indexes, such as style indexes and equal-weighted indexes, were created as performance benchmarks, not for investible products (like most indexes). Now indexes have become the growth driver in product innovation. I like to think of investing as a continuum with “passive” market cap indexes on the left hand and active management on the far right. The source of returns also follows that continuum, with beta originating from a market capitalization index and alpha (from security selection and market timing) as the goal of active management. By this accounting, the rules-based indexes of smart beta are trying to enhance returns, reduce risk or provide returns of an uncorrelated nature.

Why Is There So Much Interest In Smart Beta?

Investors want the option to invest in funds beyond pure market cap indexes, or active management, and smart beta offers that alternative. It has been estimated, on average, that one new smart beta ETF has come to market every week in the last three years, and that the total number of smart beta ETFs tops 500. Ignore the smart beta label and these ETFs become investible products tied to single- or multi-factor indexes such as size, momentum, high dividend, minimized volatility, etc. They bring the benefits of “passive investing” such as lower fees, taxes, holding costs and increased transparency, together with the outperformance potential of active investing.