None of the criticisms levied over the years against indexing has undercut the primary advantages of passive investing: It’s cheap, simple and avoids the futility of stock picking. Still, you have to give the opponents credit for persistance. They keep trying to convince investors that it is a poor approach to asset management.

I calculated last year that more than $80 trillion in equities worldwide was actively managed, which shows why active managers want to protect their franchise from further erosion. Since the 2008-2009 financial crisis, about $1.8 trillion has moved out of active funds, while $2 trillion moved into passive. This makes for an incredible chart on capital flows.

Even so, the criticisms are worth considering, if only to sharpen one’s thinking. In particular, the claim that indexing is dangerous because it represents a highly concentrated stock risk. In many major indexes that are weighted by market capitalization, such as the Standard & Poor's 500 Index or the Nasdaq 100 Index, the six high-flying “FAANMG” stocks have gained disproportionate influence. A recent MarketWatch column asked, “How much of your retirement savings are you now gambling on the fortunes of just six companies? If you’re holding them in an S&P 500 stock market index fund, the answer is: About a quarter.”

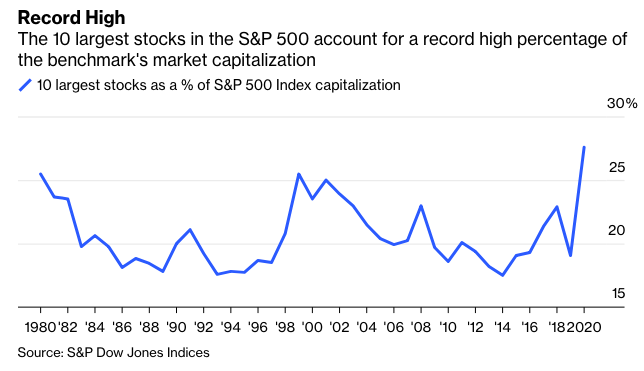

I reached out to Howard Silverblatt, senior index analyst for S&P Dow Jones Indices, for more color. He noted that the 10 largest stocks in the S&P 500 accounted for 27.6% of the index’s capitalization. That makes the benchmark the “most top-heavy index” since the 1960s, according to Silverblatt. That may seem concerning, but history shows it isn’t. Year-end data Silverblatt shared going back 40 years showed the highest concentration of the top 10 stocks ranged from a low of 17.5% in 2014 to a high of 25.5% in 1980. That puts the current weighting a little above the range.

That high concentration to begin the 1980s did not prevent the market from seeing substantial gains that decade. The recovery from the 1970s bear markets and the double dip recession that began the 1980s eventually gave way to increased breadth, or greater market participation. In other words, as the economy helped small and mid-sized firms, the top-heavy index concentration decreased.

The bigger point is that it’s not rare for a small group of stocks to account for a large percentage of the S&P 500. What is important is the relative performance of those 10 stocks to the other 490 stocks. The ratio fluctuates based on which group is outperforming, resulting in a continuous battle between mega cap stocks and the merely large and mid-sized stocks.

Consider just some of the many variables affecting this relationship. For example, when overseas economies are soft, larger international companies may be less appealing to investors. Alternatively, a robust global economic expansion does the opposite, creating more opportunities for bigger companies than firms that lack an international reach.