The Federal Reserve looks to have outsourced monetary policy to the financial markets -- and that may not necessarily be bad.

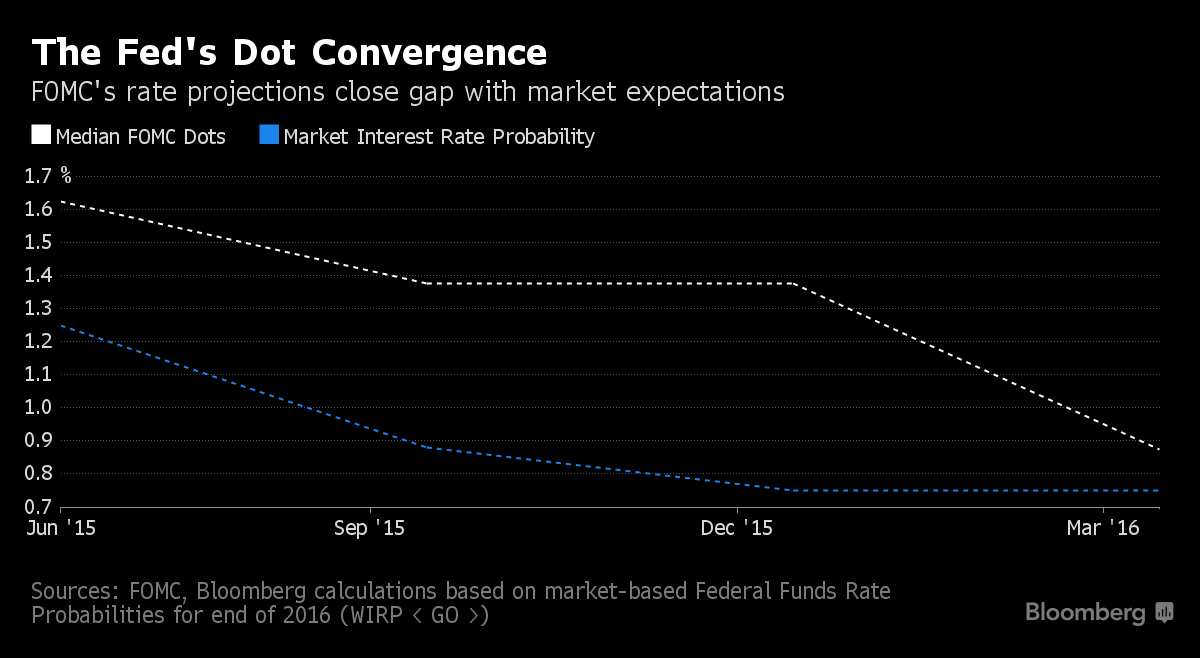

Fed Chair Janet Yellen told the Economic Club of New York on Tuesday that policy makers had scaled back the number of interest rate increases they expect to carry out this year after investors did the same.

She argued that the downgrading of rate expectations in the market had led to lower bond yields, providing the economy with needed support in the face of weaker growth overseas. The Fed then followed suit this month by reducing its anticipated rate hikes in 2016 to two from four quarter-percentage point moves projected in December.

“That’s a good thing,” said Lou Crandall, chief economist at Wrightson ICAP LLC in Jersey City, New Jersey, commenting on the sequence of actions. “Monetary medicine gets into the blood stream faster if the public can anticipate what the Fed’s response to an economic shock will be.”

There are pitfalls. Investors may become so impressed with their ability to influence Fed policy that they’ll press for more stimulus than the central bank is willing to supply.

Forcing Fed

“The risk is that markets’ perception of such continued accommodation will embolden them even more to try to force the policy hand of the Fed,” Mohamed El-Erian, chief economic adviser at Allianz SE and a Bloomberg View columnist, said in an e-mail.

Indeed, investors in the federal funds market are betting that the central bank will raise rates just once this year, not the two times policy makers envisage.

The Fed’s experience over the last six months also shows how difficult it can be for the central bank to align investors’ view of optimal monetary policy with that of its own.