A simple definition of investment diversification is conveyed in the overused statement, “Don’t put all your eggs in one basket.” The basic buy-and-hold, set-it-and-forget-it style of investing is often premised in a 60 percent global stock and 40 percent bond allocation (known as “60/40”) and sold as enough diversification to handle whatever market turmoil might come your way over the long term.

Two major shortcomings spoil this view of investing. First, what is the long term? From 2000–2010 (the lost decade), the U.S. stock market did not make anyone money. We observed 10 years of varying degrees of market volatility and no return. We have found that most investors, ourselves included, aren’t interested in leaving 60 percent of their money in assets that don’t add value for a decade.

A second and less obvious flaw of traditional “diversification” is that its basic assumptions are defective. Why? Because they assume that when stocks fall, bonds will go up and provide risk mitigation, and when U.S. stocks fall, stocks in other countries will go up, thereby also providing risk mitigation. These negative correlation assumptions do not necessarily hold true, especially as it is commonly and erroneously expected that these correlations remain static over time.

These mistaken assumptions can lead to some painful outcomes. Anyone who lived through 2008 will recall that the S&P 500 dropped 37 percent that year. European stocks plummeted 41 percent and emerging market stocks were cut down nearly 50 percent. Owning all 3 of these broad asset classes as “diversification” didn’t provide investors any form of downside risk management.

More recently, in early 2018, the S&P 500 fell 10 percent in short order. Bond prices also dropped. The negative correlation assumption of the two simply did not work. This happens much more frequently than most would like to believe.

This isn’t to say that holding a diversified group of asset classes doesn’t reduce risk. It does reduce volatility compared to holding just the more volatile asset classes, but drawdowns can still be painful. So holding onto a mix of assets can be too simple a view and doesn’t protect investors during periods of high stress and when the correlation of asset classes spikes up.

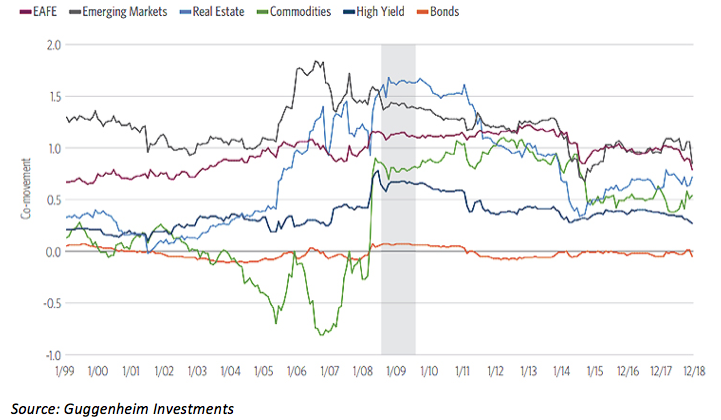

Guggenheim Investments published fascinating research documenting shifting correlations. Their chart shows the co-movement of the S&P 500 and different assets over the past 20 years ended December 2018. A measure of 1 or above means that assets are moving strongly in the same direction as U.S. stocks. The shaded area highlights when stocks were crashing in the 2008 period. This is exactly when the co-movement of commodities and bonds jumped up. Translation: All the eggs in all the baskets made a mess of the “diversified” portfolio.

All Eggs In All The Baskets

Co-movement of the S&P 500 and different asset classes over the past 20 years.

What is “True Diversification”?

We recommend looking beyond traditional asset classes, and holding alternatives whose sources of risk are truly differentiated from mainstream stocks and bonds. Managed futures strategies, for example, and volatility managed alternative strategies are two ways to accomplish that.

Further, we also recommend employing a tactical approach to buying and selling. Rather than defaulting to a “long-term” time horizon and risking a decade of unproductive investing, we exercise a rules-based, quantitative and tactical approach. We aren’t afraid to sell and get out of the way when a trend turns down and then use our rules to define when to get back in. Our process seeks to avoid the occasionally painful co-movement of asset classes rather than assuming (hoping!?) that diversification will save our clients.

Portfolio Positioning

Given the focus of this commentary, it may come as a surprise when we tell you that our strategies sold out of all risk-on classes in October and November, only to buy long government bonds in December. Didn’t we just make the case that the low or negative correlation assumption for stocks and bonds was an unreliable one? It is. Our alternative approach, though is to use rules to observe when an asset class is declining and when it is rising, and to react with discipline to what the markets are telling us.

In October of 2018 as U.S. stocks began to fall, bond prices were falling too—including the “safe” U.S. government bonds.

Our process kept us out of most of that. Then in early December, stocks really began to collapse in what turned into the worst performing December for U.S. stocks since the Great Depression. It was during this period that the flight to quality and into U.S. government bonds began. In this case, the negative correlation was clear and our trend-following process reported it loud and clear.

We don’t make predictions about what will happen to the U.S. economy and its stock market. We don’t rely on assumptions either. We do think it makes sense to build an ark before the rains start. For us, true diversification isn’t holding a risky stock allocation and a low-yielding bond allocation and believing that is enough. Instead, our rules-based approach depends on dynamic and tactical buying and selling to cut out downside risk and participate in uptrends.

Right now, our first buys are in preferred stock mutual funds, which are participating in the upside gains of stocks with less volatility. That said, we will sell these when our rules identify a shift back to the downside. True diversification is a process, not a set of assumptions.

Terri Spath, CFA, CFP, is chief investment officer at Sierra Mutual Funds.