Given the flow of investor money into exchange-traded funds, it’s clear they’ve become very popular. ETFs trade throughout the day, like stocks, yet there are some key differences to keep in mind.

In the world of stocks, trading volume has always been a strong indicator of liquidity, or the degree to which stocks can be bought or sold in the market without affecting their price. However, when looking at ETFs, volume is only a reflection of what has traded—not what could have traded. ETF liquidity is easy to understand once you comprehend the three levels of liquidity for an ETF that may come into play when executing a trade.

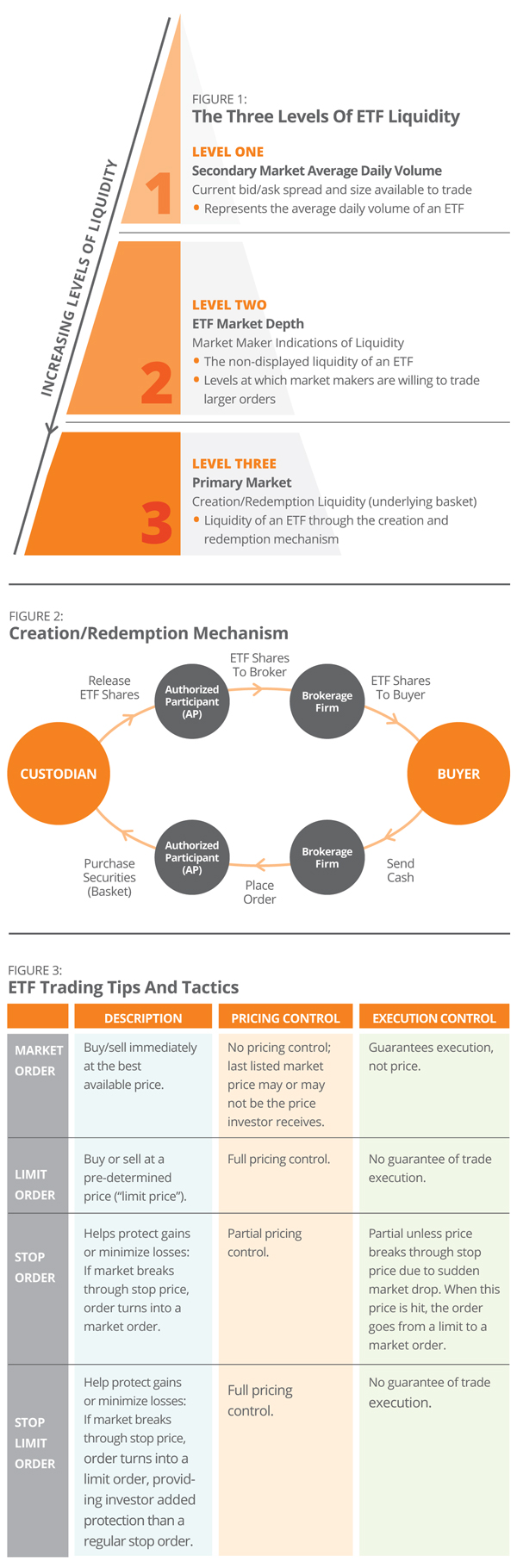

Level One: Secondary Markets

The simplest way for an ETF to trade is for a buyer and seller to be matched on the secondary market. For this to happen, a market maker publishes quotes that represent the price and number of ETF shares it is willing to buy and sell. The best of the quotes is known as the National Best Bid and Offer (NBBO) quotation. The difference in the bid and offer (also known as ask), is the spread. The spread is the payment the market maker receives for matching the buyer and seller of the ETF.

Differences in the bid-ask spreads among ETFs can have a meaningful impact on both trading cost and total return, so investors will want to take them into consideration when making investment decisions.

Level Two: Market Depth

The size and prices that are displayed through the NBBO are not the only quotes an investor can use. For most ETFs, market makers will publish quotes beyond the NBBO, helping to provide market depth. Market makers do this so that larger trades can be executed while covering the costs of providing the liquidity. There are a few ways to access this liquidity. One is to use a limit order to direct your broker to buy or sell ETF shares at a price beyond the NBBO, breaking up a trade into smaller trades, or contacting a broker-dealer’s ETF block desk, which handles large purchases and sales of ETF shares.

Level Three: Primary Markets

The heart of ETF liquidity is the primary market. This is where the “creation and redemption mechanism” comes in. The volume of the underlying securities is a source of liquidity for the ETF.

As illustrated in Figure 2, when demand for the ETF shares exceeds supply, a creation ensures there is sufficient inventory to fill an investor’s order. In ETF share creation, a firm authorized to purchase securities to create more ETF shares—known as an authorized participant (AP)—assembles a portfolio (or “basket”) containing the ETF’s current holdings. The authorized participant turns over the basket to the ETF custodian, who is responsible for holding it. In return, the custodian delivers ETF shares that can then be bought and sold in secondary markets, generally in blocks of 50,000 or 100,000 shares.

ETF share redemption reverses this process when the excess supply of ETF shares needs to be removed from the marketplace. The creation and redemption process helps keep supply and demand in balance, leading to an ETF share price that is generally in line with the value of the underlying securities.

Trading Tips and Tactics

There are a few simple steps that can give investors greater confidence in placing ETF trades (see Figure 3). While there are no hard-and-fast rules that apply under all circumstances, different situations and investor objectives call for differing tactics. No one approach is best in all situations, so it’s important to understand the potential benefits and limitations of each and choose the one that best fits the specific circumstance.

Call On ETF Capital Markets

ETF capital markets experts at issuers and broker/dealers are available to guide you through your ETF trading strategies, help bring about a positive trading experience, and achieve the best execution to help meet trading objectives.

Matt Lewis is vice president, head of ETF implementation and capital markets at American Century Investments.