Clients often ask me: “How can the Federal Reserve raise interest rates when our debt is so high? Won’t higher rates just add to the burden?” With the national debt now at $18 trillion and climbing, it’s a reasonable concern. However, the Fed’s responsibility is the conduct of monetary policy, not fiscal policy. The national debt factors into the Fed’s decisions only insofar as it affects the economy and inflation. Otherwise, fiscal policy is in the hands of Congress.

©Charles Schwab & Co.

So, what do the debt dynamics look like? The Congressional Budget Office (CBO) compiles a lot of useful data on this topic. It recently released its updated 10–year projections for the country’s financial outlook. The report is available online here, and we’ll take a closer look at some of the numbers below.

Debt and deficits

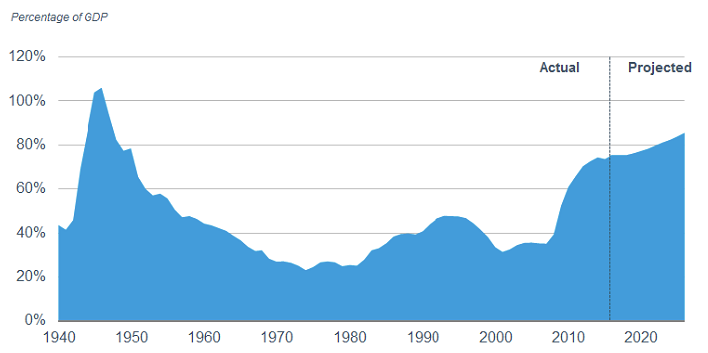

Total gross federal debt stood at $18.1 trillion at the end of the fiscal year 2015,1 or slightly more than the country’s gross domestic product (GDP) of $17.8 trillion.2 Government entities and agencies held about $5 trillion of that debt, with the public holding $13.1 trillion—or 73.6% of GDP.

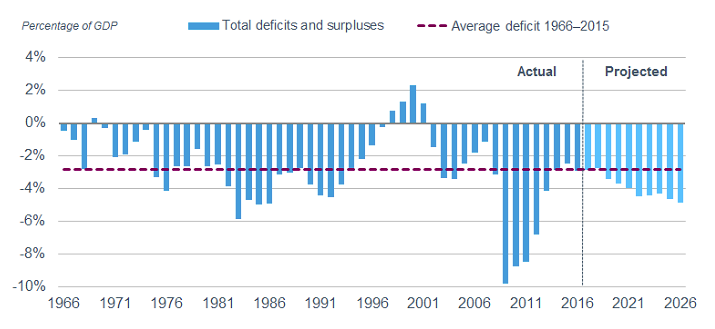

The good news is that annual budget deficits—which add to the federal debt—have fallen as the economy has recovered from the recession. The deficit came to about 2.5% of GDP in fiscal year 2015, down from nearly 10% in the depths of the financial crisis.

Federal debt held by the public

Source: Congressional Budget Office, “Updated Budget Projections: 2016 to 2026.”

That said, annual budget deficits are projected to start growing again over the next decade. The CBO projects that, under current budget laws, government spending will rise 5% per year over the next decade while revenues will grow by only 4%. As a result, the annual deficit is projected to rise to 4.9% of GDP by 2026, compared with 2.9% of GDP in 2016.

Higher deficits will add to the debt, with the amount of debt held by the public projected to increase to 86% of GDP. That would be the highest since 1947, and more than twice the long-term average of 40% of GDP.

Deficits exceed the 50-year average for most of the 2016–2026 projections

Source: Congressional Budget Office, “Updated Budget Projections: 2016 to 2026.”

Impact of rising interest rates

So how would higher interest rates affect all this? To start, higher rates would mean the federal government would have to pay more interest to Treasury security holders, and the resulting higher interest costs would add to the deficit and accumulated debt.

The CBO assumes the average interest rate the government pays on debt held by the public will increase from 1.7% in 2015 to 3.5% by 2026. It also projects a sharp rise in interest rates, with the average rate on three-month Treasury bills rising from 0.5% in 2016 to 3.2% a decade later. It sees the average rate on 10-year Treasuries rising from 2.6% to 4.1%.

But that’s not the only cost. When the Fed makes a profit on its Treasury holdings, it sends much of it back to the Treasury. Such profits have totaled hundreds of billions of dollars over the past decade. However, rising interest rates could push down the value of the Fed’s holdings, as bond prices fall when rates rise. That could mean Fed remittances to the Treasury will shrink.

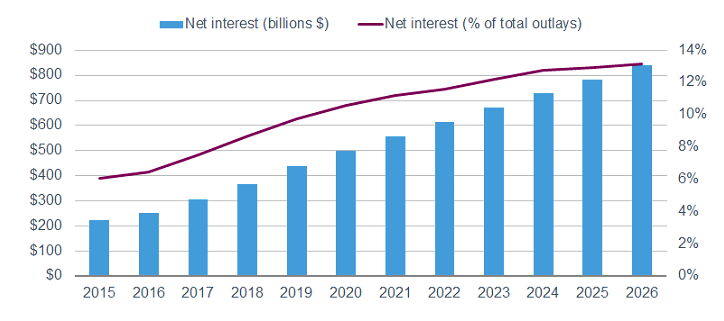

The combination of rising interest rates and declining remittances from the Fed could help push overall interest costs from $223 billion in 2015 to $839 billion in 2026. Relative to the size of the economy, that would increase interest costs from 1.3% of GDP to 3% of GDP over the next decade.

Projected net interest expense, in billions of dollars and as a percentage of total federal outlays, 2015–2026

Source: Congressional Budget Office, “Updated Budget Projections: 2016 to 2026.”

In the current fiscal year, interest costs are expected to be 6.1% of total outlays. By 2026 the cost will more than double to 13.1%, according to the CBO’s assumptions.

Those numbers might seem like a good reason for the Fed to hold off on raising rates. However, even if the Fed held interest rates at current levels, the impact on the budget would likely be limited, because the Fed directly influences short-term interest rates more than long-term ones. And holding short-term rates at low levels because of budget concerns could backfire. By keeping policy rates too low for too long, inflation expectations might rise, sending long-term interest rates higher.

Effect on the bond market

How will growing deficits and rising national debt affect the bond market? One possibility is that the government will have to issue more debt to cover its financing needs, potentially absorbing a bigger share of market demand. That could raise borrowing costs for non-government issuers and put upward pressure on yields.

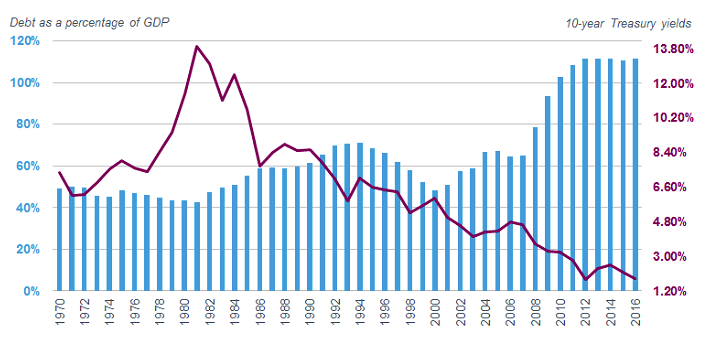

However, whether higher deficits and debts necessarily send bond yields higher hasn’t been proved, as demand for Treasuries is harder to measure than supply. The U.S. has experienced periods of rising deficits without a spike in interest rates in the past. In the late 1980s and mid-2000s, for instance, budget deficits expanded while interest rates declined. Other factors, such as economic growth and inflation, tend to have a bigger impact on bond yields.

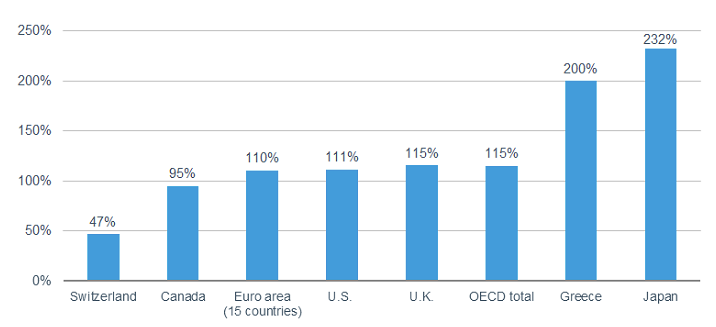

Rising U.S. government debt hasn’t stopped bond yields from falling

Source: OECD Economic Outlook, General government gross financial liabilities, as a percentage of GDP, 11/2015. The Federal Reserve Bank of St. Louis, 10-Year Treasury yields, Annual average, as of 3/30/2016.

Moreover, rising government debt levels are an issue in most major developed market countries, yet bond yields are low and have even declined. The U.S. debt-to-GDP ratio is well below the levels seen in many European countries and in Japan, where the national public debt is 232% of GDP. Bond yields in those markets are lower than in the U.S., or even negative.

General government gross financial liabilities, as a percentage of GDP

Source: OECD Economic Outlook, 11/2015.

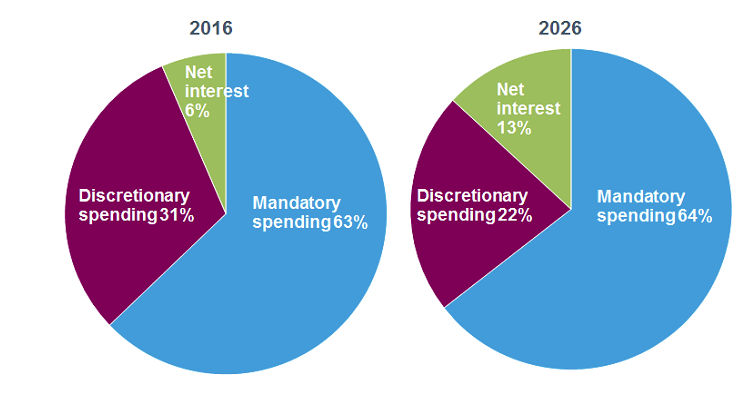

Mandatory versus not-so-discretionary spending

It’s also worth keeping in mind that mandatory outlays for programs like Social Security, Medicare and Medicaid—which represent about 63% of total spending—are much larger than interest outlays. With an aging population increasing the rolls of Social Security and Medicare,3 these expenses will likely rise rapidly over the next 10 years, though their share of spending is projected to hold relatively steady.

Amending or reducing benefits for these programs has proved to be difficult in the past, and it seems doubtful it will get any easier now that more people receive these benefits.

Mandatory versus discretionary spending, as a percentage of total outlays

Notes: Mandatory spending consists of Social Security, Medicaid/Medicare and other health-care programs. Discretionary spending consists of defense and nondefense spending.

Source: Congressional Budget Office, “Updated Budget Projections: 2016 to 2026.”

Finding savings in the budget to offset the increases in mandatory spending programs and interest costs is likely to prove challenging. After the mandatory programs and interest expenses, the only area left is discretionary spending. About half is defense spending, which has already shrunk to 3.2% of GDP, its lowest level in more than 40 years. The other half of the discretionary sector includes things like health care for veterans and programs for food and drug safety, transportation, education, national security and scientific research.

Since most people rely on this spending to assure the safety of the highways, the trains and planes we travel on, the food we eat, and the medicine we take, spending cuts may prove difficult, as well. Even assuming that discretionary spending slows, as the CBO does, budget deficits and the overall national debt will continue to grow relative to the size of the economy.

A rising debt load is a risk factor for the economy, but we don’t see it affecting the path of Fed policy. Nor is it necessarily the case that a rising debt load will cause bond yields to move up over the next few years. Longer term, rising government debt issuance could raise the cost of borrowing for non-government borrowers by absorbing more demand. A high debt can limit the government’s ability to spend on discretionary items such as productivity-enhancing infrastructure or invest in scientific and medical research. With elections approaching, now would be a good time in our view to have a thoughtful national conversation about budget priorities. Let’s hope that happens.

Kathy A. Jones is senior vice president and chief fixed-income strategist at the Schwab Center for Financial Research.

Will Rising U.S. Debt Levels Keep The Fed On Hold?

April 5, 2016

« Previous Article

| Next Article »

Login in order to post a comment