Most retail portfolios have little exposure to managed futures today. Managed futures mutual funds and ETFs total approximately $.8 billion in assets—a paltry sum given the trillions of dollars invested in stocks and bonds. Investors might want to consider adding more exposure to managed futures. After a 10-plus year bull market in equities and with fixed income yields near historical lows, retail portfolios need strategies with proven diversification benefits, especially those that can deliver strong performance during a bear market. This article explains how asset allocators and advisors could better evaluate managed futures strategies, how to include managed futures in a traditional portfolio, and how best to manage client expectations to avoid selling at the wrong time.

1. Evaluate The Performance Of The Asset Class, Not Individual Funds

Managed futures as a “asset class” is perhaps best defined as the average pre-fee performance of firms that employ the strategies. Getting to this performance is more complicated than with traditional indices. Benchmarks, such as the SocGen CTA and the Barclays indices, compile the performance of hedge funds after hedge fund fees and expenses—estimated to be 300 bps per annum. This means that a big chunk of alpha generated over the past ten years was diverted towards fees.

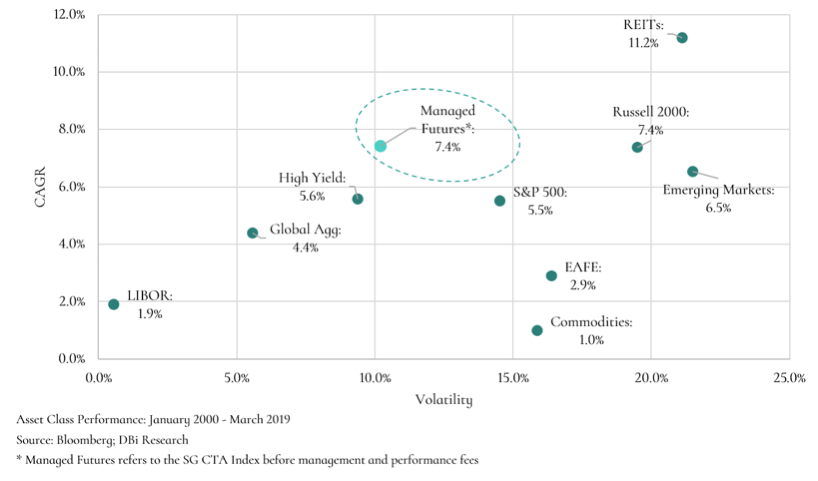

The most accurate way to estimate historical performance of the asset class, then, is to add back estimated fees. The difference in results is startling: since 2000, managed futures have outperformed the S&P 500 (7.4 percent per annum vs. 5.5 percent) with lower volatility and with a correlation around zero. As an asset class, managed futures arguably have more diversification “bang for the buck” than REITS, commodities, and even bonds.

2. How To Include Managed Futures In A Portfolio

Using asset class returns, allocators should target a 10-20 percent allocation in a traditional portfolio. In fact, since 2000 a 20 percent allocation to a 60/40 portfolio would have increased returns by 10 percent, reduced volatility by 18 percent, and lowered drawdowns by 26 percent. (The 60/40 portfolio is defined as 60 percent of a portfolio allocated to the S&P 500 Index and 40 percent allocated to the Barclays U.S. Aggregate Index. The statistics (return, volatility, drawdown) shown are the percentage changes in the statistics.)

However, picking a single manager fund is challenging. The annual dispersion between good and bad managed futures funds is around 30 percent a year—akin to the riskiness of buying a single stock rather than the S&P 500 or a diversified mutual fund. To compound this, last year’s top performers are no more likely to repeat this year—a concept called “lack of persistence.” When investors chase performance and invest in a recent highflier, the final outcome might be different.

Instead, allocators and advisors should seek diversified exposure to the space. One solution is to spread bets across a number of funds. To get appropriate diversification, we believe a portfolio should have a minimum of six individual managers. A more promising approach may be to identify funds that offer diversified exposure. Another, and likely most efficient approach, is to select a replication-based product which can deliver diversified exposure with lower fees—similar to an index ETF or mutual fund.

3. Set Clear And Realistic Client Expectations