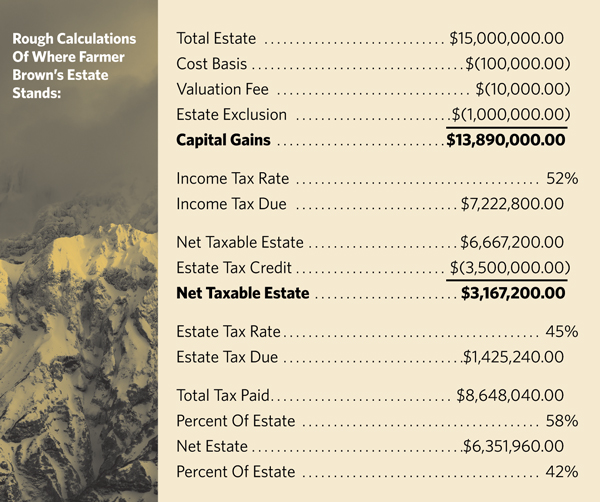

Farmer Brown, a widower, owns the 200-acre family farm he bought from his parents in 1960 for $100,000. Because the farm is located in what was once a rural community and is now a suburban community, the value of the farmland is much higher. If converted into lots for houses, it could fetch $150,000 per acre. If we assume that only half the land is buildable, Farmer Brown is still sitting on top of a $15 million asset.

Now here come Senators Chris Van Hollen, Cory Booker, Bernie Sanders, Sheldon Whitehouse and Elizabeth Warren. In late March, they introduced the Sensible Taxation and Equity Promotion (STEP) Act, which broadly parallels a similar bill filed in the House of Representatives. Combined with the proposed changes in the income tax laws, this will have a huge effect on the tax burden on individuals and families in the United States. What’s more, it will be retroactive to January 1, 2021.

If STEP is enacted, any assets transferred either during a person’s lifetime or when that person dies will realize a net gain for income tax purposes. There is an exclusion for the first $1 million of gain when the asset holder dies, but only the first $100,000 in lifetime gifts by Farmer Brown will be exempt (this does not apply for assets given to a spouse). This also applies to transfers such as gifts to trusts (those that are not included in the transferor’s estate), and it makes the use of these trusts very costly.

Even if there is no transfer, all future irrevocable trusts would have to report gains on all of their appreciated assets every 21 years. Any trust formed before 2005 would report and pay taxes on this gain in 2026. Trusts with more than $1 million of assets (or more than $20,000 of gross income) would be required to provide a balance sheet and income statement and to list all trustees, grantors and beneficiaries to the IRS every year. This will require the valuation of hard-to-value assets like art, businesses, land and other unique assets, though there is an itemized deduction for the valuation costs.

Items transferred to charity, spouses, charitable trusts, qualified disability trusts and cemetery trusts are exempt from the tax. The gains on a personal residence would be exempt up to $250,000, or up to $500,000 for a married couple.

For transfers of illiquid property, such as farms and certain farm assets, you can pay the tax over a 15-year period. It would be interest-only for up to five years and then there would be 10 equal payments for the remaining 10 years. If you sold the property, you would have to pay in full. There would be a lien attached to any property, and that would likely prevent you from refinancing it without paying off the loan to the IRS. Any transfer tax owed when you die would reduce the estate value subject to estate taxes.

There would also be no $15,000 annual exclusion per donee as there is under the current gift tax rules. This means parents and grandparents who typically gift assets to their children and grandchildren will eventually reach the $100,000 lifetime exemption amount and have the remaining amounts subject to tax.

Bernie Sanders has also proposed significant changes to the income tax. His proposal would add four new income tax brackets for high-income households: with rates of 37%, 43%, 48% and 52%. The Sanders proposal would tax capital gains and dividends at ordinary income rates for households with income over $250,000 and would create a new 2.2% “income-based [healthcare] premium paid by households.” This is equivalent to increasing all tax bracket rates by 2.2 percentage points, and would raise the top marginal income tax rate to 54.2%.

Bernie Sanders has also proposed significant changes to the income tax. His proposal would add four new income tax brackets for high-income households: with rates of 37%, 43%, 48% and 52%. The Sanders proposal would tax capital gains and dividends at ordinary income rates for households with income over $250,000 and would create a new 2.2% “income-based [healthcare] premium paid by households.” This is equivalent to increasing all tax bracket rates by 2.2 percentage points, and would raise the top marginal income tax rate to 54.2%.

Now, back to Farmer Brown. He has to pay for a valuation of his property, and when the appraisers tell him the value (and present him with their bill, which is between $10,000 and $15,000) Farmer Brown promptly dies of a heart attack. In his will, he gives equal shares of his farm to his children, all of whom are successful in their professions and are making more than $250,000 a year.

Will this STEP Act pass? Probably not in its current form. If it passes in any form, however, President Biden will certainly sign it into law, given that there are new $3 trillion infrastructure and childcare policies to be funded. Where there was once certainty about estate taxes, uncertainty reigns, and I predict many snake oil salesmen will arise to “help” the Farmer Browns of the world avoid this draconian tax.

The bottom line: The children will be forced to subdivide the farm into house lots and sell off the property to raise the cash necessary to pay the taxes. That is, if they can subdivide the property and develop it, as some global warming proposals might restrict any future development of agricultural land near urban centers.

Matthew Erskine is managing partner of Erskine & Erskine in Worcester, Mass., which provides legal and fiduciary services for unique assets.