President Trump’s election platform “Make America Great Again” included protecting jobs and building businesses in the United States. To that end, U.S. Treasury Secretary Steven Mnuchin, Secretary of Commerce Wilbur Ross and the Director of Trade and Industrial Policy Peter Navarro have been working to normalize trade with our global trading partners. The focus is on normalizing unfair trade practices with China and Germany, but this also includes Canada and Mexico. China exported roughly $525 billion worth of goods to the United States last year and imported only $135 billion. President Trump is seeking to narrow that gap. Any efforts to narrow the trade deficit through tariffs will slow economic growth in China. Ultimately, a trade spat will slow economic growth in the United States near term as well. With respect to China, we expect Trump’s goal is to normalize bi-lateral trade at the margin and to take steps, which have yet to be defined, toward protecting intellectual property that China steals from the United States.

The Chinese Economy

In 1972, President Nixon and Henry Kissinger broke a 25-year period of no communication between China and the United States and visited China. Up to that point, China was an underdeveloped country focused on rebuilding its economy after World War II. After normalizing relations, trading between the two countries began to grow. The socialist market economy of China, which includes state-owned businesses and centrally planned control, is now the world's second largest economy by nominal GDP. In addition, China is the world's largest manufacturing economy and exporter of goods according to the International Monetary Fund.

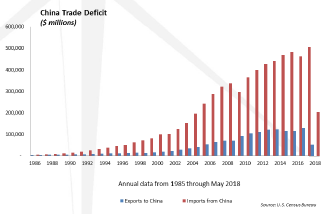

In the 1960s and 1970s, the words “Made in China” implied that, whatever it was, it was cheap and low quality. However, over the last three decades, China has invested heavily in its cities, manufacturing facilities, equipment and infrastructure in order to build a strong manufacturing-based economy. The impact on the trade balance has been dramatic. In 1990, the trade deficit the United States ran with China amounted to $10 billion. By 2017, the trade deficit had ballooned to $375 billion. This means that China sold more goods to the tune of $375 billion each year to the United States than we sold into China.

It is important to remember that China’s economy and capital markets do not represent free market capitalism. China’s form of capitalism is orchestrated by their central government. We have written over the years about how the Chinese economy works and recommend the book Red Capitalism by Carl Walter and Fraser Howie for a deeper understanding of China’s financial and capital markets system.

In its simplest form, the Chinese government injects capital into its banking system. The banks extend loans for construction, real estate, consumers and businesses; however, the central government effectively mandates the amount of loans a business receives. When the debt is not repaid, the problem loan may remain on the balance sheet of the banks, and the government injects more capital. As a result, China now boasts the world's largest total banking sector assets of $39.9 trillion with $26.5 trillion in total deposits. Discerning loan growth and quality is difficult for us since the data is suspect.

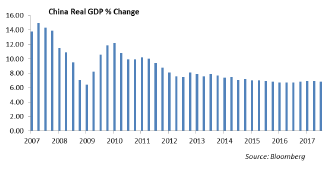

China’s central government has indicated that they are targeting economic growth of 6 percent. This is lower than the 10 percent average growth rate of the past 30 years.

The Impact Of Tariffs On China And The United States

This Administration has taken a more aggressive stance toward normalizing long-standing trade agreements with countries with which we trade in an effort to address unfair trade practices. China has been a net beneficiary of U.S. trade policy over the past 30 years. In addition, China unveiled a plan three years ago called “Made in China 2025” which identified 10 industries that China wanted to become globally competitive in by the year 2025. The tariffs that have been implemented and are proposed take aim at many of the industries highlighted in this plan. We expect China will not back down from its 2025 plan.

In his first initiative, President Trump has implemented tariffs on a package of capital and industrial goods, which include semiconductor components, steel and aluminum that could amount to $34 billion. The White House has proposed an additional $200 billion in tariffs on Chinese imports, which will touch cell phones, electronics, appliances and clothing. The impact of this latest proposed round is that the U.S. consumer will end up paying more for Chinese goods as well as some U.S. manufactured goods. According to the U.S. Commerce Department, cell phones and computers are the two largest imports from China with $70.4 billion and $45.5 billion respectively imported annually to the United States.

Tariffs act the same ways as taxes and will ultimately slow economic growth for both countries and raise prices for U.S. consumers as companies attempt to pass the tariff costs onto the consumer. However, we believe that China has more to lose in this trade spat than the United States.

The U.S. economy is on solid footing today growing at a rate near 2.7 percent annually with the unemployment rate at 3.8 percent and heading lower. The rate of inflation is nearing the 2 percent target and the Federal Reserve is in the process of reducing the simulative monetary policies that have supported economic growth since the financial crisis in 2008.

According to the National Bureau of Statistics of China, the Chinese economy grew by 1.4 percent in the three months ended March of 2018. This compares to growth of 1.6 percent in the previous period, the weakest pace of expansion since the first quarter of 2016. We expect the Chinese economy is on pace to grow at a rate of 6.8 percent annually. This is its slowest pace of growth in the past 26 years.

China’s economy is fueled with huge levels of debt and as their economic growth slows, the debt burden increases. According to the International Monetary Fund, China’s debt as a share for Gross Domestic Product is near 240 percent, up from 125 percent in 2002. China is in a danger zone with its financial sector and debt burden. As an economy slows, the interest expense on the debt can create a chokehold on consumption further impeding growth.

Slowing Economic Growth In China

We expect there are three scenarios that China will experience through the Administration’s push to increase tariffs:

1. China may experience a severe recession as the tariffs effectively reduce exports to the United States resulting in a sharp decline in China’s manufacturing production. This would severely increase their nonperforming debt, which will result in higher level of nonperforming loans putting additional pressure on their financial system. The yuan will collapse and their banking sector will require large capital infusion.

2. We would posit that another scenario is that everything goes back to the way it used to be. However, the Administration has made a pretty strong argument for how unfair the trade practices have been over the past two decades and the impairment on the U.S. economy. We would place a low probability on this scenario happening.

3. China and the United State come to an agreement that allows for fewer barriers for U.S. goods to be exported to China and address protections around U.S. intellectual property. We expect that this agreement would have a marginal impact on Chinese exports to the United States; however, the impact on the Chinese economy will result in slower growth. This will put pressure on the financial sector as the amount of bad debt increases albeit at a slower rate than the first scenario. The yuan weakens.

Two of the three scenarios we outline result in a slowdown in the growth of the Chinese economy. We do not believe the capital markets have discounted the impact of a slowing Chinese economy and the risk of the potential deterioration in the Chinese financial system. We believe that the Trump Administration knows that this is leverage they have and they are willing to use that leverage for the purpose of reforming trade agreements.

At the margin, the initial tariffs will hit earnings of companies in the manufacturing and technology sectors as raw materials costs and supply chain disruptions negatively impact margins. We also expect a slowing in business investment and capital expenditures as uncertainty causes management to rethink near term investment plans.

A prolonged trade war will act to suppress U.S. interest rates as economic growth slows. However, China’s demand for U.S. Treasury securities, which it uses to hedge its trade with the United States, may decline depending on the impact tariffs have on Chinese exports.

Gregory Hahn is president and CIO of Winthrop Capital Management.