We can see the impact of low rates on financial earnings. Second quarter 2016 earnings for the developed world financial sector (defined by the MSCI EAFE Index) declined -11.6%. Equally, if not more important, expectations for earnings for the rest of 2016 and for 2017 have been reduced. At the end of March 2016 (before any first quarter earnings were released), financial sector earnings for the year were expected to be flat. Currently, consensus expectations are for financial sector earnings to decline -9.8% for the year. The outlook for developed market financials has become even gloomier. In contrast, earnings for financial companies in EM actually grew by 2.7% during the second quarter. While not much, it is certainly much better than in developed markets. Furthermore, expectations for financial company earnings for the rest of the year really have not changed from March 31 to today. The market is expecting financial earnings growth of just over 14% for 2016.

VALUATIONS EMERGE AS ATTRACTIVE

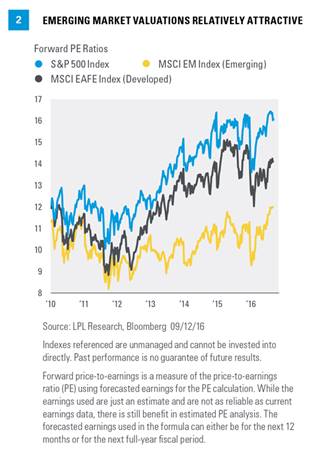

Earnings growth is important, but so is what investors are willing to pay for earnings. Low interest rates globally have encouraged investors to buy stocks seeking greater total returns, and increasingly seek income from dividend-paying stocks rather than from bonds. As noted above, EM interest rates have not had the same magnitude of decline; in some markets, rates remain quite high. This is one reason that EM valuations have not expanded as rapidly as the same measures for the U.S. and EAFE [Figure 2]. Globally, we see price-to-earnings ratios (PE) generally follow each other across the regions. This makes sense, despite regional differences; all stock markets operate in a world that became increasingly globalized. However, valuations for both the U.S. and EAFE expanded rapidly, partially because of the cumulative impact of the Fed’s third quantitative easing program that began in September 2012 and further interest rate reductions by the European Central Bank (ECB) in May 2013. Equity markets in the U.S. rallied, but with PE expansion as a significant part of that rally. The reverse happened in EM. Stock prices fell and valuations for the asset class contracted. We believe this divergence may represent an opportunity, but only if earnings continue to increase.

COMBINING FACTORS

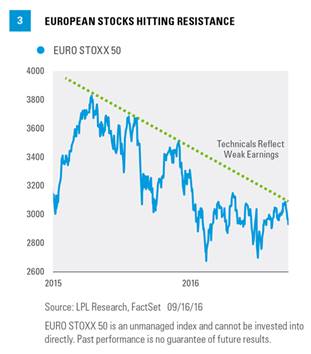

LPL Research uses a combination of fundamentals, like earnings growth, valuations, and technical factors in evaluating investment opportunities. While this commentary focused mostly on EM, several previous commentaries have focused on Europe, which is the primary component of the EAFE Index. We can use the activity in the European markets to show how these factors combine. Valuations have increased in Europe, though not to the same extent as for U.S. equities. Earnings in developed overseas markets have declined and expectations continue to fall. The technicals are telling us that the market has real questions about European fundamentals. Overall, Europe continues to lag, as nearly all European country stock markets are down in 2016, with the Financial Times Stock Exchange (FTSE, the primary U.K. stock market gauge) the surprising outperformer. Technically, the EURO STOXX 50 has been in a downtrend for more than 15 years. Focusing on more recent market activity [Figure 3], the EURO STOXX 50 ran into firm resistance from a trend line going back to the April 2015 peak. We can see in this example how the three components of our process can reinforce each other, and in this case reinforce our caution with respect to Europe and developed international equities in general.

CONCLUSION

Emerging markets have seen earnings increase and future expectations remain stable. This improvement has occurred across many sectors, including the important financial sector. Combined with relatively attractive valuations, we believe opportunities exist in EM for suitable investors, though strength in these markets will likely depend on continued earnings growth. We can see how disappointing earnings can impact performance, and therefore the stock charts and technicals, by looking at recent technical weakness in European stocks.

Burt White is chief investment officer for LPL Financial.