After years of managing household budgets through the stress of the worst inflation in a generation, U.S. families are increasingly pressured by a different kind of financial squeeze: The cost of carrying debt.

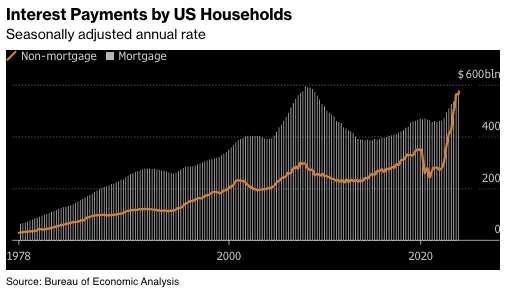

Two years after the Federal Reserve began hiking interest rates to tame prices, delinquency rates on credit cards and auto loans are the highest in more than a decade. For the first time on record, interest payments on those and other non-mortgage debts are as big a financial burden for U.S. households as mortgage interest payments.

The figures suggest a difficult reality for the millions of consumers who are the engine of the U.S. economy: The era of high borrowing costs—however necessary to slow price increases—has a sting of its own that many families may feel for years to come, especially the ones that haven’t locked in cheap home loans. And the Fed, which meets next week for a policy decision, doesn’t appear poised to cut rates until later in 2024.

As monthly debt payments take up more of workers’ paychecks, those consumers are more exposed to potential economic contractions.

And the cost of money affects people’s perception of their own prosperity: A February paper from IMF and Harvard University researchers posits that the recent high cost of borrowing—which isn’t captured in inflation figures—is key to understanding why consumer sentiment remains lackluster even as inflation has moderated and businesses are hiring at a healthy pace.

That theory suggests the debt burden could be a drag on President Joe Biden’s reelection bid, with the economy consistently registering as a top concern at the ballot box.

Nikki Cimino, a 40-year-old recruiter living in Denver, said she finally saved up enough to buy a condo last year, but missed out on the ultra-low interest rates that had made homeownership more affordable in the early days of the pandemic. Her 5.25% interest rate pushed her monthly payments to $1,650. After a divorce in 2020, she’s shouldering $4,000 in credit card debt.

“I’m making the most money I've ever made, and I’m still living paycheck to paycheck,” she said. “There's this wild disconnect between what people are experiencing and what economists are experiencing.”

Relying On Credit

The Fed’s rate hikes, by design, make it more expensive for consumers to borrow.

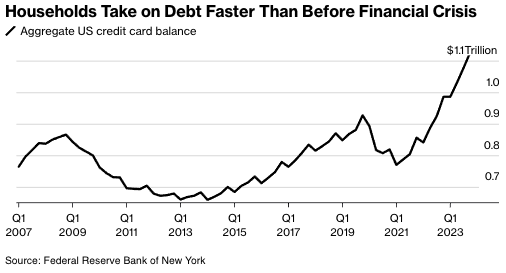

Since the pandemic, families have taken on debt at a comparatively fast rate. According to calculations by Wells Fargo economists, it took only four years for households to set a new record debt level after paying down borrowings in 2021, when interest rates were still near zero. Before that, the time from one debt peak to the next was three times longer. And that increased debt load often comes with a higher price. The typical charge on a credit card has climbed to a record above 22%, according to the Fed.

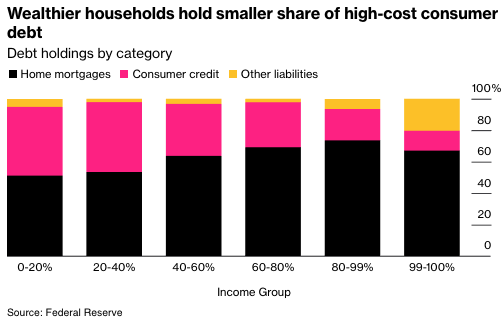

It helps that many families are relatively well-positioned to service that debt: Broad wage gains mean workers are pulling in larger paychecks, and higher home prices have bolstered many households’ net worth. While the share of income going to debt service is higher than it was three years ago—when stimulus checks were making it easier for people to throw money at their credit card bills—it is still low by historical standards.

And part of the reason some Americans were able to take on a substantial load of non-mortgage debt is because they’d locked in home loans at ultra-low rates, leaving room on their balance sheets for other types of borrowing. The effective rate of interest on U.S. mortgage debt was just 3.8% at the end of last year.

Yet the loans and interest payments can be a significant strain that shapes families’ spending choices.

“Many consumers are levered to the hilt—maxed out on debt and barely keeping their heads above water,’’ said Allan Schweitzer, a portfolio manager at credit-focused investment firm Beach Point Capital Management. “They can dog paddle, if you will, but any uptick in unemployment or worsening of the economy could drive a pretty significant spike in defaults.”

For Denise and Paul Nierzwicki, credit cards are the only way to make ends meet. The couple, ages 69 and 72, respectively, have about $20,000 in debt spread across multiple cards, all with interest rates above 20%.

The trouble started during the pandemic, when Denise lost her job and a business deal for a bar that they owned in their hometown of Lexington, Kentucky, went bad.

They applied for Social Security, which helped, and Denise now works 50 hours a week at a restaurant. Still, they’re barely scraping together the minimum payments for their credit card debt.

The couple blames Biden for what they see as a gloomy economy and plans to vote for the Republican candidate in November. Denise routinely voted for Democrats up until about 2010, when she grew dissatisfied with Barack Obama’s economic stances, she said. Now, she supports Donald Trump because he lowered taxes and because of his policies on immigration.

“We had more money when Trump was president,” she said, noting that three years ago her credit card debt was less than half of what it is now.

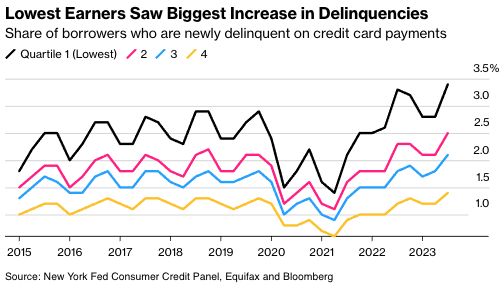

The Nierzwickis are not alone in struggling to stay on top of debt. Among middle-class adults with credit card payments, more than a quarter say they’ve been “behind” at some point in the last year, according to exclusive data from the Harris Poll for Bloomberg News. New York Federal Reserve data shows credit-card balances turning delinquent—more than 30 days late—at an annual rate of 8.5% last quarter.

The high borrowing costs—and how households manage them—pose some risk to the broader economy.

“As rates rose in 2023, we avoided a slowdown due to spending that was very much tied to easy access to credit,” said Shannon Grein, an economist at Wells Fargo. “Now, credit has become harder to come by and more expensive,’’ she said, calling the change “a significant headwind to consumption.”

Mohsin Meghji, managing partner of M3 Partners, a firm that consults for troubled companies, is girding for the reverberations of that kind of pullback by consumers.

“Any tightening there immediately hits the top line of companies,” said Meghji. For those companies—heavily indebted themselves after years of easy borrowing—“there’s no easy fix,” he added.

Of course, consumers can try to refinance their debt after the Fed lowers rates. But the timeline and magnitude of cuts is uncertain, and refinancing fees can sometimes outweigh the benefit.

Student Debt Burden

The return of student loan payments is adding to many borrowers’ financial stress.

Brittany Walling, a 29-year-old in Columbus, Ohio, has about $80,000 in federal student loans and $20,000 in private debt from her undergraduate and graduate degrees. That’s alongside $6,000 in credit card debt, which she accumulated when she was unemployed for a six-month stretch in 2022.

She’s been living paycheck to paycheck, she said, on her $50,000-a-year salary working for the public health department.

“I can't even save, I don't have a savings account,” she said. “I just know that a lot of people are struggling, and things need to change.”

For Walling, that sentiment isn’t necessarily going to be a decisive factor at the ballot box. While she said she was disappointed that Biden’s student debt forgiveness plan was struck down by the Supreme Court, her views on abortion and transgender rights will likely keep her from voting Republican.

Yet the issue overall looks like a headwind for Biden, as it shapes the economic outlook of people like the Nierzwickis.

“Maybe the Fed is done hiking, but as long as rates stay on hold, you still have a passive tightening effect flowing down to the consumer and being exerted on the economy,” said Grein, the Wells Fargo economist. “Those household dynamics are going to be a factor in the election this year.”

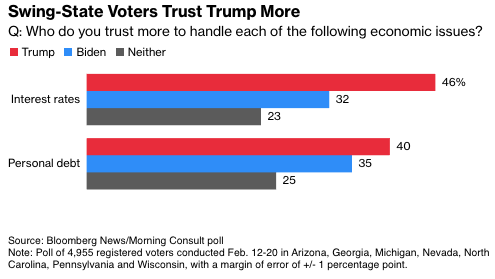

Plus, swing-state voters in a February Bloomberg News/Morning Consult poll said they trust Trump more than Biden on interest rates and personal debt.

Cimino, the Denver condo buyer, says despite her debt load, she feels lucky that she makes $65,000 a year and owns a home—a situation that leaves her better off than many others.

“Being middle-class these days,” Cimino said, “is just carrying around a lot of guilt.

— With assistance from Alexandre Tanzi

This article was provided by Bloomberg News.