If we had to emphasize one mantra of investing, it would be the importance of maintaining a long-term perspective. We must keep our emotions in check and strive to block out the hype—the noise that can distract us from these long-term goals. The “hype” on everyone’s minds right now is of course, the 2016 presidential election, and that cannot be ignored. If this were a debate and LPL Research was behind the podium, the question we’d be asked by many is: How will this election affect the markets? Our first response: it’s not about election years, or even political parties—but about investing for the long run. Nonetheless, there are some historical election year patterns that may be worth watching.

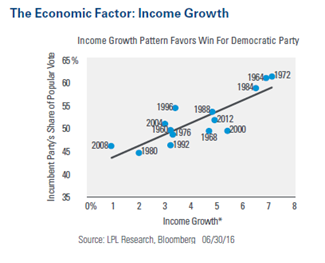

The Economic Factor: Income Growth

Income growth is one way to gauge the impact of the economy on election results, as this measure captures the impact of several key factors, including the unemployment rate, inflation, and wage growth. In the year leading up to the election, inflation-adjusted, after-tax income growth of about 3–4% appears to be the threshold for the incumbent party to win. As of June 30, this measure is currently growing in the 3–3.5% range, suggesting that the incumbent Democratic Party will win just over 50% of the two party vote in November’s election.

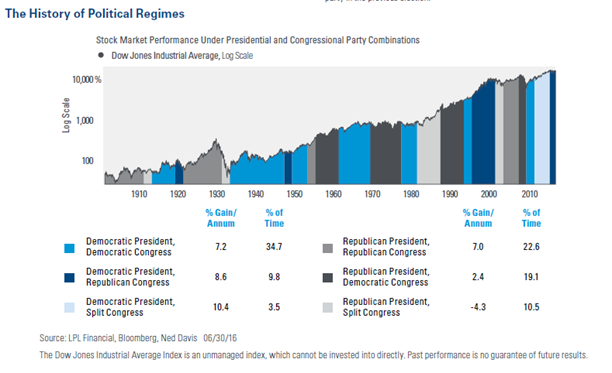

The History of Political Regimes

The market mantra “gridlock is good” suggests that a split Congress, or a President from the party opposite the one in control of both houses of Congress, would be better for markets. The downside, however, is that gridlock could limit policy action at a time when it is needed on several fronts (taxes, entitlement reform, immigration, security, etc.). Historically, the combination of a Democratic President and split Congress has been best for markets, thought it has occurred infrequently, with an average gain of 10.4% for the Dow Jones Industrial Average. A Republican sweep of the White House and Congress has been positive for stocks as well, with an average gain for the Dow of 7%.

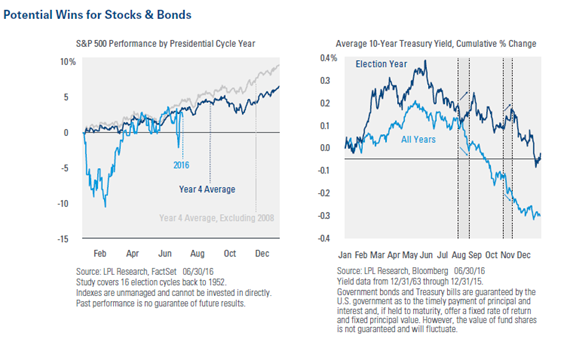

Potential Wins for Stocks & Bonds

Election years have been strong for stocks, especially excluding the anomaly in 2008 (the worst year of the Great Recession), with gains averaging near 10% and positive returns in a solid 87% of years. The election year pattern for stocks suggests volatility may persist through the summer months until markets have more clarity on the candidates and their platforms. Once that clarity arrives, often before the election itself, stocks have typically staged a late-year rally.

The path of bond yields during a presidential election year is very similar to the historical pattern for any given year. The seasonal tendency is for yields to decline starting in late October through November; but during election years, the tendency is for an increase in Treasury yields. The path of Treasury yields is slightly higher during election years (compared to the average year) due to the frequency of Fed rate hikes.

Taking these historical patterns into consideration, and given the current environment, suggests that we will remain in a similar policy and stock environment as we’ve seen in recent years.