Model portfolios may offer substantial benefits to financial professionals, but many are reluctant to implement models in their practice. Some of the reasons financial professionals typically give, while understandable, don’t hold up under examination.

A Brief Story: Automation And Responsibility

Let’s begin with a short story that may provide a helpful analogy. Only nine years after the Wright brothers made their initial flight at Kitty Hawk, North Carolina, a man named Lawrence Sperry created an instrument called a gyroscopic automatic pilot that could balance the plane without human assistance. A common myth still held today is that the power of autopilot means that all that human pilots need to manage is an airplane’s takeoff and landing. The reality is quite different: Pilots have many tasks during a flight, including making sure that the plane is operating smoothly, anticipating possible malfunctions, and constantly preparing for alternate landing destinations if the plane is in distress.

The moral of this story is that technology that simplifies one task doesn’t eliminate the need for human agency; rather, it frees up the human operator to handle more sensitive tasks requiring judgment and discretion. Similarly, financial professionals who delegate portfolio construction to third-party models after proper research and due diligence aren’t abandoning their main responsibility. They’re freeing time to spend guiding their clients through challenging decisions and market volatility while simultaneously giving themselves more opportunities to grow their business and income.

Not Your Father’s Fund Categories: Types Of Model Portfolios

Before delving into several myths about the use of model portfolios, a review, not necessarily exhaustive, of model portfolio types is in order. Model portfolios don’t typically fit the descriptions we normally associate with mutual funds, such as large cap, value, or international, to name a few.

• Target risk—An especially popular model for investors who seek a certain level of risk, on a continuum from seeking aggressive growth to focusing primarily on generating income

• Target date—Useful in planning for retirement, college, or other future events. Depending on their timeframes, they typically begin with heavier equity allocations and then follow what’s known as a glide path toward fixed income over time

• Income oriented—Focused on generating attractive cash flow from a variety of sources

• Risk aware—Designed to reduce potential risk when markets are falling and add potential risk as they rise

• Tax sensitive—Particularly useful for high-net-worth investors oriented toward pursuing higher after-tax returns with tax-efficient vehicles such as municipal bonds and exchange-traded funds

• Dynamic asset allocation—Active trading, trying to capture market trends and benefit from volatility

• Alternative asset allocation—Using nontraditional asset classes to generate absolute returns with low correlations to the stock and bond markets

Financial professionals interested in using models should be sure to have access to these classes of portfolios to accommodate client desires and needs.

Now let’s address some myths.

Myth 1: My Clients Work With Me Because They Want Me To Act As CIO

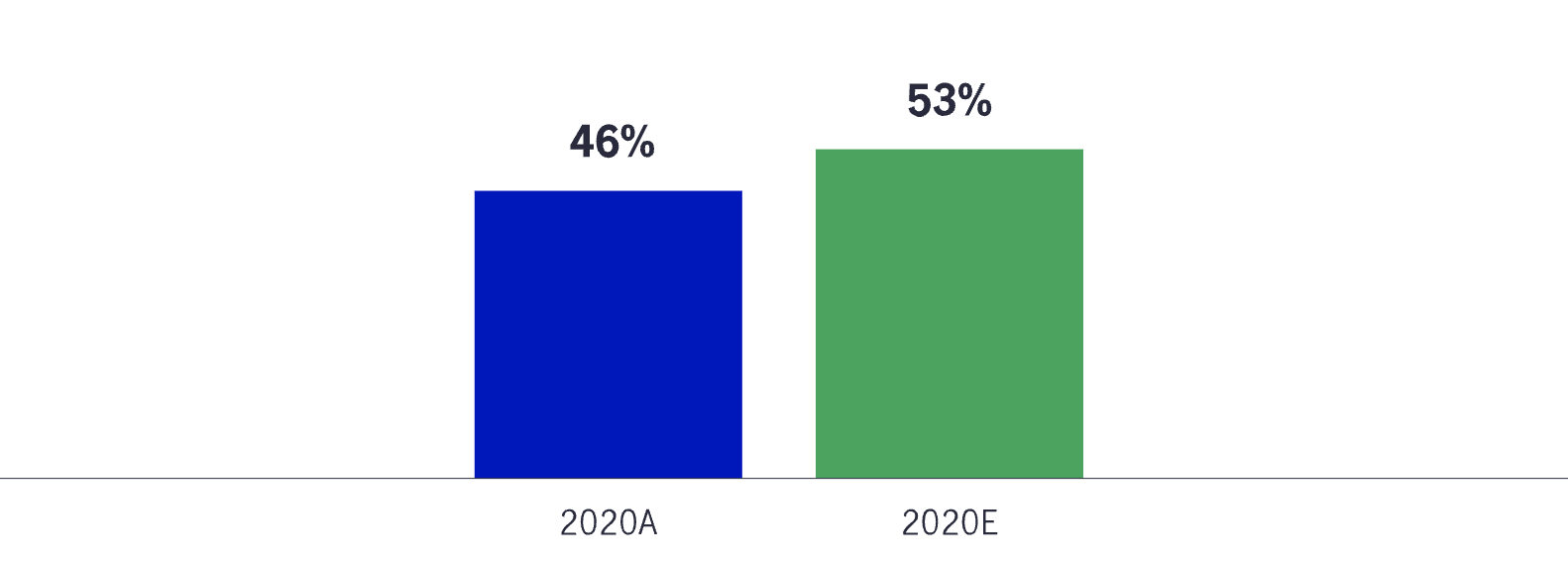

The reality is that relative performance may be, while not irrelevant, one of the least important considerations clients have in evaluating their financial professionals. Relationship management, which involves understanding goals, needs, and risk tolerance, is more important than portfolio management.¹ Performance relative to the market is less important than seeing problems and opportunities and knowing your whole financial picture. In fact, the role of the financial professional is shifting from pure investment management toward comprehensive financial planning, from 46% in 2020 to an anticipated 53% in 2022.1

Clients Receiving Comprehensive Financial Planning

Source: "U.S. Advisor Metrics 2020," Cerulli Associates, 2020.

Myth 2: Using Models Won’t Add Tangible Benefits To My Practice

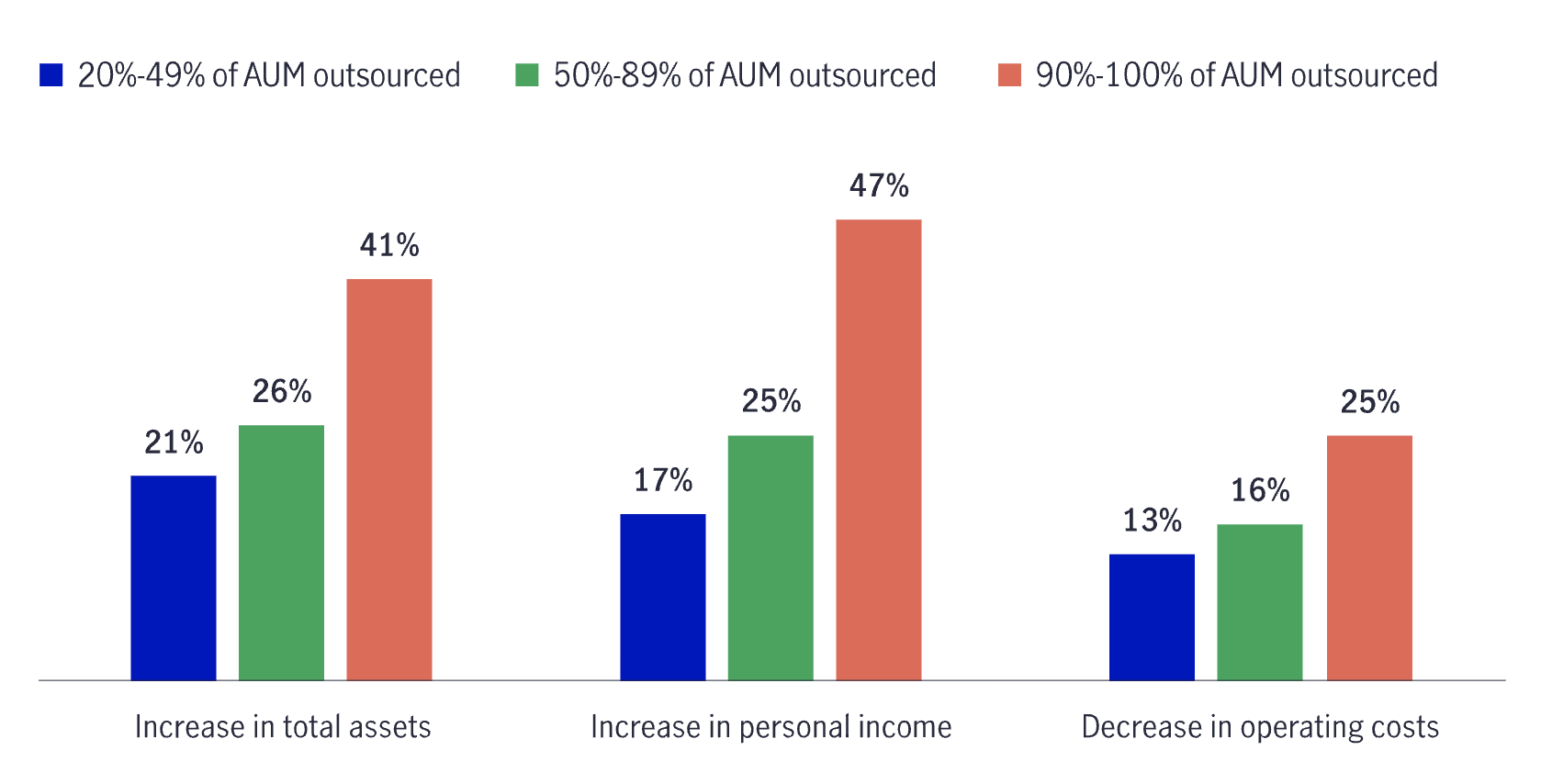

The Benefits Of Outsourcing Management

Source: "The Power of Outsourcing Investment Management," AssetMark, July 2020.

This may be the easiest myth to debunk. Using model portfolios clearly brings substantial time savings by freeing the financial professional from the portfolio construction process. But this is only part of the story. Models may offer more consistent results than internally built portfolios thanks to the expertise of the model provider. Moreover, using an established third-party provider may help reduce the advisor’s exposure to fiduciary concerns by bringing on an additional and essential level of oversight.

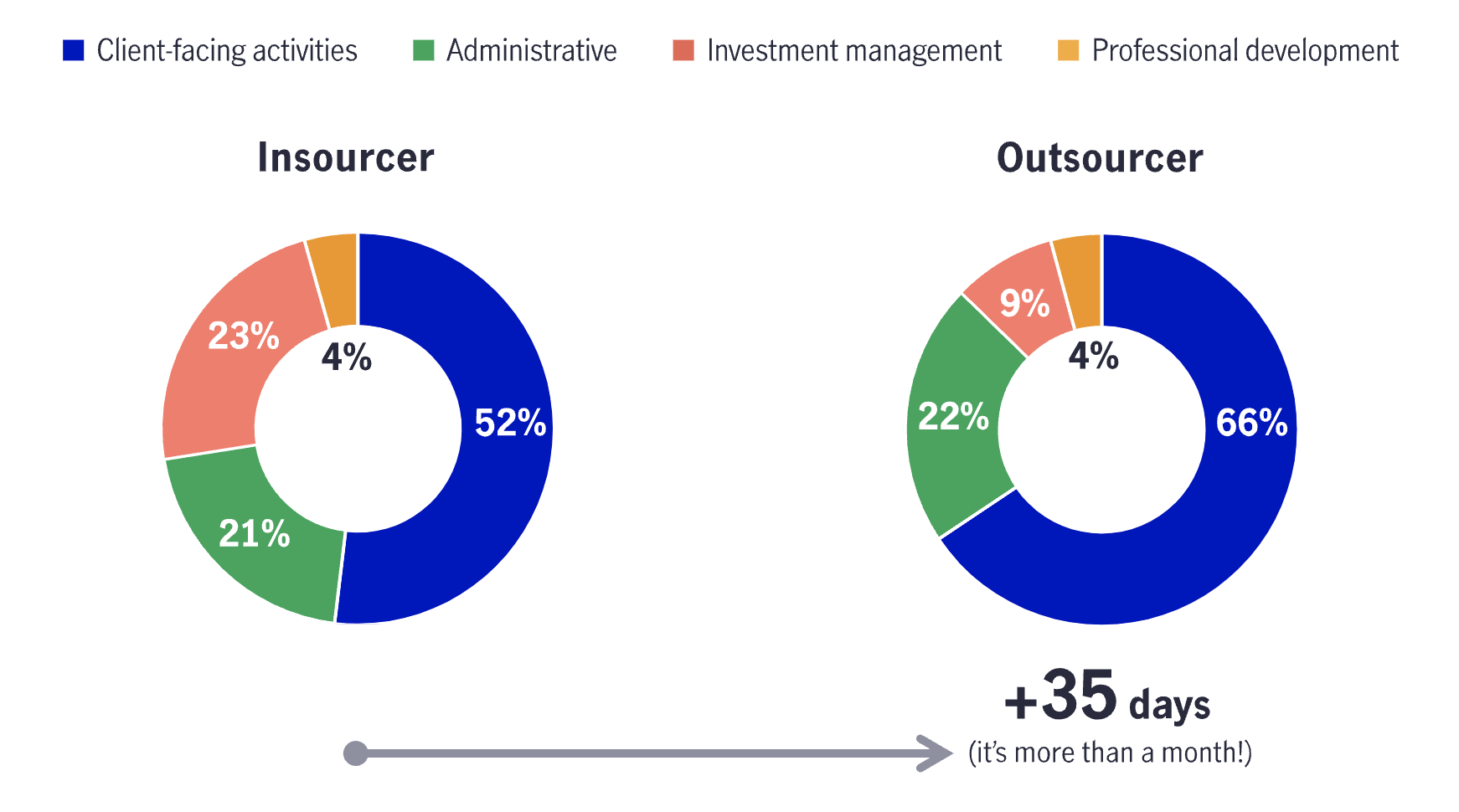

Getting back to time savings, a 2020 study found that outsourcing through third-party or home office models frees more than a month per year relative to using internal intellectual capital (insourcing). The financial professional can use this substantial additional time for more in-depth financial planning services and new client prospecting, a process that results in actual cost savings.2

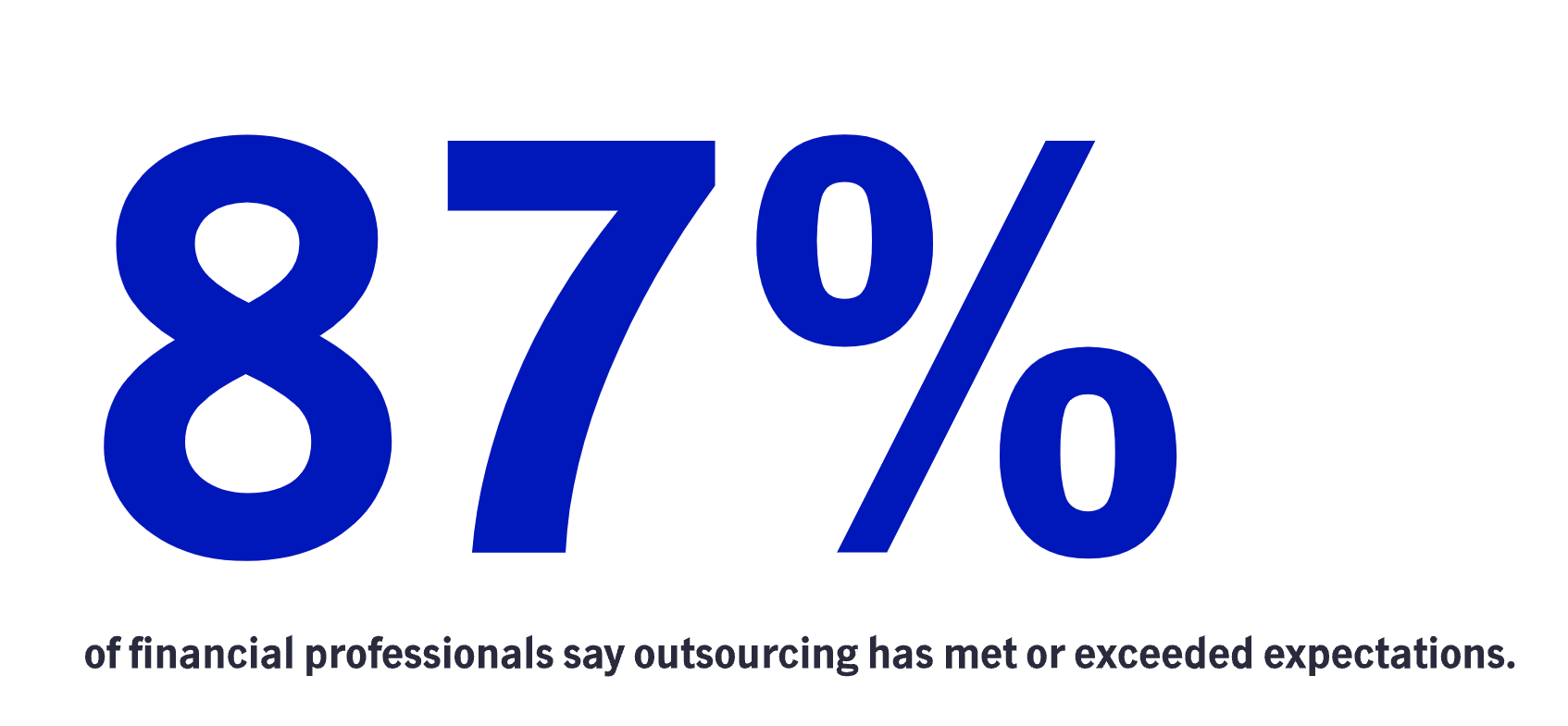

More generally, another study found that 87% of financial professionals found that outsourcing investments met or exceeded their expectations.3 The study showed that the more financial professionals outsourced, the greater their total assets and personal income and the lower their operating costs.

A Pleasant Surprise

Source: "The Power of Outsourcing Investment Management," AssetMark, July 2020.

Myth 3: Switching To Outsourcing Will Be A Time-Consuming Process

The process may indeed seem time-consuming up front when the financial professional performs due diligence on third-party candidates. But while periodic review is in order, the financial professional may view the up-front time cost as being largely amortized over a period that may extend for many years.

Some of the key due diligence questions a financial professional should address include:

• Does the provider have expertise in a sufficient range of assets, as asset allocation has been frequently shown to be more important than security selection?

• Does the provider have open architecture (i.e., are multiple managers involved in constructing the portfolio or are all the assets proprietary)?

• What's the fee structure? Are there additional layers?

• How deep is the sales and service team? Better support typically means a better client experience.

Myth 4: Transitioning To Models Is An All-Or-Nothing Proposition

While full outsourcing results in the greatest time savings, it’s not the only option. Cerulli Associates explains that “insourcers may be open to discussions with wholesalers, portfolio construction consultants, portfolio managers, and other professionals close to the investment process. These will be the most customized conversations for asset managers and third-party strategists and will require the most sophisticated technology-assisted portfolio analysis.”2 In other words, the degree to which financial professionals use third-party providers remains an individual choice.

Insourcing takes the most time. It typically involves engaging consulting teams and in-house intellectual capital to build portfolios seeking beneficial outcomes. Asset allocation and manager selection are handled internally. Modifying is the middle ground—starting with home office or third-party models, then tweaking them internally, generally monthly or quarterly. The modifier may choose to substitute other managers for those recommended by the external models. Outsourcing, again, leaves the maximum amount of time available for tasks outside the portfolio construction process.

Developing An Action Plan

How much time could financial professionals get back if they outsource investment management?

Source: "U.S. Advisor Metrics 2020," Cerulli Associates, 2020.

Financial professionals should decide where on the spectrum of insourcing to full outsourcing they want to reside. Next, they should develop a plan to group their clients into buckets and transition them to different models based on the clients’ assets, goals, and sophistication.

Finally, and perhaps most important, financial professionals need to form a communication strategy explaining to clients how the new approach will benefit them. Such a plan may include various types of education, including, but not limited to, family meetings covering issues such as longevity planning and wealth transfer.

1 "U.S. Advisor Metrics 2019," Cerulli Associates., 2020. 2 "U.S. Asset Allocation Model Portfolios 2020," Cerulli Associates, 2020. 3 “The Power of Outsourcing Investment Management,” AssetMark, July 2020.

John Hancock Investment Management’s Practice Management Network

John Hancock Investment Management Distributors LLC. Member FINRA, SIPC. 200 Berkeley Street, Boston, MA 02116, jhinvestments.com MF2403366, 9/22