Nearly half of all advisors are using some sort of tactical investment strategy, according to new research from Cerulli Associates. This important research quantifies what we have been witnessing—advisors are actively seeking alternatives to the 60/40 buy-and-hold investment approach of the past.

Why? The 60/40, stock/bond asset allocation model favored by most investment houses and embraced by advisors for a generation is outmoded and not likely to help investors achieve their objectives.

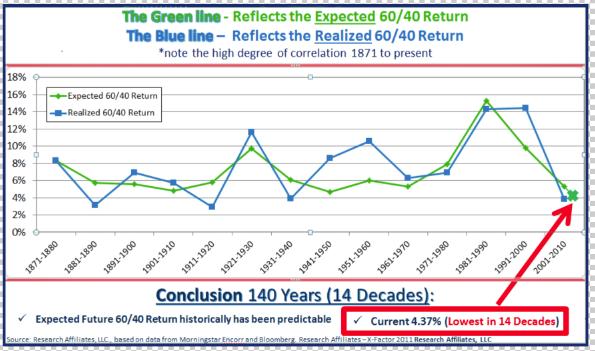

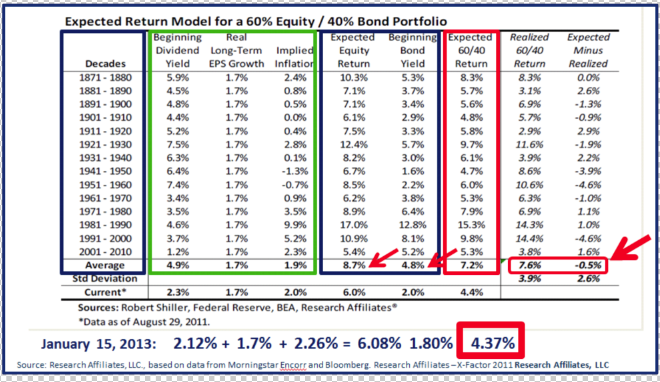

We are in an investment environment that offers historically low traditional investment returns. Today, the projected return on the traditional 60/40 model is the lowest in 140 years at 4.26 percent (excluding management fees), according to Research Affiliates LLC.

A better definition of a balanced portfolio today is 33/33/34. Enhanced Modern Portfolio Theory didn’t fail the last 12 years; the failure occurred in the construction process. The risks were too concentrated because the solutions were unavailable to most investors. Today, the solutions exist for all investors and advisors.

More importantly, there are a number of ways to protect long equity and fixed-income exposure. And there are several outstanding liquid tactical risk diversifying solutions to consider. The goal is to enhance overall portfolio return and reduce risk.

A balanced portfolio today is comprised of 33 percent equity (hedged from time to time), 33% fixed income (tactically managed) and 34% tactical-trading-alternatives. Of course, each investor will allocate differently based on risk level, age, needs, time horizon, etc.

I do believe that 8 percent to 10 percent returns are achievable over time. We favor an enhanced MPT portfolio construction approach to increase return and reduce portfolio risk. It involves a risk-managed approach towards beta, a careful view on bonds and inclusion of a select handful of tactical-trading-alternative strategies. It is a shift from 60/40 to 33/33/34.

The chart below is the math on 4.37 percent courtesy of my friends at Research Affiliates. The green line reflects the forward 10-year expected return while the blue line reflects the realized return. Note the high correlation of what was expected and what was ultimately realized. Could it be different this time? Maybe. I don’t like the odds.

The next chart details the math through the past 14 decades.

As of January 15, with a beginning dividend yield of 2.12 percent plus real LT EPS growth of 1.7 percent and implied inflation of 2.26 percent the expected equity return is 6.08 percent. Sixty percent of 6.08 and 40 percent of 1.80 percent equals 4.37 percent. Not too bad for equities, yet more than 2.5 percent lower than the historical average expected equity return of 8.7 percent.

As the U.S. and the developed world struggle with the weight of excessive debt, excessive regulation, increased taxation, irresponsible spending and unmanageable entitlements, I’m confident that we’ll find our way to a better destination, though not without some bumps. Too much debt impacts growth, and today’s low yields, low inflation and low interest rates simply don’t support attractive 60/40 forward 10-year returns. It is important to think differently.

With bonds yielding less than inflation and the planet doing everything it can to create inflation (massive currency creation and unprecedented policy) a bond market train wreak likely lies ahead. Not in the immediate future, with the continued large demand for bonds ($1 trillion this year by the Fed alone). However, the inflation seeds are planted and the risks loom large. Should rates rise just 3 percent, the loss on the 10-year Treasury will be approximately 23 percent, impacting the 60/40 portfolio by a -9 percent.

Moreover, today’s inflation rate is greater than the current 10-year Treasury yield of 1.87 percent. Bonds are producing a negative real return and are a very risky bet. With this footing, I share the following ideas on a better portfolio game plan for the period ahead. I favor 33/33/34 over 60/40.

33% Equities

Here, find inexpensive beta exposure like VTI Vanguard Total Stock Market ETF, VEU Vanguard FTSE All World ex-US ETF, and VWO Vanguard Emerging Markets Stock ETF, then hedge your equity beta exposure by periodically writing out of the money short term covered calls while at the same time buying intermediate term 5 percent out of the money put options. This is called a collared option strategy and is designed to inexpensively risk protect your equity portfolio. You might also consider just writing covered calls.

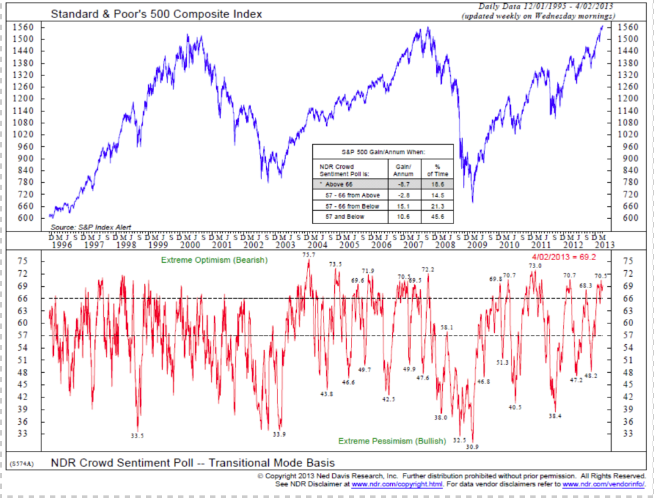

I like using investor sentiment as a disciplined way to time the entries and exits of the collared strategy. My favorite sentiment chart is NDR’s crowd sentiment poll, though there are many others.

Note the extreme optimism and the performance of the -8.7-percent S&P 500 Index Gain/Annum when above the dotted line at 66. Simply, the idea is to risk protect at extreme optimism and remove the risk protection at extreme pessimism. While no indicator provides a perfect signal, sentiment is my favorite.

Consider getting even more risk averse during cyclical bear market periods. The next chart is a 13-week over 34-week EMA chart and identifies cyclical bull and bear market periods. The red circle reflects the current bullish environment.

Additionally, there are a growing number of equity funds that have a volatility hedge built into the funds investment management process. Find them. This approach can provide equity upside with risk management protection and forgo the need to actively manage a collared option strategy.

33% Fixed Income:

Historically low yields and potential future inflation require a different view towards bonds. Here are several ideas for this portion of your portfolio.

High-yield bond ETF’s provide higher yield and importantly they trend in a predictable way. Consider trading the up trending periods in a HY ETF like JNK and moving to a short-term bond fund like VFSTX when the HY price trend begins to decline. A short-term moving average crossover might prove helpful in determining trends. Recessions are particularly painful for HY’s and this approach can help you avoid the declines.

Also, consider convertible bond securities and a safe harbor position in short term bonds and include TIPS for inflation protection.

A 34% Tactical-Trading-Alternative:

Consider select managers with experience and edge that can produce return in various market environments. Find diverse return streams that are non-correlating to equities and bonds and other tactical managers. The goal is to create a well-diversified portfolio of tactical-trading-alternative strategies.

Equal weight four or six strategies and consider including gold and REITs to round out the 34 percent weighting. The good news is that there are a number of liquid managed account strategies and a growing number of mutual funds available to you. Since alpha is a zero sum game (one winner for every one loser), choosing the right managers is critical.

Combined together, 33/33/34 is deeply diversified portfolio. We call it Enhanced MPT, “a mathematical formulation of the concept of diversification in investing, with the aim of seeking a collection of investment assets that has collectively lower risk than any individual asset.”

Most advisors are allocated 60/40. It is the standard and will likely return just 4.37 percent per annum over the next 10 years. Investors will seek advisors with a solution. Build a portfolio targeting an 8 percent to 10 percent return with 10 percent to 12 percent risk. It is possible.

Stephen Blumenthal is CEO of CMG Capital Management Group Inc. The firm offers managed accounts, mutual funds and variable annuities that are constructed to benefit from current economic conditions, and aim to provide steadier performance in all market cycles. More information is available at cmgwealth.com.

The New Modern Portfolio Theory

June 14, 2013

« Previous Article

| Next Article »

Login in order to post a comment