Inflation finally surprised markets in good way, and traders are understandably enthusiastic that the worst price pressures may finally be in the rear-view mirror. But the true turn for the better will come when inflation ceases to be shocking altogether—positively or negatively—and can fade into the background once again.

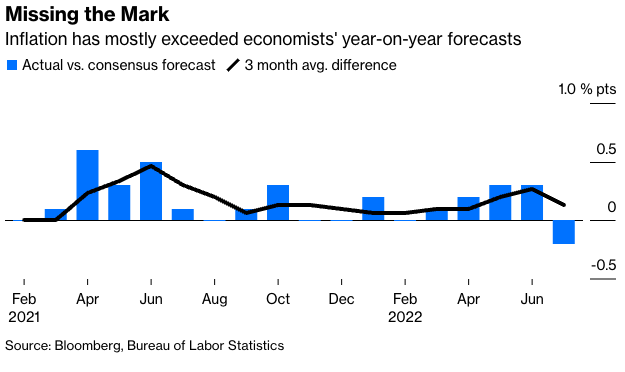

The consumer price index rose 8.5% in July from the same month a year earlier, the Labor Department reported on Wednesday, less than the median estimate of 8.7% in a Bloomberg survey. Of 46 forecasts, only two hit it right on the nose (Credit Suisse Group AG and High Frequency Economics). The consensus has now scored direct hits on just four of the past 17 CPI forecasts, with Wall Street economists underestimating inflation 12 times during the period. Even if the outlook seems to be improving, the Federal Reserve and financial markets are still flying somewhat blind, which means the odds of a policy mistake remain high.

Inflation isn’t inherently bad because it’s elevated but because it has been so unpredictable, though sustained high inflation would indeed be harmful. If everyone knew that prices would inflate by, say, 6%, businesses could all adjust wages and consumer prices accordingly and most people would be more or less fine. It’s the unexpected inflation that makes it hard for businesses and households to make prudent investment decisions, making real earnings volatile and restraining the economy. Unexpected disinflation is certainly better than the alternative at this juncture, but it’s not great either. Certainty is the optimal outcome.

That the numbers are still surprising—albeit to the downside—means economists still don’t have a handle on what’s happening. How fast will inflation come down from here? Will it settle in at a level that’s acceptable to the Fed? Or will it become sticky at around 4% amid strong wage pressures? Without much visibility as to even the next month’s inflation report, it’s hard to answer those questions with much confidence, which means Fed Chair Jerome Powell will still struggle to thread the needle in delivering monetary policy that does just enough to crush inflation without causing a recession.

Last summer, economists seemed to have the situation pretty well diagnosed, with one spot-on forecast and a few close misses that showed that inflationary pressures seemed to be ebbing. Then inflation accelerated and hardly anyone saw it coming.

Again around the turn of the year, there were a flurry of good calls as many experts saw “peak inflation” on the horizon. Once more, the idea that economists had figured out inflation vanished in the following months as big misses again became common. Until now, the bias has consistently been toward underestimating the problem; the last time Wall Street economists overestimated inflation was for the report on Feb. 10, 2021.

The problem is multifaceted and demands much soul-searching. For all the surveys and real-time data available, there are still plenty of blind spots, and many models still draw on past trends and statistical relationships. That can make them prone to underperformance in a changing economy, especially at key inflection points.