Investors think ETFs are fungible. They think that you can take one “large-cap” ETF and replace it with another and you won’t notice the difference.

Sometimes it’s true. The difference between the SPDRs S&P 500 ETF (SPY) and the iShares S&P 500 ETF (IVV) over the past year is 0.15%. Given that the funds are up about 30% each, that’s a rounding error.

Even when funds track different indexes, the differences in return can be small. The iShares Russell 1000 ETF (IWB) doesn’t track the same index as SPY or IVV, but it’s still a large-cap ETF. Over the past year it’s up 30.49%, while IVV is up 29.73%. Chump change.

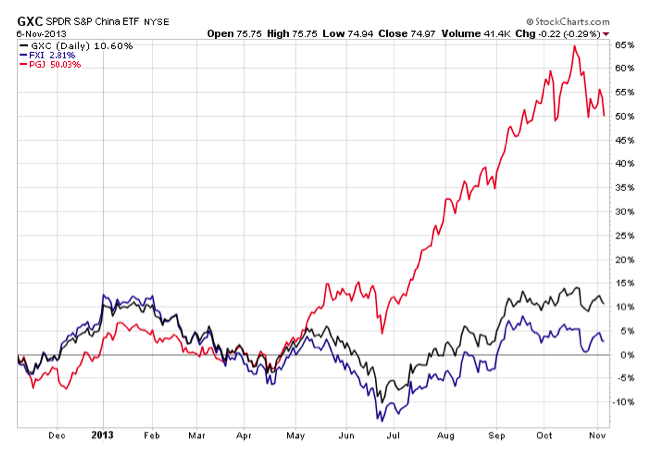

But sometimes, the differences are huge. Consider this chart of three popular China ETFs.

The most popular fund on this chart is the one at the bottom, the iShares FTSE China 25 ETF (FXI). FXI was the first China ETF to launch and has been around since 2004. It owns 25 of the largest, most liquid securities in China. These are mostly formerly government-owned firms such as China Construction Bank (9% of the portfolio), Industrial and Commercial Bank of China (8%) and Bank of China (6%). The fund is dominated by old-line sectors including financials (56%), telecom (16%) and energy (16%), and has just 7% of its portfolio in technology and 3% in consumer stocks.

It's gone nowhere over the past year, posting a meager 2.81% return due to slowing growth in China and mounting concerns about the stability of its financial sector.

Investors have $5.4 billion invested in FXI..

The second line on that chart, the SPDRs S&P China ETF (GXC), is a better fund. It holds a broad-based portfolio of 234 names representing all parts of the Chinese economy. It’s still heavily concentrated in financials (the largest sector, with a 33% weight), but it’s got a huge slug in technology (17%) and more than 13% of its portfolio in the consumer space. It’s even got a smattering of health care holdings (2% of the portfolio), which are utterly absent from FXI.

GXC is a great way to play broad-based China, and that’s why it’s outperformed: While the government sector has suffered, the consumer and tech economies in China are booming.

GXC is the IndexUniverse ETF Analytics Analyst Pick for China, meaning we think it is the best ETF for broad-based exposure. It has $907 million in assets under management, and is up 10.60% on the year.

But what, you’re wondering, is that bright red line? How do you get that?

That bright red line is the PowerShares Golden Dragon China Portfolio ETF (PGJ), which has been around since 2004 and has $312 million in assets. PGJ is unusual in that it only holds US-listed shares of Chinese companies. These include ADRs for companies listed in China, as well as a number of companies that only list in the US.

PGJ severly underweights financials and energy, because none of the big government-owned firms are included in the index. Instead, the fund bulks up on technology, which is the largest sector at 46% of the fund. Its top holdings list is dominated by Chinese tech firms like Baidu, the Google of China, which only lists in New York and is not present in FXI at all.

PGJ also tilts toward the entrepreneurial small-cap sector of China, with 40% of its portfolio focused on small or micro-caps.

Just scan a comparison of PGJ’s top 10 holdings with those of FXI:

What should you do with China? Should you pile all your money into PGJ, forsaking the more traditional funds?

The answer, of course, is no. Just as PGJ has outperformed over the past six months, so too might it underperform over the next six.

But the comparison of FXI, GXC and PGJ does show you that owning China is not as simple as buying one fund and forgetting it. Here’s my advice.

If you own FXI, you shouldn’t. FXI is an old-school fund that is too narrow and over-concentrated in government securities. If you want any exposure to the thriving consumer or technology sectors in China, FXI isn’t going to get it done. It’s liable to underperform the market in a meaningful way over the next 10 years, as the consumer economy surges and the government-dominated financial sector suffers under the weight of bad debt.

A better choice for broad-based exposure is GXC. With GXC, you cover your bases in China, capturing the important financial sector and other critical markets including consumers, technology and health care. GXC – or its close competitor, the iShares MSCI China ETF (MCHI) – should anchor your Chinese exposure.

And if you want to get truly diverse exposure, add in PGJ to the mix. PGJ captures a number of critical companies – such as Ctrip, the Expedia of China – that are missing or underexposed in competing ETFs.

ETFs are supposed to be an easy way to get exposure to different markets, and they are. But it’s not always the case that the most popular fund is the best one.