Investors tend to watch inflation closely, and for good reason. The whole point of investing is to increase the value of money, so keeping pace with rising prices is crucial. But for a growing number of U.S. investors, a healthy regard for inflation has been replaced by anxiety that the U.S. is on the brink of surging prices.

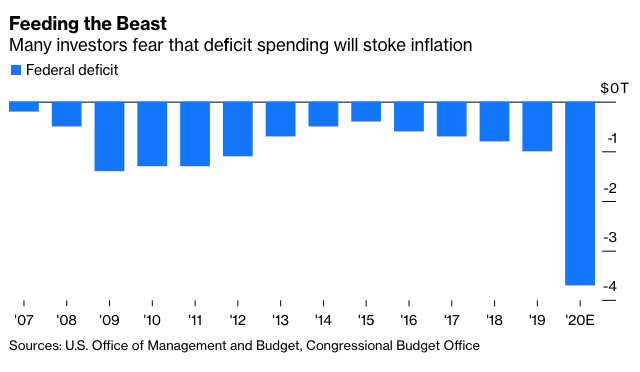

Admittedly, the current environment seems fertile for inflation. A lot of money is floating around. The Federal Reserve has injected roughly $3 trillion into the economy so far this year. Add to that the projected federal budget deficit of $3.7 trillion for 2020, according to the Congressional Budget Office, nearly triple the previous record of $1.4 trillion in 2009. Meanwhile, Covid-19 is disrupting supply chains and hastening the breakdown of global trade. The cocktail of ample cash and shrinking inventories is a recipe for higher prices.

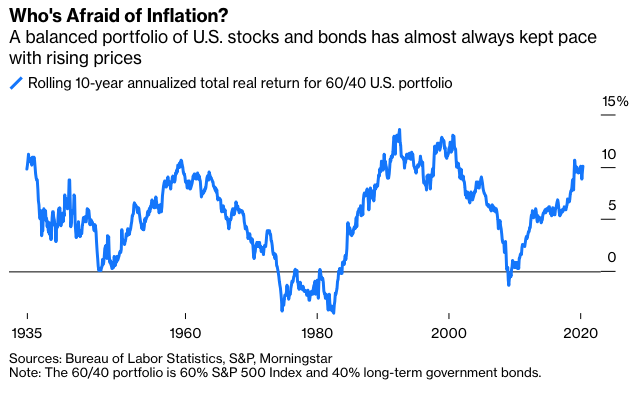

Still, the impact on portfolios is far from clear. There are few historical examples to point to because inflation has rarely been a threat to U.S. investors. A traditional 60/40 portfolio of U.S. stocks and bonds, as represented by the S&P 500 Index and long-term government bonds, has produced a real, or net of inflation, return of 5.8% a year since 1926 through May, including dividends, the longest period for which numbers are available. It also generated a positive real return 89% of the time over rolling 10-year periods, counted monthly.

In addition, almost all the 10-year periods of negative real returns were clustered around a single decade: the notorious stagflation of the 1970s, a combination of runaway inflation and tepid economic growth that inflation hawks worry about today. Inflation, as measured by year-over-year changes in the consumer price index, began to creep up during the late 1960s. By the end of 1969, the inflation rate had swelled to 6.2%, more than three times its long-term average since 1871 at the time, according to numbers compiled by Yale professor Robert Shiller. And that was just the beginning. It would eventually climb to 15% in 1980 before finally falling to a more normal level in 1983.

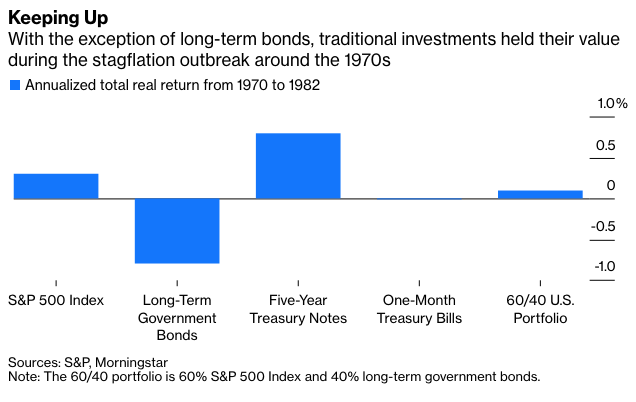

So how did the trusty 60/40 portfolio hold up against stagflation? Surprisingly well. It produced a nominal, or gross of inflation, return of 7.8% a year from 1970 to 1982, and a real return of 0.1% a year. In short, it kept up with inflation.

But the more interesting and instructive bits are in the details. As it turned out, the parts didn’t contribute equally to the whole. The stocks held up well, producing a real return of 0.3% a year during the period. While it’s never safe to generalize based on a single anecdote, it makes intuitive sense that stocks might be a good inflation hedge. As University of Pennsylvania professor Jeremy Siegel noted in Stocks for the Long Run, his 1994 homage to the market, stocks “are claims on real assets, and real assets will rise in value with an increase in the general level of prices.”

Notably, stocks did just that while battling two headwinds inflationistas fear, namely declining earnings and contracting valuations. Real earnings declined by 1.3% a year from 1970 to 1982, while the price-to-earnings ratio shrank 2.7% a year, based on 12-month trailing earnings. And yet, an investment in stocks held its value.