Gold is not an ordinary word. Mention it to anyone in the world and you are assured a reaction that's steeped in emotion, either negative or positive. The word can evoke greed or fear and loathing. And that's not a new phenomenon, but one probably as old as money itself.

Today, gold has become the hottest topic around water coolers, and not just among financial types. But its runaway price increase indicates that it has lost none of its power to evoke powerful feelings, and today that emotion is less likely to be greed than it is fear.

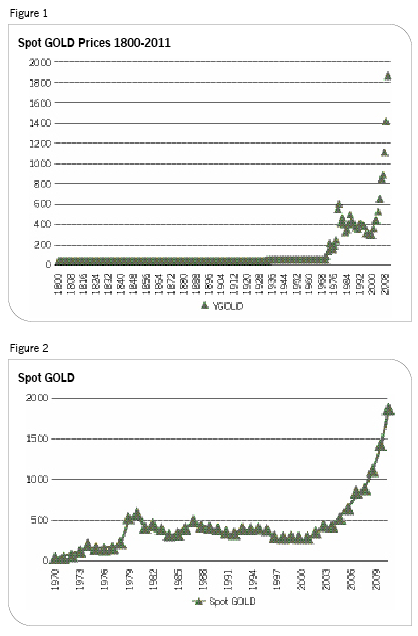

How else do we explain its meteoric rise? To properly appreciate the phenomenon, it is worthwhile to begin by looking at the long-term history. (See Figure 1.)

Interestingly, the periods of astronomical increase in gold prices says more about the global economy than about gold itself. Since its recently recorded history, gold has languished for the longest time (between 1800 and 1933) at around $20 per troy ounce. The price rose slightly at the end of the Great Depression to $35 per ounce-and stayed there until 1967. Of course, this was during the Bretton Woods system, which fixed world currency prices to the gold standard.

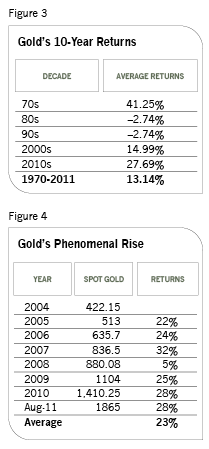

It was only after 1967, as that agreement started disintegrating and an era of market-based economic pricing emerged, that gold started its first phase of growth. This coincided with the era of modern finance and open global markets. The following chart shows gold prices from 1970. The accompanying tables show ten-year returns for each of the decades since 1970.

Figures 2 and 3 tell interesting stories. In retrospect, the '80s and '90s were a time of more stable global economic growth within an environment of contained inflation. The other three decades were more tumultuous; the Roaring '70s was a time of heightened uncertainty with high inflation rates amid waves of unfamiliar market deregulation. The latter half of the 2000s was similar as first the dot-com bubble crashed, then the real estate bubble, and the economy suffered a downturn in 2008 and 2009, the severest since the Great Depression.

Gold, meanwhile, has suffered its most tumultuous period ever in the last six years. Since 2005, it has earned an average annual return of over 23%! This incredible spurt saw prices double twice. Figure 4 shows the phenomenal rise.

What is the cause for such a trend? For one, the spikes in gold prices have always coincided with increased global economic uncertainty and turmoil. Traditionally, gold has shared the position of safe haven along with the U.S. dollar, the global reserve currency. Thus, in the past, whenever global economic uncertainty increased, both gold and the U.S. dollar increased in value. But gold prices in the past did not increase as much partly because of the alternative investment in U.S. dollars.

Over the past ten years, however, the U.S. dollar has steadily lost value against all major currencies with the weakening of the U.S. economy. The loss of confidence in the buck is one reason for gold's unusual popularity today. For people all over the world, the current global economic environment is so volatile and uncertain and deposit rates are so low that most people are just plain scared of securities, especially financial securities, and the potential loss of wealth they threaten. Thus, investors today would rather keep their monies in cash or cash-like vehicles, even if these are returning abysmally low rates historically.

This was especially true in August 2011, when there was a huge surge in the purchase of ten-year Treasury notes that locked in rates of around 2%! In contrast, the 80-year historic average for the ten-year T-note stands at 5.5%. Most investors are in a quandary trying to figure out how to earn a decent rate of return on their investments. And thus we find gold earning 23% per year over six consecutive years. No wonder, then, that gold seems bound for even greater heights.

There are two main questions to ask. First, is this rise in gold for real or is this also a bubble waiting to burst? And second, is it still safe to enter the market when gold is more than $1,800 per ounce? To answer the first question, one needs to understand whether the world will start rebounding from the 2008 financial crisis and, if so, when?

The U.S., EU and Japan are still reeling from the crisis with no signs of relief in sight as more bad news overwhelms investor confidence almost daily. Investors are so weary from the crisis that isolated announcements of positive news send the markets soaring, only so they can be dashed a few days later with the inevitable arrival of more bad news.

This roller-coaster is taking a toll on our systems; the soaring market volatility is just one reflection of the impossibility of properly reading the current global economy. It is also a reflection of the incredible uncertainties buffeting the world today. And as these uncertainties turn to fear, investors start turning more and more toward safe havens.

With the dollar slipping from its haloed position, there is nowhere for investors to turn other than gold. In the U.S., a return to stability would require capital investments from businesses so that millions of new jobs are created. The housing market would have to return to stability, interest rates must begin rising with a serious economic expansion and consumer confidence must rise along with expansionary business capital expenditures and outlays. So we can conclude that as long as global markets remain volatile and investor fears grow, gold will also continue to increase in price. Given what is needed to turn our economy around, your guess is as good as mine about when we can expect the return to stability and a return to more sane gold prices.

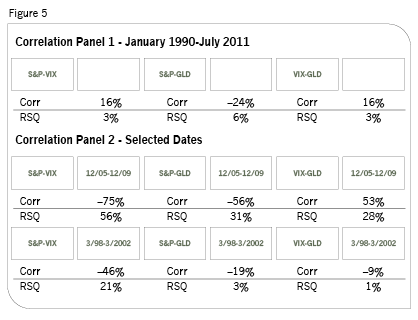

Still, from the astute investor's perspective, not all is lost. The relationships among market volatility, equity returns and gold prices (and between greed and fear) offer us an insight into the second question about whether it's safe to enter the gold market. Since market volatility increases (gauged by the VIX) will be matched by increases in gold prices and decreases in the equity indexes, then the underlying correlations could show us how we may incorporate these investment items (gold and VIX, and maybe even the dollar) into the portfolios of clients.

Before rushing into long-short and other strategic hedged positions, it is worthwhile to note the interrelationships among gold, the VIX and equities. On the surface, the VIX exhibits a surprisingly equal (15.8%) and insignificant correlation with both equities and gold for the period from 1990 to 2011. For the same period, the correlation between gold and the S&P 500 index is, as one would expect, negative (at -23%) but insignificantly so. It would seem futile to try to structure a portfolio of these components, since there would be very little diversification benefit.

But we should look closer. This period also saw the formation and crash of two significant bubbles (dot-com in 2000 and real estate in 2007). It would thus be useful to examine the significant macroeconomic events during these periods. If we construct four-year windows around March 2000 and December 2007 (the bubble peaks), a very different picture emerges. The following table shows the correlations of gold, equities and the VIX along with their respective R squared values. High values (greater than 0.3) indicate that we can reliably use the statistic for meaningful applications. (See Figure 5.)

The dot-com crash was of a much lesser magnitude than the 2008 crisis, which embroiled the entire global financial industry, not just domestic technology. And at the turn of the century, the dollar was still an attractive reserve currency. These were all good reasons that gold, the VIX and equities did not show any meaningful movements or correlations for this bubble/crash sequence.

The 2008 crisis, however, was completely different. The relationship between the VIX and the S&P 500 around 2008 is startling. Basically, the very high negative correlation indicates that increases in volatility during this period were accompanied by severe decreases in equity returns. This runs against the theory that increased risk should be accompanied by increased return.

Instead, the correlation suggests that adopting higher risk in portfolios is actually rewarded with lower equity returns! Such a condition is totally unacceptable, but nonetheless, it is the reality. It also explains the correlation between gold and equities, since the fear of losses from equity positions leads the more aggressive investors away from equities into gold. Less aggressive investors usually sell out their equity positions during market lows and place the cash in CDs, however low-yielding they may be. During the 2008 crisis, the combination of volatility and investor fear led both VIX and gold to move in the same direction.

With this knowledge, we are now in a position to weave modern portfolios more suitable for disturbing times. For portfolios that cater to long-term investment objectives (retirement, child education, estate planning, etc.) the only way to grow capital in a sustained way is, still, by keeping a significant position in equities. Such positions should be augmented by smaller long positions in both the VIX and gold, preferably with ETFs.

Any loss in the equity position will be more than compensated by the other positions. Such a portfolio would also take the guesswork out of predicting the return to stability. If and when the global economy stabilizes, equities will return to their normal job of growing capital. Positions in the VIX and gold can be easily shed. Meanwhile, the returns from such a portfolio over the next ten years will almost assuredly be higher than they would be if investors locked up their money in Treasurys, and the portfolio risk would not be much different.

Aggressive investors may also want to include a dash of the U.S. dollar in the portfolio, placing a small bet on the short/bearish dollar (ETF: UDN) whereas conservative investors may want a similar but opposite position on the long/bullish dollar (ETF: UUP). In the latter case, the return of U.S. economic stability should shore up the dollar for at least a little while.

Gold is a mirror. Its price gauges global economic fear. Fear of uncertainty, fear of losses and fear of poverty. As long as this fear remains in this world, the new gold standard will continue to reflect the fear standard. The index of fear!

Somnath Basu is a professor of finance at California Lutheran University and the director of its California Institute of Finance. Dr. Basu also serves as a professor of the Helsinki School of Economics executive MBA program. He's involved with financial planning organizations including the National Endowment for Financial Education, the CFP Board of Standards, the International CFP Board and the Financial Planning Association.