What’s in a name? In the competitive world of mutual funds, a fund typically has a nameplate that reflects its strategy and instantly tells investors what it’s all about. But not always, as was the case with the T. Rowe Price New America Growth Fund. And over time that became an issue for its portfolio manager, Justin White.

“The New America Growth name didn’t make sense,” says White, who took the reins of the fund in April 2016. “The fund was incepted in the mid-1980s, and apparently there was a period in the ’80s when ‘New America’ meant something, but that stand-alone meaning has disappeared.”

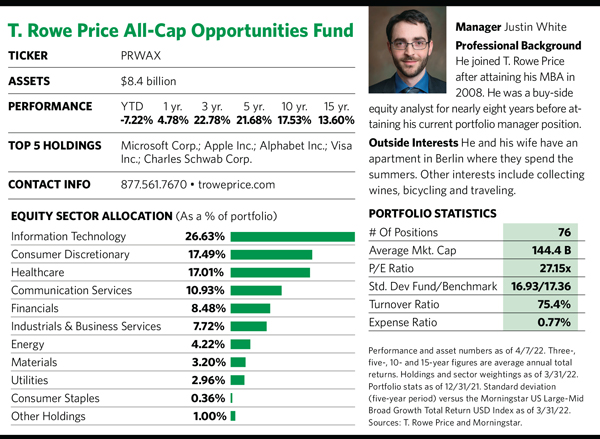

On the same day in March 2021, the fund was rechristened the All-Cap Opportunities Fund and switched its benchmark from the Russell 1000 Growth Index to the Russell 3000. As White explains, this fund has always been an all-cap product, but using the market capitalization-weighted Russell 1000 Growth Index as its bogey (which measures the performance of the large-cap growth component of U.S. equities) gave the fund a heavier tilt toward large- and mega-cap growth companies than he wanted.

“I’m benchmark-aware in that I tend to think about sizing my bets relative to the benchmark weights,” he says, noting that making too big a bet against, say, one of the FANG stocks making up a big piece of the Russell 1000 Growth Index could blow up the risk profile of the fund vis-à-vis its bogey.

The Russell 3000 is also market-cap-weighted, but it measures a broader swath comprising roughly 97% of U.S. equities. That not only reduces the gravitational pull of the largest of the large-cap companies, but it also gives White more flexibility with market-cap size and investment style boxes. In a sense, hitching the fund’s wagon to a new benchmark lets White return to the approach he used when he was an analyst on the T. Rowe Price media telecom team for nearly eight years, before he took over what eventually became the All-Cap Opportunities Fund.

“My coverage area spanned value to growth, small caps to large caps,” he says. “I had success as an analyst investing across different style boxes because I didn’t have a style-box-specific framework.”

Employing this flexible approach as a portfolio manager helps explain why the fund has been a top-quartile performer in Morningstar’s large-growth category during the past five years under White’s leadership (it also sports a top-quartile ranking over the 10- and 15-year periods). As part of that, the fund has produced a higher upside capture ratio and lower downside capture ratio than the category average over the five-year period, according to Morningstar.

In her report on the All-Cap Opportunities Fund last summer, Morningstar analyst Katie Rushkewicz Reichart noted that roughly half of the portfolio’s assets at that time resided outside of the large-growth section of the Morningstar style box, which she said supported the change from the Russell 1000 Growth Index to the Russell 3000. She added that the fund was expected to remain in the large-cap growth category, though fund rating company Lipper classifies it as a multi-cap growth fund. (Morningstar doesn’t have an all-cap style box category.)

Regardless, White says one of the reasons he pushed for the fund name and benchmark changes was that he felt growth investing’s period of outperformance could be running out of gas. He initiated the call for the changes in 2020 just as the pandemic was starting, though he emphasized it wasn’t related to the pandemic.

“I wanted the flexibility to pivot opportunistically the other way if the moment came where it made sense to own more value-oriented stocks,” he says. While it took a year for the changes to become official, White says he began repositioning the portfolio after it became likely that the changes would go through.

He said the Fed’s interest rate and inflation focus meant that for the first time in 12 years the central bank wasn’t going to rescue markets. “The thing that emboldened me to sell a lot of stocks was when I realized that inflation would be with us at a higher level and for a longer period, and that the Fed wasn’t going to bail us out because it had to slay inflation,” he explains.