Investment flows, buying and selling, can impact prices and yields but are not the sole determinant of high-quality bond prices and yields.

Investment flows, buying and selling, can impact prices and yields but are not the sole determinant of high-quality bond prices and yields.

Classic drivers of bond yields — the economy, inflation, and the Fed — will likely outweigh the impact of buying and selling flows over longer periods of time.

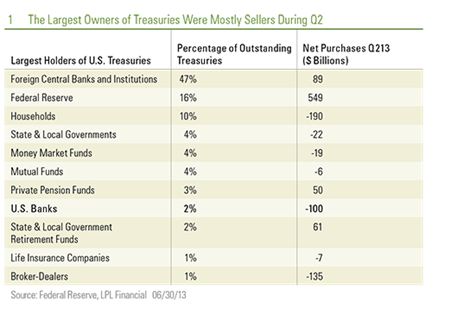

Who will step in to fill the void once the Federal Reserve (Fed) decides to exit the bond market? This is the persistent question on investors’ minds even after the Fed decided to postpone tapering, or reducing, bond purchases this past September. Investors fear that the Fed’s absence will lead to lower bond prices and sharply higher interest rates as the market struggles to find demand to make up for Fed buying. Investment flows from a particular investor group buying or selling, can impact prices and yields but are not the sole determinant of high-quality bond prices and yields. Recent history shows that simply tracking when the Fed is buying, or not buying, has not been a good predictor of bond prices and yields. In fact, Treasury prices often took the opposite expected reaction in response to Fed buying, or lack of it. For example, bond yields declined at the end of both of the Fed’s first two bond-purchase, or quantitative easing (QE), programs, QE1 and QE2. Alternatively, when the Fed began buying bonds for QE2, interest rates actually increased. Interest rates also increased from May of this year through early September despite a heavy dose of Fed bond buying. Although the Fed kept buying during the second quarter of 2013, most large Treasury holders were sellers, which contributed to bond market weakness in May and June. The Fed’s recently released Flow of Funds data is the most comprehensive snapshot of Treasury bond ownership. The report is issued with a lag and only covers the second quarter of 2013, but nonetheless provides a guide to who the largest Treasury buyers are [Figure 1].

The Role Of Foreign Investors And Major Treasury Holders

Foreign investors, the largest group of Treasury holders, continued to buy overall but at a greatly reduced pace. Foreign purchases of Treasuries during the second quarter were less than 20 percent of the average pace of the past two years. Foreign selling by Japan, the second-largest foreign owner of Treasuries, was the primary driver of weak foreign demand. U.S. banks, mutual funds, broker-dealers, money market funds, life insurance companies, and households—a catch-all category that represents individual investors as well as endowments and domestic hedge funds, to name a few—were all sellers during the second quarter, according to Fed data. The selling created price pressure that offset the impact of Fed buying. Only private pension funds and state and local government retirement funds were Treasury buyers along with the Fed during the second quarter of 2013. Investment flows did impact yields and highlight why there is cause for concern when the Fed eventually leaves the market, but it is important to note that flows are not the only driver of bond yields. In fact, we would argue they are only a secondary driver and merely exacerbate or dampen existing price momentum.

Classic Drivers

Classic drivers of bond yields — the economy, inflation, and the Fed — will likely continue to outweigh the impact of buying and selling flows over longer periods of time. Recall in May of this year, Fed tapering concerns were confused with rate hike fears. Investors believed that tapering would be a prelude to sooner-than-expected interest rate increases, and use of the word “tapering” suggested the Fed viewed the economy as strong. In April, fed fund futures, a widely followed gauge of what the market is expecting from the Fed, indicated the bond market did not expect the Fed to raise interest rates until early 2016, but by early September, in conjunction with uncertainty over who would lead the Fed in 2014, futures pricing reflected an aggressive first rate hike expectation of December 2014. Moderation to a mid-2015 first rate hike expectation was a big factor in bond market stabilization over recent weeks. A much quicker start to Fed interest rate hikes was the primary driver of the recent sell-off and exacerbated by secondary factors that included not only selling flows but also expensive bond valuations and illiquid markets. Similarly, when the Fed ceased bond purchases in March 2010, bond yields began to decline as economic data deteriorated. When QE2 ended in June 2011, bond yields fell once again as the economy slowed and European debt fears intensified. Furthermore, from mid-2000 through the third quarter of 2001, bond yields fell steadily in response to a slowing economy and concerns that the Fed had raised interest rates too much. Treasury yields fell over the period despite no meaningful buying from the Fed and modest selling from foreign investors, households, private pension funds, life insurance companies, banks, and mutual funds — a majority of the large Treasury owners. We will continue to monitor investment flows from major Treasury owners, but a few factors suggest that even when the Fed exits the Treasury market, major players will likely continue investing even after a pause during the second quarter.

- Declining Treasury issuance. The improving budget deficit means the Treasury will be issuing fewer securities. The Treasury Department has already begun to reduce issuance by curtailing the dollar amount of certain auctions. This is likely to continue as the non-partisan Congressional Budget Office (CBO) projects a further narrowing of the budget deficit in the next few years, which will likely imply less Treasury issuance.

- A decline in the amount of high-quality bonds. The International Monetary Fund (IMF) anticipates that the global supply of top-rated bonds will decline by $9 trillion in 2016 from the pre-financial crisis peak. Following the financial crisis and European debt problem, the number of AAA-rated bond issuers has shrunk, and the trend is expected to continue. High-quality mortgage-backed securities (MBS) issuance is already substantially lower due to the rise in interest rates and reduction in both refinancing and new loan origination. This development reduces the amount of high-quality bonds over the near term. All else being equal, a lower supply of higher quality bonds suggests firmer prices.

- Better valuations. The subsequent rise in bond yields has put bond valuations on much better footing, especially since the bond market has a much more balanced view of when the Fed may start to raise interest rates. Japanese investors returned in force to the U.S. bond market in September, purchasing over $600 billion in bonds, and life insurance companies along with private pension funds, who typically buy to balance long-term liabilities with long-term bonds, may continue or resume purchases given the better valuations.

To be sure, investment flows are a potential risk when the Fed ultimately exits the bond market. An example is evident among some emerging market countries that have recently turned toward protecting their domestic currencies and not buying Treasuries, creating a source of lower demand. In addition, Wall Street firms that trade and make markets in bonds have become less active participants due to increasing regulatory requirements and may be less likely to support bonds or certain types of bonds. However, we view these risks as potential headwinds and not a major driver of bond yields. We will continue to monitor investment flows but do not believe that the Fed’s eventual withdrawal from the bond market translates into steadily higher interest rates. Fed interest rate hikes, economic growth, and the rate of inflation will continue to be the primary drivers of bond yields. The onset of rate hikes in coming years coupled with still-low yields suggests that interest rates are still headed higher, but gradually. A repeat of the recent bond sell-off is unlikely given better valuations and more balanced Fed expectations.

Anthony Valeri has been with LPL Financial since June 1993. As Senior Vice President and Market Strategist, Valeri is a member of the Research department’s tactical asset allocation committee and is responsible for developing and articulating fixed income and general market strategy.