Most seers believe the U.S. labor market is overly strong. Federal Reserve Chair Jerome Powell recently described it as “extremely tight” and “out of balance,” with demand for workers far outstripping supply. I beg to differ.

It is true that quit rates had risen as employees didn’t worry about finding new jobs. Also, job-switchers got annualized pay hikes of 8.4% in August, up from 5.8% early this year, according to the Federal Reserve Bank of Atlanta. That encouraged people to change jobs or strike for higher pay. There were 180 strikes involving 78,000 workers in the first half of 2022, up from 102 strikes covering 26,500 a year earlier.

Job openings are about twice the number unemployed, which means that to return to the 63.4% labor participation rate of February 2020, before the pandemic, it would require 2.8 million people moving into the labor force. Layoffs in July of 1.4 of million were about 23% below the average in 2019.

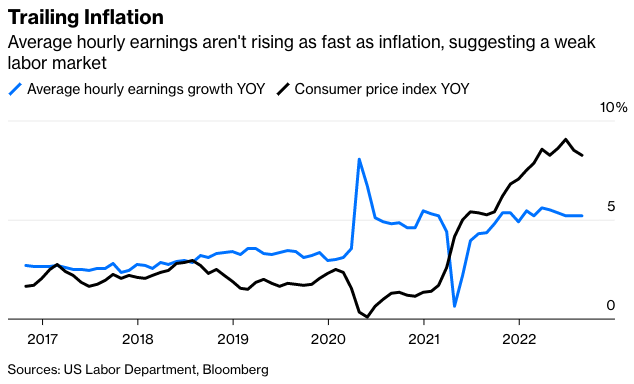

If there really isn’t any slack in the labor market, then why are real wages falling? Corrected for inflation, average hourly pay in August had fallen 2.1% this year, with the year-over-year jump in the consumer price index at 8.2%. The many employers who scrambled to add employees are now reluctant to cut staff even as the economy slips on concern that they may not be able to find workers when things turn around.

The recent weakness in productivity growth—and actual declines in the first half of this year—adds fuel to the fire since it takes more hours worked to produce the same output. In the first quarter, output per hour worked fell at a 7.4% annual rate and by 4.1% in the second quarter.

Furthermore, immigration, which can substitute for native-born workers, has slowed to a trickle. From 2019 to 2021, annual immigration dropped from 1.3 million to 505,000. Also, the rapidly aging postwar babies, now age 58 to 76, are dropping out of the labor force as they retire. The labor participation rate for those 65 and older is 19.1%, compared with 82.8% for those in prime working ages, 25 years to 54 years.

My analysis indicates that current labor market stringency isn’t due to robust demand for workers but because Americans are limiting the supply after the pandemic. After staying at home for two years due to the lockdowns, many people became accustomed to working remotely and putting in fewer hours while others dropped out, retiring early. In late September, office occupancy as measured by workers at actual desks was only 47.5% of early 2020, according to Kastle Systems.

Many switched to part-time from full-time work. In August, 21 million worked part-time because they wanted to while a declining number of part-timers—4.1 million—wanted full-time jobs but were only offered part-time work. Surveys by the Federal Reserve Bank of New York, among others, reveal that the pandemic-induced changes in attitudes toward work, with men, women, the young, middle-aged, full-time and part-time all wanting to work fewer hours than before Covid-19 struck.

Consumers can maintain their real spending in the face of falling real wages by liquidating assets, but that isn’t happening or likely. Much of the earlier three rounds of pandemic-related federal fiscal stimulus in 2020 and 2021 went into single-family housing, as Americans fled cities for suburban and rural areas, and into equities.