We have a question to ask you: when it comes time to buy, will you?

It’s fair to guess that you will not want to buy when it comes time to buy, so the question really is: do you have a process and, importantly, the discipline to do it?

What Just Happened?

On a daily and even hourly basis, investors and every day citizens are worried, and they are struggling to determine what the COVID-19 virus means for their personal health and their personal finances. With no shortage of uncertainty, a rush to the exits has fed all forms in a swift and scary global sell-off of stocks. Like the undefeated team finally losing at home, the longest bull market in history has stunned its fans and sucked all the enthusiasm out of the rest of the season.

If a bear market means a 20% drop from a high, there can be no debate we are now firmly in a bear market. Fear shrinks lives and it also shrinks investment portfolios, this time to the tune of a 30% loss in stock market value in 18 trading days in a selling frenzy that many seem to worry is bottomless.

As the uncertainty sinks its claws in deeper, it should be no surprise that corporations are beginning to face very real contractions in sales and earnings, and therefore cuts for 2020 earnings estimates. Ten weeks ago, heads of U.S. corporations were printing 8% to 9% year-over-year earnings gains for 2020, but those numbers have been chopped. Indeed, some companies have added to the confusion by excising any 2020 earnings estimates at all, making it that much harder for market participants to get any clarity or “2020 vision.”

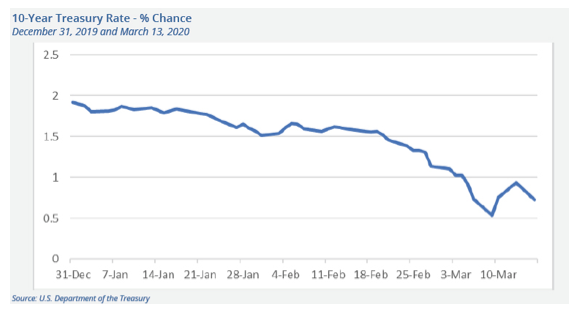

We have many examples of the rampant investor fear, including this one: investors are clutching to find their security blankets, snatching up Treasury bonds. The heavy demand for safety is pushing Treasury bond prices up and yields down. Earlier in March and for the first time ever in the history of the United States, the yield on the 10-year Treasury fell below 1%. In fact, that yield has remained doggedly below that key level for most of March.

It feels quite easy to hit the sell button, which is why we ask again: when it comes time to buy, will you?

A Process For Selling

Right now, our portfolios are sitting on a whole lot of dry powder after acting in an orderly way on sell signals that our rules-based discipline generated in late February and into early March. Here is a brief summary:

• In the 7 days from February 19 through February 28, all our stops were hit for U.S. and international stocks resulting in a total exit during that period (with those asset classes careening down another 15% in March so far).

• Preferred stocks generally return less than common stocks, but with that comes about half of the volatility (as measured by standard deviation). However, preferred stocks still walk up the stairs and jump on the elevator down. During the last trading days of February, preferred stocks lost about 3%, also hitting our sell levels (and thereafter lurching down another 10% so far in March).

• High-yield corporate bonds also typically trend in the same direction as stocks, but with half or even a third the volatility of common stocks. Unlike the broad stock market, the high-yield corporate bond market has a much higher weighting towards energy companies. When Saudi Arabia boosted oil production earlier in March, energy prices lurched even further down pulling high-yield corporate bond prices with it. The rules-based process we follow, though, pushed out this asset class in the last days of February and first days of March (that asset class has also fallen another 8-10% since early March).

• As fear accelerated in the second week of March, a take no prisoners frenzy took over and even asset classes that are typically a safe place to hide were no longer providing protection. The prices for low volatility municipal bonds dipped enough to reach our sell signals with many registering high single digit percentages declines in just a few days.

Summarizing, an orderly sell discipline limited the impact from global equities, preferred stocks, high-yield corporate bonds and even municipal bonds in our portfolios and strategies.

So now what?

When It Comes Time To Buy, Will You?

We ask again, when it comes time to buy, will you? Will you really feel like buying when opportunity is at or as close to as good as it gets?

In other words: do you have a process and the discipline to follow it?

Human behavior and emotion are not useful substitutes for a disciplined process. Conversely, emotions can be a massive threat to financial health, as the students of behavioral finance have studied and documented in Nobel Prize winning papers.

The familiar chart below says it all. Optimistically, investors expect to make money investing and when those expectations are met, excitement, thrill and buying reigns supreme and converts into further buying.

When lofty hopes of making money are thwarted, complacency and denial begin to set in. Facing a bear market, anxiety, fear and eventually panic result in widespread selling. Sometime during the panic and eventual despondence the cycle of emotions produces maximum financial opportunity.

However, without a process in place, caution, worry, second-guessing and more override the opportunity to push the “buy” button.

Following rules for “when to sell” we currently have dry powder and stand ready to buy. Our “when to buy” framework is similarly rules-based, quantitative and reviewed daily with a goal of identifying the inflection points and then trend establishment to the upside.

We have seen this cycle of emotion before. Again, we ask: when it comes time to buy, will you?

With some confidence, we can say that you won’t want to buy when it is time to buy, so our process is to have a rules-based process ready and the discipline to just do it.

Terri Spath, CFA, CFP, is chief investment officer and portfolio manager at Sierra Investment Management Inc.