Stocks and corporate bonds may be the surprise big losers once the Federal Reserve starts reducing its $4.5 trillion balance sheet.

A committee of investors and banks highlighted that outside risk in a presentation to Treasury Department officials this month. A week after that, strategists at Morgan Stanley separately warned that investors are underestimating the trouble that the Fed’s plans could bring to corporate debt markets.

Money managers don’t seem alarmed so far. Stocks have gained 10 percent this year, including dividends, while corporate bonds are up 4.8 percent as of Friday’s close. Both Treasury debt and mortgage bonds, the securities most directly influenced by the Fed’s plans to reinvest less money, have lagged the broader U.S. bond market in 2017, although their returns tend to be more stable.

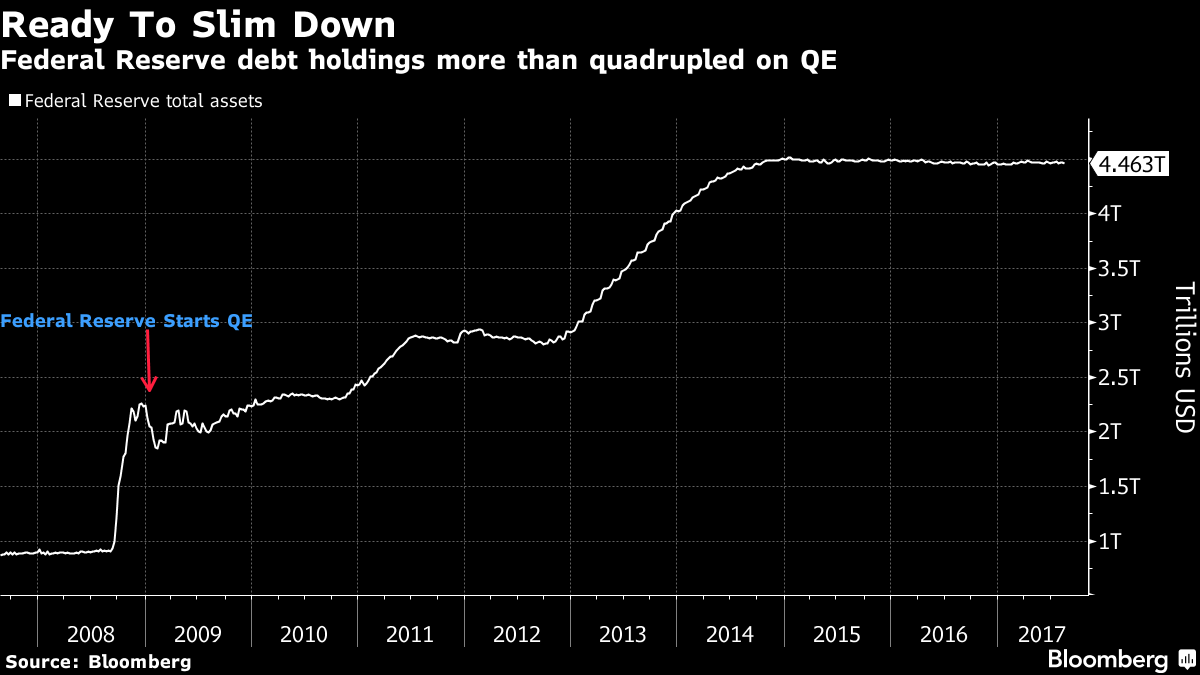

The threat to the stock and corporate bond markets underscores the bind that the Fed is in as it tries to scale down the extraordinary stimulus it gave the economy during and after the financial crisis. Its quantitative easing program has more than quadrupled its debt holdings, and Fed policy makers plan to start slimming down those investments soon now that the economy is on more solid ground. But cutting back could hurt markets and perhaps the broader economy in ways that are hard to forecast.

As the Fed contracts its balance sheet, “all we can do is hypothesize what the paths are because this is unprecedented,” said Joubeen Hurren, credit fund manager at Aviva Investors, which managed $456 billion as of June 30.

Companies’ borrowing costs, for example, might rise by 1.35 percentage points relative to Treasuries, according to the committee’s presentation to the Treasury, and those higher funding expenses could weigh on stocks. The European Central Bank is considering further dialing down its quantitative easing, which could add to the pressure.

After years of the central bank stimulus, signs of froth are everywhere. On the debt side, U.S. high-grade companies have already sold about $1 trillion of bonds this year, and are on track to break last year’s issuance record. Junk bond yields, at just 5.8 percent, are near all-time lows. In stocks, U.S. markets are close to record highs.

The Fed hasn’t been buying corporate debt, but as it snapped up Treasuries and mortgage securities, bond yields broadly fell, making it cheaper for companies to borrow. Corporations have often used the money they raised to buy back shares, buoying the stock market. That’s what worries a group of investors and banks known as the Treasury Borrowing Advisory Committee, which counsels the government on its funding and the economy.

“The private sector piggy-backed on the Fed’s large-scale asset purchases, a move that promoted a surge in corporate borrowing and tighter risk spreads,” wrote Jason Cummins, TBAC chairman, in an Aug. 2 letter to Treasury Secretary Steven Mnuchin. Cummins is head of research at hedge fund Brevan Howard.

‘Meaningful’ Decline