Sharing businesses have emerged as the hot topic in the current wave of technology excitement. Start-ups are competing to be “the next Airbnb” of every industry imaginable, and are vying for the capital that label can attract.

Airbnb itself advertises three times more beds than the world’s largest hotel chain. Meanwhile, Uber has rapidly become the largest passenger transport network. Identifying sectors vulnerable to similar disruptions and understanding existing companies’ exposure and strategic responses is increasingly vital given the scale and speed with which change can unfold.

The signs of disruption are clear and fast

– Sharing businesses receive more venture capital funding than any other category, having overtaken social media platforms. The total value of sharing start-up businesses had reached $219 billion by mid-20153, with $20 billion of new capital invested in the sector in just the last two years

– Sharing revenues are set to grow at 25% annually over the next decade, and are expected to reach$335 billion by 2025, according to PWC5.

The drivers of this growth are swelling

Growing trends particularly among the younger generation – who represent the most active users of sharing businesses – serve to complement the “sharing” culture. Such trends include: access to communication technologies; increased trust and social acceptance of online exchanges and sharing; recognition of existing inefficiencies; significant savings; and flexible working patterns.

Few opportunities to invest in the theme through public equity markets

With an ability to scale with limited capital, most sharing businesses operate outside public equity markets and provide little visibility into their finances or operations. Our main focus is therefore on the abilities of existing companies to adapt and defend their competitive positions, and potentially ride the growth opportunities this presents if they are able to adapt quickly enough.

Sharing businesses pose a threat to listed companies in exposed sectors

In markets for which sharing businesses started earlier and have achieved greater scale, the impacts on established companies are already becoming clear:

– Barclays has estimated that car sharing, when combined with autonomous driving technologies, could in time lead to a 40% drop in the demand for cars and a 60% fall in the number of cars on roads globally

– Airbnb – which currently represents 1% of global lodging supply – could grow to 5% of the global market by 2020, according to Credit Suisse

– Peer-to-peer lending and small-and-medium-enterprise crowdfunding remain tiny as a market share (1%–2% of bank lending 6). However, global crowdfunding more than doubled last year to $34 billion7, and The World Bank estimates it will reach $90 billion by 2020

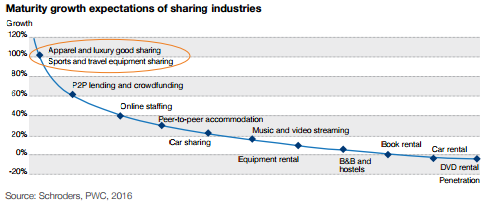

But more sectors may be at risk

By examining large categories of spending on consumer durable goods with low utilization rates and for which physical sharing is straightforward, we have identified markets we think are likely to face new disruption, circled here in orange:

Sharing businesses are typically based on a kernel of innovation that allows them to undermine the economics of traditional peers. Airbnb uses the scale of an online marketplace to allow home owners to generate a positive return on property and eliminates redundant administrative and service overheads its users don’t require. Uber similarly leverages an online market place to bring together self-employed drivers and passengers. Had existing companies recognized those business model opportunities, they might have more easily stemmed their growth by adapting their own strategies.

Every industry will face different challenges

Companies are starting to find novel ways to adapt. Peer-to-peer insurer Lemonade is apparently looking at ways to leverage behavioral analytics and distributed ledgers (holding records with customers rather than centrally). Others – like Heyguevara, Bought by Many and Friendssurance – are building policy pools that create small “captive insurers” for groups of people or friends, who are likely to try to keep their claims and premiums down. Many established insurers are looking at ways of exploiting ubiquitous smartphone ownership to monitor driving behavior and even patterns of home occupancy. Another strategy is to buy emerging competitors once their business is scalable, although this is typically costly and difficult to execute.

We are monitoring trends to identify winners and losers

Our approach is to (i) observe markets where the conditions are ripe for disruptors; and (ii) conduct discussions with companies on the changes they expect and the responses they are preparing. This two pronged approach is providing insight into the winners and losers of the sharing economy.

Solange Le Jeune is ESG (environmental, social and governance) analyst at Schroders.