Purchasers agreed to pay more than the asking price in 10 percent of deals for properties under $3.3 million -- this quarter’s definition of “non-luxury” homes, making up the bottom 90 percent of the market, according to a report Thursday by appraiser Miller Samuel Inc. and brokerage Douglas Elliman Real Estate. It was the biggest share of transactions with bidding wars since the firms began tracking the data in the second quarter of 2016.

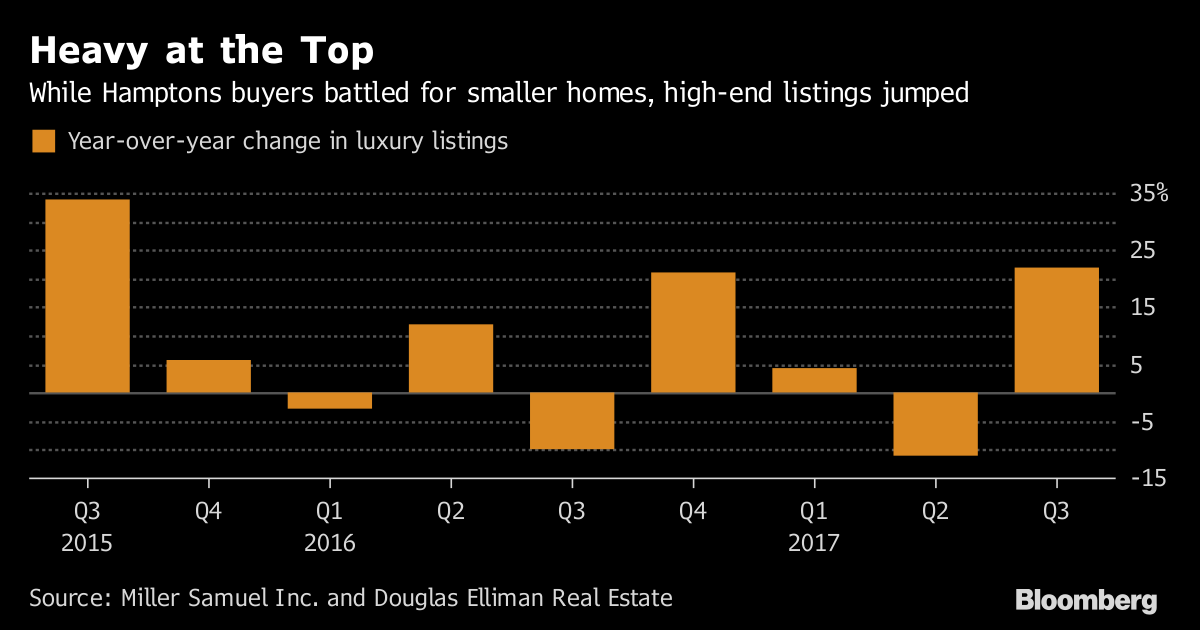

In their zeal for lower-end deals, buyers snapped up condos as well. Those units -- with a median sale price of $567,500 -- were available for just 97 days on average before going under contract, the fastest clip in six years of record-keeping. On the high-end, buyers showed less interest in acquiring luxury homes than sellers did in listing them. Inventory in that top 10 percent of the market jumped 22 percent, the biggest pile-up in two years.

“The market is looking towards those smaller, more manageable homes,” said Carl Benincasa, a regional vice president at Douglas Elliman who oversees sales in the Hamptons. “That’s certainly been a trend we’ve been observing.”

With stocks at record highs, people are in a buying mood in the Hamptons. The beachside towns on Eastern Long Island, whose fortunes are closely linked to the performance of the financial industry, had 517 total sales in the three months through September -- or 12 percent more than the 10-year quarterly average, Miller Samuel and Douglas Elliman said. Even with all that buying, inventory declined only in the non-luxury category, with listings dropping 10 percent from a year earlier to 1,143.

Buyers of Hamptons homes in the third quarter didn’t want to splurge on something too costly, but they were willing to bid up cheaper properties in their search for a vacation retreat.

Hamptons Buyers Battle Over Cheaper Homes—That Is, Under $3.3 Million

October 26, 2017

« Previous Article

| Next Article »

Login in order to post a comment