Companhia de Bebidas das Ameri-cas is the kind of stock that portfolio managers like to talk about. Also known as AmBev, Brazil's largest producer of beer and soft drinks, its shares more than doubled in price in 2009 and analyst consensus estimates call for 22% growth in the company's earnings in 2010. "If you can't make money selling beer on the equator, there's something wrong," quips James Moffett, manager of the Scout International Fund, explaining why he thinks AmBev, his fund's best performer last year, should continue to do well in 2010.

AmBev is more than a play on Brazil's growing thirst for beer. It also represents the potential success of companies around the world positioned to tap into a growing emerging market consumer base. To Moffett, the best way to reach those consumers is by investing in the larger mid-cap and smaller large-cap spaces, areas that offer exposure to global companies but leave room for growth.

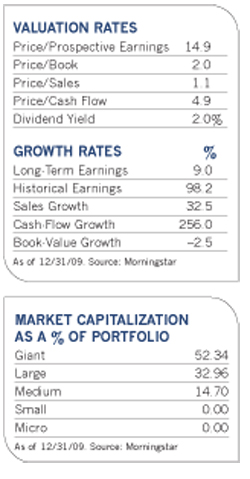

The 68-year-old Moffett, who has managed the fund since its inception in 1993, pinpoints broad economic trends and then looks for companies poised to take advantage of them. Those companies must have a history of above-average earnings growth and healthy balance sheets. Scout International spreads its allocation widely among 92 holdings, with the largest one representing less than 2% of assets. The fund's measured approach, along with a reasonable 1% expense ratio, has helped it earn a five-star Morningstar rating, as well as top ratings from Lipper and Standard & Poor's.

Leading The Charge

As Moffett sees it, the worldwide economy is in the process of turning around, and the two main drivers are the U.S. and China.

In the U.S., he says, it looks as if the economy has bottomed out and will continue to improve gradually. While reports of tapped out consumers and huge budget deficits continue to dominate headlines, corporate balance sheets are in better shape than they've been for a long time. The overall health of corporate America lays the groundwork for mergers and acquisitions and capital expansion, particularly in technology.

In China, government efforts to rein in inflation by curtailing bank lending have raised what Moffett considers an inordinate amount of speculation about future growth. "All that means is that they took their foot off the pedal a little bit. Instead of growing 10%, the economy might grow at around 8%. There isn't going to be any major shortfall," he contends.

Although he sees China as one of the drivers behind economic growth around the world, he won't invest directly in companies based there because of what he considers their poor corporate governance standards and lack of transparency. "There's also a lot of government control. When the government tells banks to lend, they comply. When it tells them to stop lending, they do that. Many companies are also partially owned by the government. From an investor's point of view, all that government intervention creates additional risk," he says.

He also thinks the market is showing signs of overheating. People used to ask him how the fund was positioned in terms of sectors and countries. Now their big question is how much the fund has in China. "At a gut level, that's a warning sign," he says.

Instead, he prefers to get China exposure by focusing on companies that do a significant amount of business there. Many of them are based in Brazil, whose exports to China now exceed those it sends to the U.S. Moffett's fund has a roughly 17% exposure to emerging market countries, with 4.5% in Brazil.

Many of his indirect China plays focus on raw materials and energy companies, including Australia's BHP Billiton, one of the world's largest producers of iron ore, aluminum, specialty metal and coal. The fund has also increased its weighting in raw materials companies such as Vale, the Brazil-based metals and mining concern that produces industrial materials such as iron, nickel, coal and copper and also has investments in energy and steel businesses. South Korea's POSCO, the world's fourth-largest steel maker, is another commodity-related play with ties to China. The company plans to expand capacity by 25% over the next few years as the global economy improves.

Moffett has also upped his indirect banking exposure to China through banks that do business there, such as Standard Charter. Based in the U.K., the bank has seen strong earnings growth thanks to its presence in Asia and other emerging markets and also thanks to its ability to keep a tight rein on costs. Another U.K. bank the fund owns, HSBC, has significant operations in both Hong Kong and mainland China.

As for individual countries, the fund is underweight relative to the benchmark MSCI EAFE index in the U.K. "Frankly, the country has lost its capitalist edge since Margaret Thatcher left office. There are just better places to invest," he says.

He's also wary of Japan. "The thing that helped us the most in country allocation last year was not owning Japan," he says. "That's something we're in the process of reviewing now. Companies there pay a lot more attention to profitability than they did when I started the fund 15 years ago and there's a new finance minister in place. We could see some positive surprises going forward."

Canadian companies, which aren't part of the index, occupy about 6% of the portfolio. In part, the allocation is a play on raw materials through companies such as Imperial Oil, one of the country's largest producers of crude oil and gas, and Enbridge, a leading energy transportation, distribution and services company. He also has holdings in the financial sector, including Toronto-Dominion Bank and the Royal Bank of Canada. "The U.S. has always looked down on Canadian banks as too conservative," he says. "But good regulation, a cleaner mortgage market and no esoteric derivatives have kept them out of trouble."

The fund also has a small allocation toward U.S. stocks, which aren't included in the index. The exposure underscores his belief that the U.S. economy "will probably do better than Europe's this year."

In Europe, where the fund has about 55% of its assets, economic problems and historically high budget deficits in Greece, Spain and Portugal "will be a drag on the rest of the European countries for quite a while and prolong the recovery process," he says.

Earlier this year, Greece avoided a potentially disastrous default on its debt by raising cash with a new bond issue. Although other countries in Europe have pledged support for their less fiscally sound neighbors, concerns remain about the impact the financial headwinds could have on the rest of Europe.

The fund's only exposure to Greece is through Hellenic Bottling, the second-largest Coca-Cola bottler and distributor in the world. Moffett says the company is largely insulated from the country's financial woes because it does business in a variety of locations, including the growing Eastern European market. Another holding from the troubled region, Spain's Banco Bilbao Vizcaya Argentaria Bank (BBVA), is "a well-run bank that happened to be based in a country with a bad economy. It has very conservative lending practices and higher reserve levels than most banks in the U.S." BBVA has operations in Mexico and owns Compass Bank in the U.S. through a 2007 acquisition.

To Moffett, the weakening of the euro since last year is a double-edged sword. It's a negative for investors who will not have the benefit of a currency tailwind that they've enjoyed over the last several years. At the same time, currency translation could help boost revenue for companies in Europe that do lots of business elsewhere such as Germany's Siemens, which distributes its electrical engineering services and electronics products throughout the world. On the other hand, retailers and others without such geographic reach are likely to suffer.

If economic growth in the region continues to lag that in other parts of the world, Moffett thinks the euro could weaken further against other major currencies. Nevertheless, he does not hedge currencies in the fund because it increases transaction costs. Since Scout International is essentially a hedge against the U.S. financial markets, he believes that "it doesn't make sense to hedge a hedge."

Even in emerging markets with more robust economic growth than Europe, financial markets will likely remain choppy, he says. "You need to remember that financial markets and the economy are sometimes not linked. We saw that last year from March until September when the markets did very well before the economy had turned. We could see a similar situation during the course of this year."

But overall he believes it's going to be a fairly good year for worldwide economies and for the fund. "We had a good year last year, with a 35% return. This year, we're hoping for 10% or 15%. But no promises."