Last Wednesday, on March 9, 2016, the bull market officially celebrated its seventh birthday. During that seven-year period, the S&P 500 nearly tripled, gaining 194% in price and producing a total return of 241%. Although our expectations for the stock market in 2016 are for only modest S&P 500 gains, we do not see the warning signs that have signaled the end of past bull markets and would not be surprised at all if the current bull market celebrates its eighth birthday one year from now.

Quick History Lesson

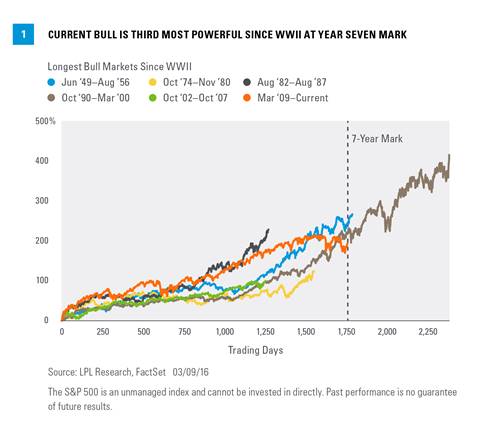

Despite all of the time that has passed, memories of the stock market collapse in 2008 and 2009 remain vivid for all of us. Set up by the severe 2008–09 decline, this bull market has been one of the strongest in history. Going back to World War II, only five bull markets have even made it five years, and only two of those celebrated their seventh birthday, making the current bull market the third longest over the past 70 years [Figure 1].

The previous two bulls to reach the seven-year milestone were June 1949 to August 1956 and October 1990 to March 2000. The rally in the 1950s lasted only one more month than the current bull, but the one in the 1990s lasted two more years. The current bull would have to stay intact until mid-2018 and propel the S&P 500 to over 3440 (up from 2022 on March 11, 2016) to match that epic bull market’s duration and performance.

When asked what the biggest driver of these gains has been, many might respond with Federal Reserve (Fed) policy. Certainly, monetary policy stimulus—including quantitative easing (QE) and the so-called ZIRP (zero interest rate policy)—has played a role in powering this bull. But S&P 500 earnings have more than doubled during the past seven years, and thus provided a good deal of support for the market [Figure 2]. Corporate America’s ability to drive profit margin expansion with efficiency gains during this decade is perhaps one of the most underrated pieces of the stock market’s seven-year run.

Higher valuations have also played a big role, not surprising given the extreme amount of pessimism at the lows seven years ago. On a trailing four-quarter basis, price-to-earnings ratios (PE) bottomed between 8 and 9 during March 2009 before spiking to 17 later that year [Figure 3]. Interestingly, the S&P 500’s PE is right around 17 today after peaking near 18 last year. Although a PE near 17 may seem high, it is roughly in-line with the average since 1980, and low interest rates are supportive of higher valuations. With some help from the possible resumption of earnings gains in the second half of 2016, we think valuations may be low enough to potentially keep this bull market going at least until its eighth birthday.

Sector Leadership