As you approach retirement age, planning is everything, right down to the pennies. But you could be in for a severe case of sticker shock when you find your Medicare Part B and Part D premiums are much higher than you’ve budgeted for. The good news is there’s an appeal process for those who disagree with this adjusted amount. Here, we’ll take a look at that process and walk you through the options.

First, a word about Medicare Part A. Most who enroll in Part A, which provides hospital coverage, will not pay monthly premiums. This goes for anyone who has worked at least 10 years, or 40 working quarters, and has paid into the system through Medicare taxes.

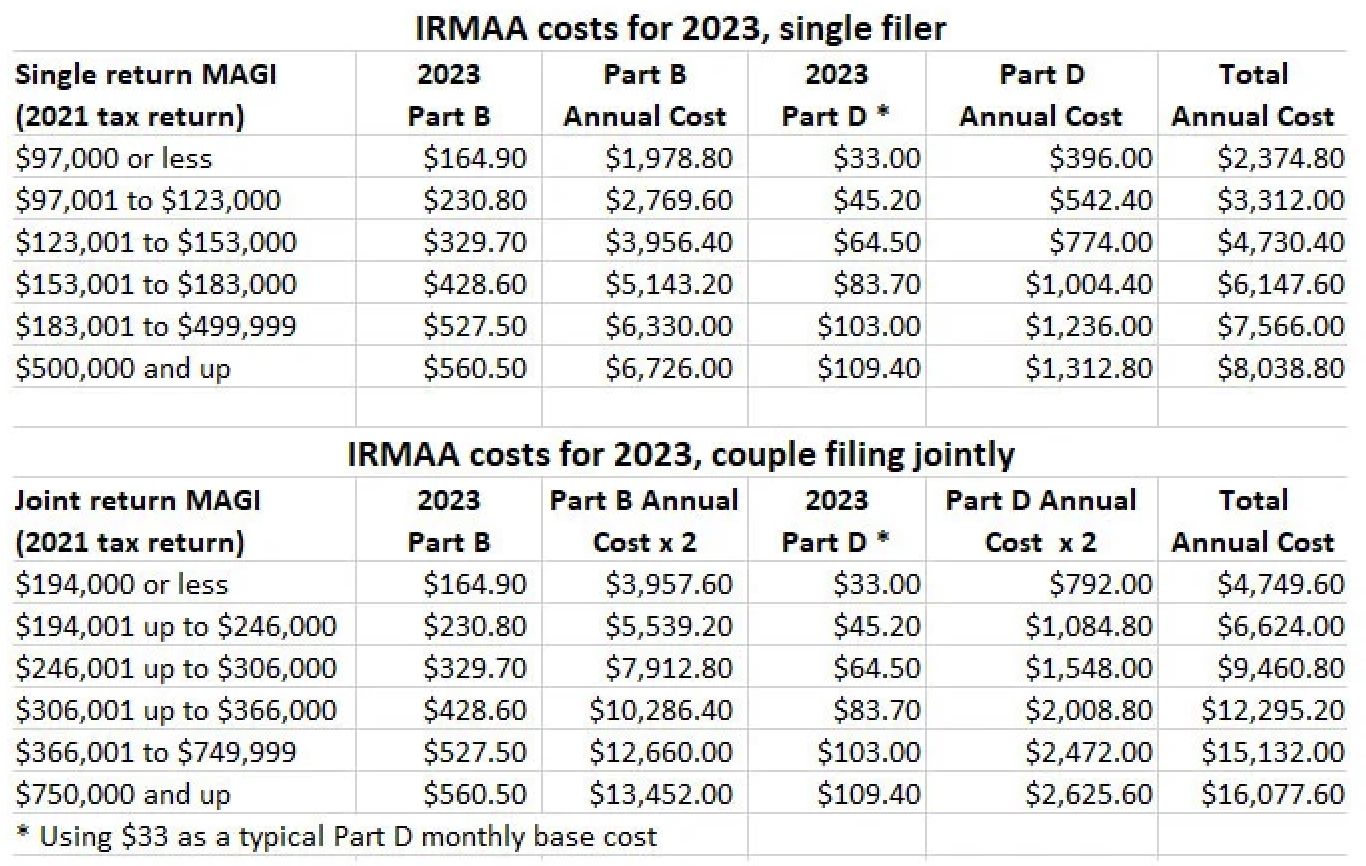

Medicare Part B is a different story. Your monthly premium for Part B, your doctor/outpatient coverage, is determined by the Social Security Administration, which runs Medicare, and can change every year. It’s set for the following year in late September or early October. In 2022, the standard Medicare Part B premium was $170.10. This year, it’s $164.90. That standard premium increases based on your gross income as reported on your taxes filed two years prior to the current year. So that means SSA is looking at your 2021 gross income to determine your 2023 Medicare Part B premium.

Of course, if you’re a recent retiree, your 2021 gross income is going to be significantly higher than what you’re bringing home this year. And yes, that will mean your Medicare Part B premium could be much higher than the standard premium.

Meet IRMAA

For many seniors, this sudden increase in monthly expenses comes as a big surprise. If you’re in this boat, you will receive a letter a few weeks before your Medicare effective date informing you of your income-related monthly adjustment amount, or IRMAA. For some high earners, the monthly cost could jump as high as $560.50 per month, a nearly 240% increase from the standard premium. The chart below shows what those additional Part B costs look like for 2023.

Higher earners might also be in for a surprise when they find their Medicare Part D drug coverage costs more than they expected. IRMAA applies here too. If your income is above $97,000 filing individually or $194,000 married filing jointly, you’ll pay an extra amount on top of your plan premium. This extra amount could be as low as $12.20 per month for an individual making between $97,000 and $123,000, or as high as $76.40 per month for an individual making $500,000 or above. And remember, that’s on top of your monthly premium.

You can appeal IRMAA if you’ve had a qualifying life event, such as work reduction, loss of income-producing property, loss of pension income, marriage, divorce, death of a spouse, work stoppage or an employer settlement payment. Your retirement counts as a work reduction. But be aware that if your appeal is successful, you will need to appeal again next year–RMAA recalculated every year based on your income from two years prior. So your 2024 IRMAA will be determined based on your 2022 tax return.

Also keep in mind that a capital gain might tip you into another tax bracket, affecting your IRMAA. You should consult with your tax professional to plan for these potential increases.

Toby Stark is the founder of Stark Associates Insurance Agency.