Whether it is speculation about when the Fed will act on interest rates or wariness over the upcoming earnings season in mid-October, advisors and clients are staring down an election year market that’s likely to have the jitters for some time to come.

Increased volatility, limited growth opportunities and a low-return fixed income environment have essentially become the new normal. One option for tackling these unpredictable and challenging times is for advisors and clients to examine the effectiveness of long/short strategies.

The starting point for such an evaluation is current market valuation and fundamentals. Equities are exhibiting lofty valuations by historical standards, with a Shiller Cyclically Adjusted PE Ratio of about 27.3 times earnings versus a long term average of 16.6, and interest rates are again moving toward their all-time lows, as measured by the 10-year Treasury.

While equity valuations can reside far from their means for extended periods, bond valuations expressed in current yields do tend to be more predictive of near-term returns for investment grade debt, a key component of the typical core portfolio. With that in mind, let’s explore the potential pathways for rates.

Closer To Zero

What if rates remain relatively flat for the next few years? Over the medium term, the best predictor of bond market returns, as measured by the Barclays Aggregate Bond Index, is the yield at the time of investment. The yield on the index was about 1.88 percent on Aug. 31.

Further, an estimate of future inflation based on a model that combines the inflation forecast from the Philadelphia Fed’s Survey of Professional Forecasters and the implied breakeven rate of inflation between nominal Treasuries and TIPS (adjusted for the liquidity premium), suggests that inflation will run around 2.1 percent over the next 5 years.

Therefore, even without a much feared rise in interest rates, the best investors can reasonably hope for from their U.S. investment grade bond holdings over the next five years is a return of very close to zero on a real basis.

Of course, the math will likely be worse if rates rise. Long-term corporate bonds and long-term government bonds experienced four consecutive decades of negative real rates of return beginning in the 1940s. Forty years is an entire investment horizon for the typical investor, who begins saving at age 25 and retires at age 65. While it would seem highly unlikely that history would repeat in such a way, advisors and their clients need to be aware that it isn’t outside of the realm of possibility.

And what if rates continue to fall? If that is the case, the U.S. economy will undoubtedly be knee deep in a worsening quagmire. Investors could still do well in investment grade debt for a while longer, but equities would likely falter.

All of this is exacerbated by the fact that clients don’t have the luxury to wait to earn the “average” returns offered by the long term. With only a few decades over which to save and invest for retirement, a prolonged period of low real returns can be quite detrimental, as that reduces the time over which compounding can work its magic.

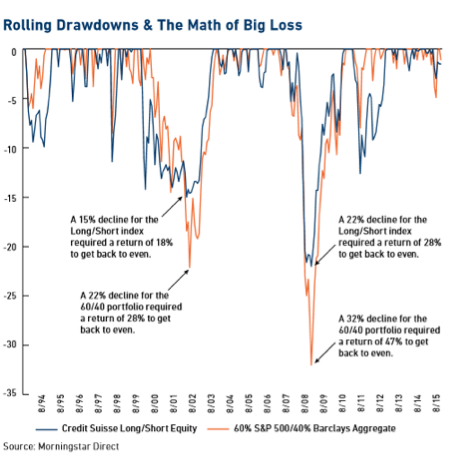

In low-return environments, the solution cannot be to throw caution to the wind, increase risk and hope for the best. The math of a big loss can be very difficult from which to recover.

The Long/Short Advantage

For advisors and their clients, the benefits to including long/short equity in an otherwise traditionally diversified portfolio are many.

For one, alpha generation at a time of low expected returns for both fixed income and equities becomes even more important. When markets are delivering strong returns, as was the case in 2013 when the S&P 500 was up 32 percent, 100-300 basis points of alpha would be nice, but not hugely impactful. If hypothetically on the other hand, a manager can add that level of alpha on top of 5-7 percent market returns, it’s a game changer.

But perhaps of greatest value to most investors is the potential ability of long/short managers to dampen volatility and help mitigate the possibility of a large loss.

The bottom line is that investors need to improve upon the return potential of an investment grade debt portfolio without taking on too much equity risk. Adding long/short equity while reducing both long-only equity and investment grade debt does just that. Over multiple market cycles (including two major crashes), long/short equity strategies have outperformed the 60/40 core on a risk-adjusted basis. In a market environment that portends low future returns, every basis point counts.

Clifford Stanton, CFA, is chief investment officer of 361 Capital and is responsible for managing the investment department, including oversight of strategy development, investment research and portfolio management. Stanton spoke on the topic of long/short strategies on September 19 at Financial Advisor’s 7th Annual Inside Alternatives conference in Denver.