According to the efficient market hypothesis, investors who learn about a company’s positive earnings surprises are supposed to bid up its stock price. After all, the surprise should reflect new expectations about a company’s improved prospects. But more often than not, that bid up doesn’t happen.

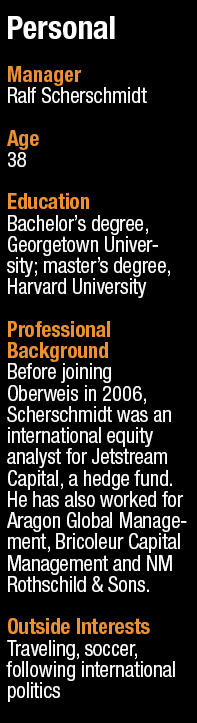

“Study after study indicates that quick price adjustments in response to earnings surprises often do not occur,” says Ralf Scherschmidt, who manages the Oberweis International Opportunities Fund. “In fact, it can take many months, and sometimes over a year, for prices to slowly reflect the new reality.”

According to the 38-year-old manager, the secret sauce for successful investing is buying a stock after a positive earnings surprise has been announced but before investors have woken up to its longer-term implications. He believes the lag time, called “post-earnings announcement drift,” occurs because of human behavioral biases.

“In the real world, market participants take a lot of time to adjust to a new reality and process information,” he says. “And when people have an ingrained belief about a company, they find it difficult to change that belief even in the face of convincing evidence to the contrary.”

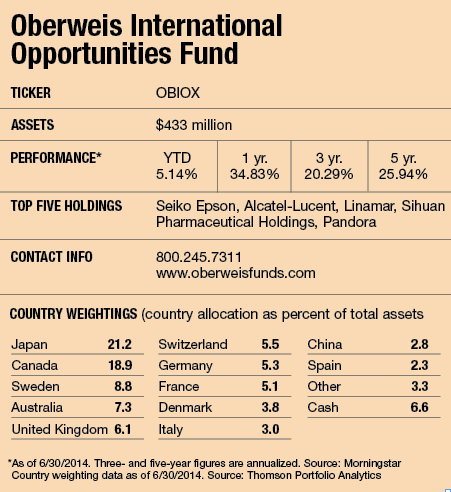

While lots of portfolio managers seek to exploit the market’s under-recognition of certain stocks, Scherschmidt has been far more successful at it than most. Over the year ended May 31, his fund’s performance has been in the top 5% of its Morningstar peers, and over the last three- and five-year periods, it’s been in the top 1%. It was awarded “Best Fund” by Lipper among international small- and mid-cap growth funds for its three- and five-year performance, and it has Morningstar’s five-star rating.

The trade-off for that performance has been above-average volatility. Tagged “aggressive growth at a reasonable price” by the firm, the strategy combines growth and momentum. The International Opportunities fund has generated a three-year standard deviation of 19.56, whereas the MSCI EAFE index’s was 16.38 and the Morningstar peers figure was 16.01.

Scherschmidt says the presence of small, fast-growing companies explains why the fund is bumpier than the indexes, which are usually loaded with large caps. And the fund’s decisive, focused approach generates more volatility than the strategies of peers, which usually invest in hundreds of stocks and use indexing or index-like strategies.

“The more stocks you own, the closer you’re going to come to benchmark returns,” he says. “But you are also going to look like a closet indexer. We run a fairly concentrated portfolio of 70 to 80 stocks. We may have more short-term performance deviations from the benchmark, but we’ve also had much better returns over time.”

Although the fund isn’t a benchmark hugger, it has some strict investment parameters so that it won’t overreach in individual sectors and countries. Country allocations may not exceed 15% of equity assets, or three times the MSCI World ex USA Small Cap Growth weighting, whichever is greater. Sector allocations may not exceed two times the index’s weighting or 50% of assets. The fund reduces individual security risk by making sure no positions can account for over 7% of the portfolio.

Scherschmidt is currently finding the most opportunities in the information technology sector, which accounts for 28% of his equity assets while it only accounts for 12% in the MSCI World ex USA Small Cap Growth Index. On the other hand, energy, materials, industrials, consumer discretionary financials and consumer staples are all heavier in the index. Overweight countries in the Oberweis fund include China and France, while its weightings for the U.K. and Japan fall short of the benchmark.

An Overlooked Asset Class

With analysts and investors covering the same ground, it’s getting harder and harder to find overlooked opportunities. But because international small caps are much less discovered than other parts of the investment universe, it’s still possible to find stocks whose prices aren’t living up to their earnings potential yet.

“International small caps make up about 6% to 7% of the global equity pie, yet most investors have 0% to 2% in them,” Scherschmidt says. “From a strategic standpoint, they make sense because of their low correlation to other asset classes and superior performance over time.” He says a good “neutral” starting point would be to have 12% to 14% of an international equity allocation devoted to small-cap stocks.

Oberweis International’s approach is an outgrowth of the company’s aggressive domestic small-cap growth strategy honed by Jim Oberweis. The company’s namesake once ran his family’s successful dairy products business, published a well-known investment newsletter and became a successful stock broker before founding Oberweis Asset Management in 1989.

Over the years, the firm, along with its small mutual fund family, carved a niche as an emerging growth stock specialist. Son James W. Oberweis began running the business in the early 2000s, when his father stepped aside to pursue other interests, including a number of unsuccessful runs for public office in Illinois. (He finally clinched the Republican nomination for U.S. Senate in 2014.)

After a few years, the firm decided to extend its small-cap strategy to global markets and began looking for someone to run the strategy. That person turned out to be Scherschmidt, who had answered the firm’s ad in a financial analyst journal for an international small-cap equity manager. After several months of discussions and interviews with Oberweis, Scherschmidt signed on in 2006 and began managing the fund the following year.

The decision to go global breathed new life into Oberweis’s fund business, which was wilting after small, high-growth U.S. companies fell out of favor following the 2008 financial crisis. Around the same time, investors began eyeing international small caps as an asset class that promised better performance than the already-discovered emerging markets.

Today, the international strategies Scherschmidt runs account for approximately $1 billion of the firm’s $1.7 billion in AUM. At $433 million in assets, International Opportunities is by far the largest fund in the Oberweis family, with its much-less-popular domestic offerings ranging from $9 million to $61 million in assets.

Fast Lane

August 2014

« Previous Article

| Next Article »

Login in order to post a comment