There is an old saying that successful real estate investors follow three important considerations: location, location, location. When the real estate market is booming, one can make good returns in marginal properties, but those investments are unlikely to hold their value during a downturn in the market.

The same can be true of equity investing during the past several years. When the global economy was binging on credit, it was fine to invest in marginal locations’ equity markets. However, as the global economy slowed, those fringe markets have disappointed, and “location, location, location” has proved as important to equity performance as it is in real estate.

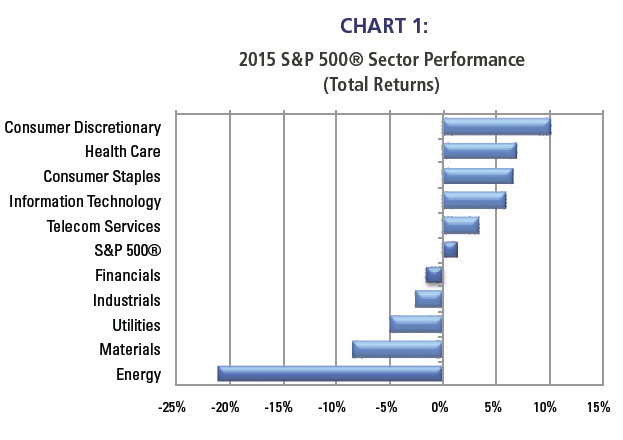

The equity world’s equivalent of A+ office space is the US consumer sector. It’s not an accident that Consumer Discretionary stocks were 2015’s best performing sector in the US (see Chart 1) because the US consumer has been the strongest and most stable part of the global economy. Our overweight of Consumer Discretionary stocks was a major fillip to our performance.

Source: Bloomberg Finance L.P.

Mute the TV

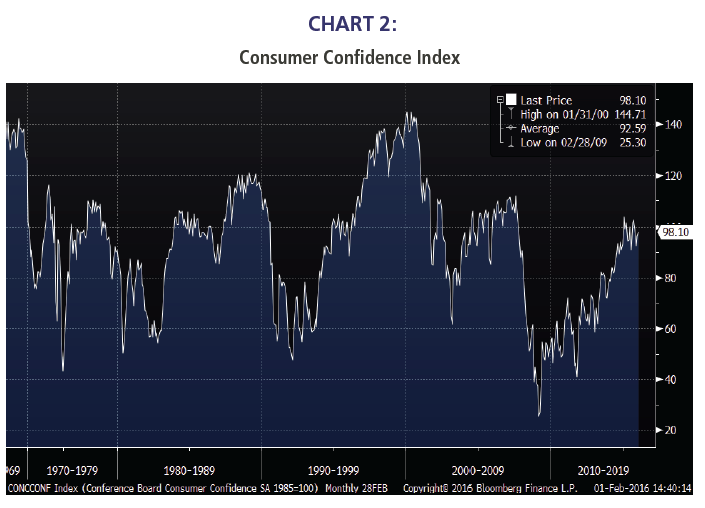

Our Year Ahead report emphasized that 2016’s political rhetoric was likely to give very misleading signals about the health of the US’s household sector. Although politicians from both parties suggest the US household sector is in terrible shape, households themselves do not seem to agree at all with that assessment.

Chart 2 shows the Conference Board’s Consumer Confidence Index. The latest reading (98.1) is close to the cycle high and is well above the long-term average (92.6). A reading above the long-term average indicates that consumers are more confident than “normal”. One would never know that by listening to the political pundits. Rather, one might think that the US household sector was in terrible shape. The outperformance of consumer stocks demonstrates the stock market muted the TV and paid attention to actual data like consumer confidence.

Source: Bloomberg Finance L.P.

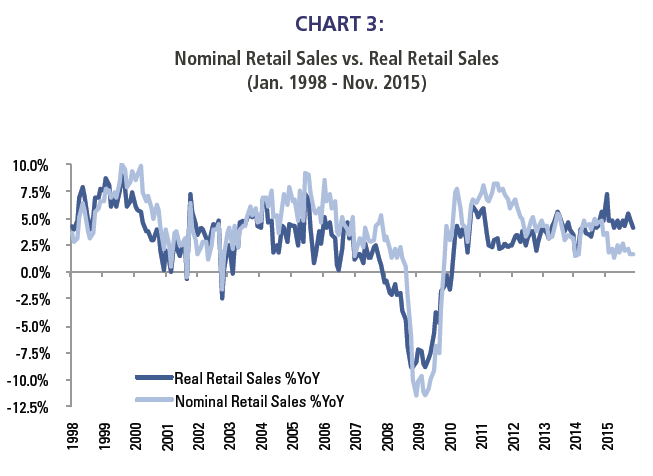

The US consumer is benefitting from what we have called the “Wal-Mart World”. Excess global capacity is putting pressure on product prices as countries compete for market share within the stable and healthy US consumer market. Effectively, the entire world is acting like a giant Wal-Mart, and is offering consumers lower and lower prices.

The Wal-Mart world is starkly evident in a comparison of US nominal and real retail sales. For the first time in the history of monthly consumption data, real retail sales (units) are growing faster than are nominal retail sales (which include prices). So, consumers are buying, but price competition is constraining nominal retail sales.

Source: Richard Bernstein Advisors LLC, Bloomberg Finance L.P.

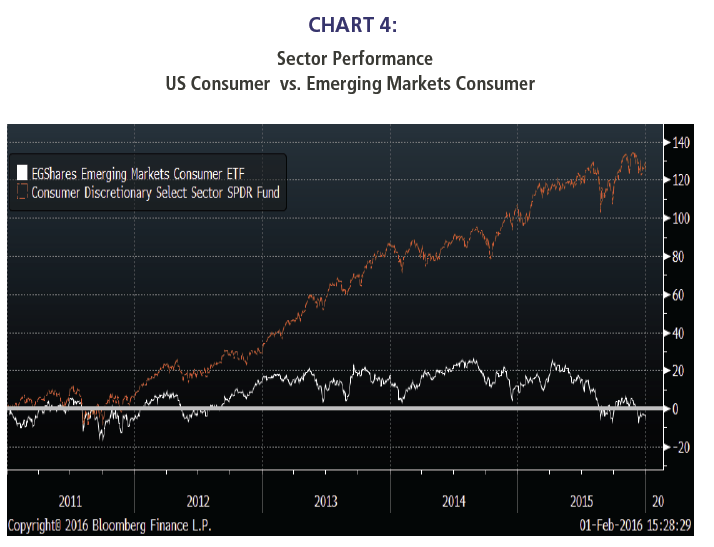

Emerging consumer vs. US consumer

The emerging market consumer has been one of the most discussed growth stories of the past decade or more. Investors believe that US consumers are sated and over-leveraged, but emerging market consumers provide great growth opportunities because of their high savings rates and growing incomes. Unfortunately, sector performance has reflected the exact opposite, and US consumer stocks have outperformed emerging market consumer stocks by more than 1800 basis points per year over the last five years (see Chart 4).

This is understandable when one looks at the secular depreciation of emerging market currencies. Because currency strength or weakness measures purchasing power, a country’s standard of living improves as its currency appreciates and deteriorates as its currency depreciates. Accordingly, when the US dollar was depreciating, some observers pointed out that the US’s standard of living was weakening.

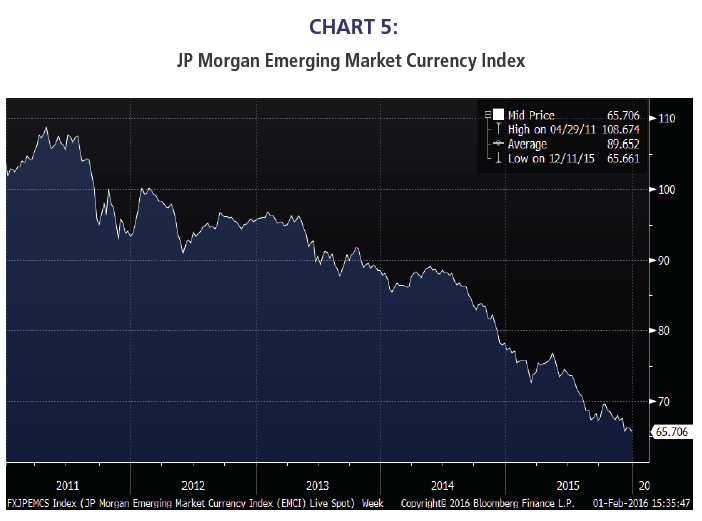

Chart 5 shows the JP Morgan Emerging Market Currency Index, and it has consistently fallen over the last five years. It is curious that investors were pessimistic regarding the outlook for US consumers when the US dollar was falling, but have remained bullish on the prospects for emerging market consumers despite the precipitous fall in EM currencies.

Source: Bloomberg Finance L.P.

Source: Bloomberg Finance L.P.

Location, Location, Location

The moral of the story is that it’s fine to invest in fringe markets when the world is binging on credit, but investors need to be more circumspect when the global economy slows. Economic cyclicals tend to outperform when the economic cycle revs up, but underperform when the economic cycle slows.Credit cyclicals outperform when the credit cycle revs up, but underperform when the credit cycle slows. Unfortunately, fringe markets are significantly exposed to both cycles.

Richard Bernstein is CEO and chief investment officer of Richard Bernstein Advisors LLC, an independent investment adviser. RBA partners with several firms including Eaton Vance Management and First Trust Portfolios LP, and had $3.1 billion collectively under management and advisement as of December 31, 2015.