• It gets worse: Some 38 percent of those misbehaving advisors later go on to hurt even more clients.

• You might think bigger firms would be more diligent, but you’d be wrong. At some large firms, more than 15 percent of advisors have records of serious misconduct. The highest was Oppenheimer & Co., where 20 percent had such black marks. Oppenheimer responded to the study, first published a year ago, by saying it replaced managers and made changes to hiring, technology, and compliance procedures.

• Predators typically seek out the weak, and financial advisors are no different: The study shows that those with misconduct records are concentrated in counties with fewer college graduates and more retirees.

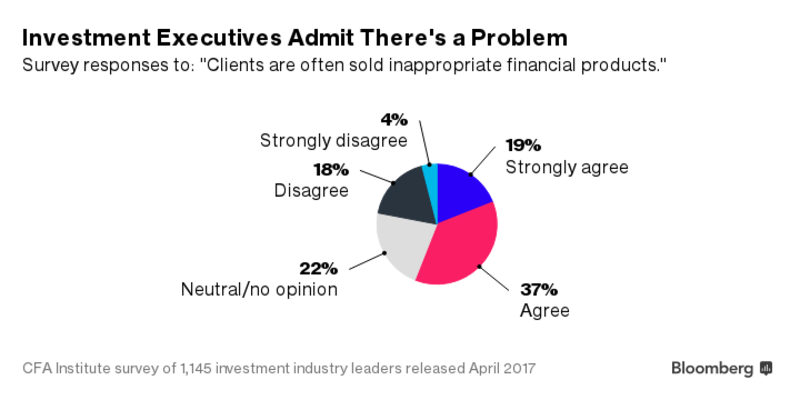

The unique nature of the investing business makes it easier to exploit client ignorance. Investing is complicated, with sometimes-intentionally impenetrable jargon, and customers must trust their advisors in the same way they trust their doctors: If an expert makes a recommendation, you tend to follow it, whether that means getting heart surgery or a variable annuity.

“Some firms ‘specialize’ in misconduct and attract unsophisticated customers,” the researchers write.

More astute investors aren’t entirely at the mercy of advisors. Certain products are so expensive and so typically underperform that their mere presence in your portfolio can suggest you’re getting bad advice. Variable annuities, high-fee mutual funds, and non-traded real estate investment trusts, or REITs, are good examples. Non-traded REITs charge, on average, upfront fees of 13.2 percent, while delivering returns about half those of traded REITs, which are also much easier to buy and sell.

Another example is the “reverse-convertible,” a complicated product in which a bond payment is linked to the performance of a stock. Banks will create two or more versions of the same reverse-convertible. The only difference is one offers a higher payout—yet investors usually end up choosing the inferior product. University of Minnesota’s Mark Egan calculated that customers bought over 10 times more of a reverse-convertible with a 9 percent yield than an otherwise identical convertible with an 11.25 percent yield.

Why? Because that’s what their advisors told them to do. The more lucrative version paid advisors a commission of 2.15 percent, while the inferior one paid 3.09 percent. In other words, advisors could boost their pay by half if they steered clients to an obviously worse investment.

Commissions like these are the traditional way advisors hide costs from investors: Instead of clients paying them directly, companies pay advisors commissions to push their clients toward particular products.

“There’s an ever-present incentive to betray your client’s interest,” said Benjamin Edwards, a law professor at the University of Nevada, Las Vegas. These conflicts don’t just cost investors more money. They also skew the U.S. economy by pouring capital into less productive investments merely because they offer a better “kickback” to advisors, he said.