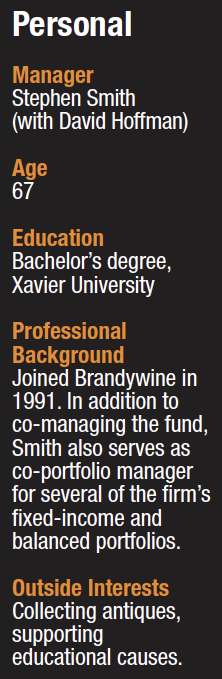

Stephen Smith has some advice for investors who aren’t thrilled with income and capital appreciation prospects for U.S. bonds in the coming year: Give overseas securities a shot. Smith, who has co-managed the Legg Mason Brandywine Global Opportunities Bond Fund with David Hoffman since the fund’s launch in 2006, recommends that fixed-income portfolios have at least 10% to 15% of assets in non-U.S. securities. “Personally, I’d have closer to 50% outside of the U.S.,” he says.

With nearly three-quarters of the world’s sovereign debt issued outside the U.S. and rising economies in developing markets, Smith has a broader investment palette than ever. “The world is my oyster,” he says. “If I don’t like one country’s bonds, I can go somewhere else.”

Currency fluctuations can also provide a tailwind. Even if a country’s bond market produces average performance in local currency terms in a given year, a cheap and appreciating currency can provide a shot in the arm to returns. And if a currency looks like it’s in danger of depreciating, the fund’s hedging strategies can help mitigate the damage to returns.

Avoiding The Index Trap

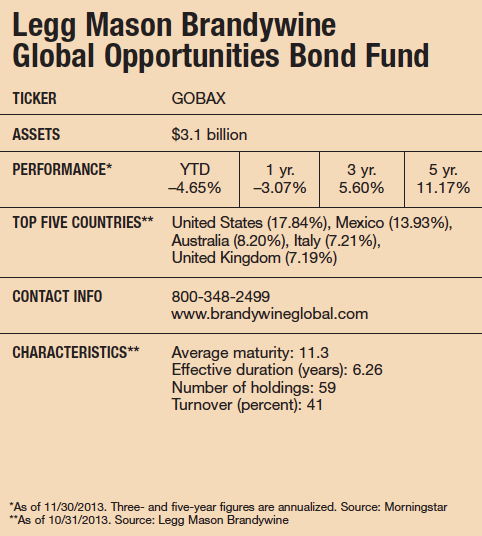

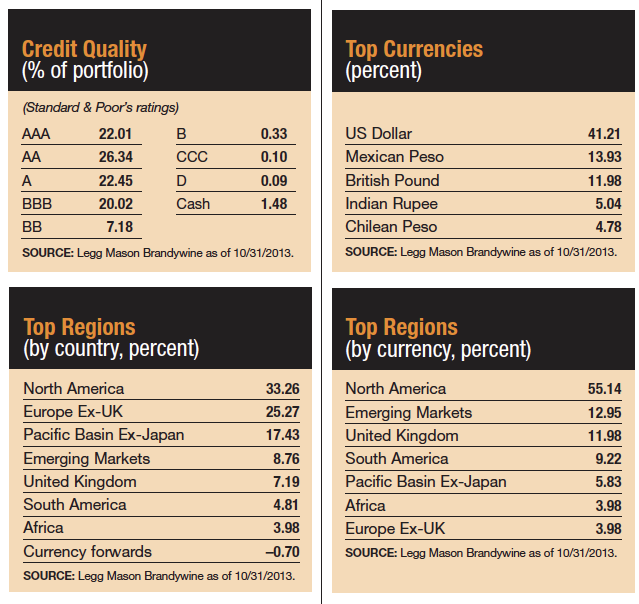

Unlike many global bond fund managers, Smith and his team don’t follow in traditional index footprints. Instead of emphasizing countries with lots of debt, the fund emphasizes those with improving economies, many of them in emerging markets, whose bonds they consider undervalued. Developed market countries with stagnant growth and lower-yielding bonds have a below-index weighting in the fund, or none at all. Although the focus is on sovereign debt, corporate or mortgage-backed securities are fair game when their valuations are attractive. The high conviction portfolio consists of 59 issues, which is unusually concentrated for a bond fund. A low 41% turnover rate indicates Smith and his team are likely to stick with their picks for several years.

Smith also adjusts currency exposure to his view of whether a currency is likely to weaken or strengthen against others. A strengthening currency warrants more emphasis, while an overvalued currency that could fall gets notched down or eliminated.

The approach creates a distinctive portfolio whose returns often veer widely from traditional benchmarks and from its peers. Over the last three- and five-year periods, its annualized returns have been in the top 4% of its Morningstar category. But the fund has also had short-term periods of underperformance such as 2008, when it fell 8.9% against its average peer’s loss of 1.6%.

Often, forging a unique path has meant giving short shrift to some places with a big economic footprint on the global market. Despite the fact that Japan makes up 27% of the Citigroup World Government Bond Index, the fund has no Japanese bonds and no currency exposure to the yen because of Smith’s concerns about low yields and new measures to lift the country’s long-struggling economy. Unlike his predecessors, who opted for cautious and gradual measures to stimulate the economy, Prime Minister Shinzo Abe is moving with surprising swiftness to kick-start the country’s stalled growth engine and bring inflation up to 2%. If that happens, rising rates could negatively impact bond values. Prospects for a stronger yen are also slim. “The government is focused on creating inflation, and a soft yen is instrumental to that outcome,” says Smith. “The case for a sustainable rebound in the yen is not great.”

In Europe, Smith says expensive “socialistic” labor policies and ineffective structural reforms point to a slow growth scenario and a deterioration of the euro against the U.S. dollar and other currencies this year. In that region, Smith favors developing markets such as Hungary, Ireland and Portugal because of their improving credit picture and attractive bond yields. He’s using currency hedging strategies for those positions in anticipation of a decline in the euro.

While the fund is underweight in U.S. bonds relative to the index, Smith sees a relatively benign picture for interest rates over the next few months. He believes last year’s spike in Treasury bond rates was an overreaction by investors to Federal Reserve Chairman Ben Bernanke’s midyear talk of tapering off government bond purchases if the economy continues to improve.

In this fund, a good chunk of foreign exposure comes from up-and-coming emerging markets, where Smith sees better bond prices, higher yields and more vibrant economies than there are in developed markets. “Diversifying into developing markets is especially important now, when markets in the U.S., Japan and Europe appear more synchronized than ever before,” he says.

Smith began investing in foreign bonds back in 1991 when he saw that sovereign debt from foreign countries with improving credit profiles was yielding much more than U.S. Treasurys. Back then, only a handful of developing market countries had investment-grade ratings from Standard & Poor’s. Today, about 60% of them do.

He cites a number of reasons investors might want to share his worldly view of fixed-income investing. Because returns across different U.S. bond sectors tend to be highly correlated, spreading bets across domestic sectors provides a minimal opportunity to diversify or outperform traditional indexes. By contrast, global business cycles and bond market movements can differ dramatically from one another. The greater disparity, he says, offers greater diversification and a better shot at outperforming the indexes through selective country weightings and active management.

Foreign bonds may be difficult to buy and sell, so investors often rely on mutual funds or exchange-traded funds for global bond exposure. But that can backfire if a fund hews very closely to common global bond indexes, as most of them do. Because index weights are directly proportional to the size of a country’s debt issuance, they tend to emphasize countries with huge deficits that issue lots of bonds, such as the U.S. and Japan. Developing nations, many of them with less debt and better economic growth prospects than bigger countries, have a razor-thin presence in global bond indexes.

“The fund’s idiosyncratic makeup has required patience in the past,” Morningstar analyst Miriam Sjoblom noted in a report. “But its outstanding long-term track record offers evidence that when this team forges its own path, shareholders ultimately win out.”

A Broad Palette

January 2014

« Previous Article

| Next Article »

Login in order to post a comment