There are many different and quite attractive approaches to the construction and management of an investment portfolio. This brief discussion focuses on one of these, Tactical Asset Allocation (hereafter referred to as TAA). TAA is not better or worse than other investment approaches. Instead it is different, with certain advantages and disadvantages. We touch on each below, but first a brief definition.

What Is Tactical Asset Allocation

TAA is a process for constructing and managing balanced portfolios that focus almost exclusively on active asset allocation. These active decisions can focus on quite different levels of granularity. At the highest or coarsest level, the active asset allocation decisions could be between stocks and cash or between stocks and bonds. At the most granular or finest level, the active asset allocation decisions could be between one narrowly defined industry segment and another, e.g., between the energy industry and the healthcare industry or between real estate and telecommunications.

The investment objective of TAA is to add value both with respect to return-enhancement and risk-mitigation through these active asset allocation shifts. Moreover, TAA distinguishes itself from other investment approaches by the frequency and timing of these active allocation decisions. In general, the frequency of these portfolio changes results in a high level of turnover and therefore TAA portfolios are considered to be highly tax inefficient. Typically, investors who live in high tax states (e.g., New York or California) and who are exposed to the highest marginal state and federal tax brackets, tend to avoid or minimize the use of TAA portfolios in their taxable accounts.

Relative Advantages

When designed properly and executed successfully, TAA portfolios have two main advantages. First, risk mitigation during severe bear markets. Second, return enhancement when markets are realizing a higher than normal level of trending. We touch on each of these in turn.

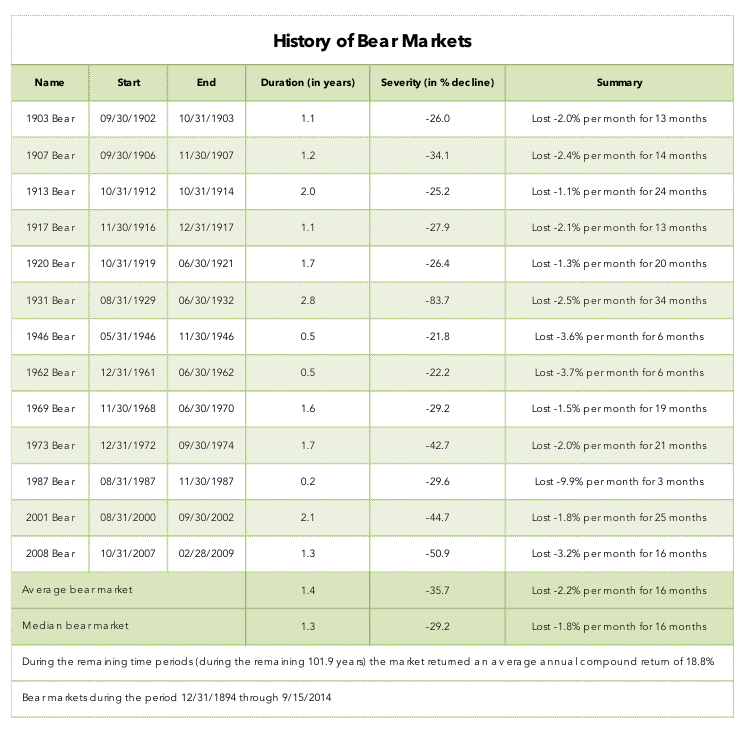

Risk mitigation during severe bear markets. TAA’s primary investment objective is to mitigate a balanced portfolio’s decline during severe bear markets. It is important to appreciate that the objective is to mitigate and not eliminate severe declines. The benefit of such mitigation is most clearly understood by reviewing the history of bear markets. The following table shows the history of such declines for the U.S. stock market as defined by the S&P 500 Index.

Several observations may be particularly helpful.

- A new bear market starts once every 9.2 years, on average.

- The average decline is -35.7 percent.

- The typical bear lasts for 1.4 years (or 17 months).

- The most recent bear market started 6.9 years ago (back on 10/31/2007).

- When the market is not experiencing a bear market, the average annual compound return is 18.8 percent per annum.

Return enhancements when markets are realizing a higher than normal level of trending. TAA’s secondary objective is to provide superior performance (out-performance) when markets are experiencing a higher level of trending than is normally experienced. The phenomenon known as trending is best described as the market’s propensity to keep doing what it’s been doing, e.g., if the market has been going up, then to keep going up, or if the market has been going down, then to keep going down.

Why might markets trend? Consider a simple example.

- Central banks pump money into the economy in ever increasing quantities, year after year with the objective of stimulating real economic activity (jobs and business expansion).

- But the only outlet for the central bank money-printing is found in higher asset prices (higher stock and bond prices).

- The result is strongly trending markets - print money, stocks rise, print more money, stocks rise some more, and so on.

- Over time, stocks become disconnected from fundamentals, having been driven primarily by money printing.

- Stock prices are now trading at levels driven primarily by unsustainable and artificially low interest rates and risk premia.

- Eventually, central banks end their money-printing.

- Interest rates and risk premia begin to rise.

- As they rise, stock prices decline.

- The result is strongly trending markets, but now in a downward direction - interest rates and risk premia rise, stock prices fall, interest rates and risk premia rise some more, stock prices fall some more, and so on.

Relative Disadvantages

The primary disadvantage of TAA is something called whipsaw. In general, TAA portfolios are unusually exposed to under-performance when markets are experiencing a lower than normal level of trending. When markets are aimless, perhaps alternating rapidly between up and down, TAA portfolios have a hard time deciding how to be invested and whipsaw results. Such market environments are characterized by volatility but with little to no direction.