Dear Fellow Investors,

On March 10, 2000, two wonderful things happened. Tribune Corporation offered $95 cash for each share of Times Mirror Corporation and, in retrospect, the Tech Bubble burst. At the time, we had avoided technology for valuation reasons and saw value names like Times Mirror begging for shareholders. We had the feeling that the prior two years of purgatory for value investors might be ending. It was truly good news.

We have come full circle as of the morning of April 25, 2016. Our portfolio holding, Gannett (GCI), has offered $12.25 cash per share and is willing to assume the existing debt to acquire Tribune Publishing (TPUB). Other than the Chicago Tribune, the rest of the main newspapers in the deal―the Baltimore Sun, Orlando Sentinel and the LA Times―came from Times Mirror. Is there value and a future in the newspaper business in the U.S.? Can Gannett’s acquisition of Tribune Publishing and ownership of the former Times Mirror papers be good news for Gannett shareholders? Also, is there any chance that some sanity will come back in valuations of various advertising mediums, like what we had when the Tech Bubble broke in early 2000?

We believe that the newspaper business has a future because our society needs professional journalism. No other entity will cover community news, community politics, public safety, schools and local sports like the local newspaper. Our national adult population today is dominated by single folks who have yet to have children, homes and other community-oriented needs in life. Therefore, we’ve been in a down period for interest in the local news, which nobody else provides. We think time may be an ally for Gannett and creating scale before young adults get interested in your product could be a good strategy.

Gannett has publicly stated that they seek to create a nationwide network of community newspapers. They believe that cost savings and national scale will turn into a bonanza, even before circulation in print reaches its nadir and digital news finds a more maximal pricing and advertising audience. At the beginning, Gannett sees $50 million of cost savings which could be added to the $20 million of after-tax profit Tribune is anticipated to produce this year.1 In effect, Gannett will borrow the money to buy Tribune Publishing (approximately $350 million) and pay the interest out of the existing after-tax profit and free-cash-flow of Tribune Publishing. For us as shareholders, we could potentially see this acquisition raise the earnings of Gannett 20-30% immediately. The good news is, it could be more!

Secondly, Gannett has been in a declining industry the last ten years and almost nobody believes there is anything which would reverse that fact. At Smead Capital Management, we’ve found the stocks we get the most pushback on end up being some of our best performers. After all, Starbucks had no affection back in 2008’s deep recession, because “Who wants to buy a $4 cup of coffee?” Or in 2012 and today, who would want to own a bank in this horrible regulatory, slow economic growth and low interest rate environment. As Warren Buffett likes to say, “You pay a high price for a cheery consensus.” For Smead Capital Management and our clients, “Only the Lonely Can Play!”

It is possible that Gannett’s acquisition of Tribune Publishing would trigger a national discussion about the economics of advertising. Currently, advertisers have flooded internet sites with ads based on where people are spending their time. What are advertisers getting in exchange for their money from these various mediums?

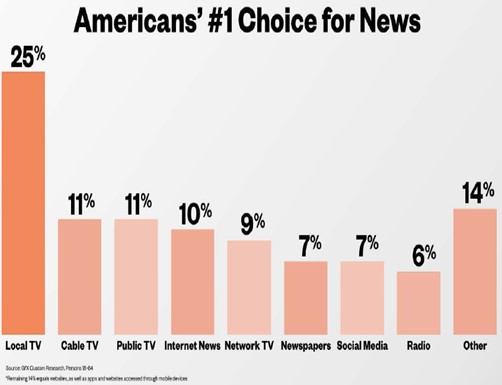

Source: TEGNA Investor Presentation 2015

The entire stock market capitalization on April 22, 2016 of U.S. broadcasters and radio stations was $40 billion. The categories of Local TV, Network TV and Radio are 40% of the audience for news on a first-choice basis. Facebook and Twitter, the two largest sources of social media news, have a market cap of $324 billion as of April 26, 20162 and were the first choice of 6% in late 2015. The entire market cap of publicly-traded newspapers is tiny compared to the broadcasters, but is still the first choice for 7% of the audience for news. At a recent media conference, a panel pointed out that old media is finite and the internet is infinite. Internet advertising is comparable to throwing spaghetti on a wall to see what sticks, but it is an infinitely long wall. If Einstein is right, it might bend back to where we started. The good news could be that the return on investment in old media is higher, while the future expectations attached to internet advertising could move dramatically lower.

An additional piece of the good news pertains to comments WPP’s Martin Sorrell made recently. He pointed out how much stickier old media advertisements are than those found in the infinite internet world.3 Ask yourself if you have a jingle stuck in your mind from a radio or TV advertisement or a visual image you saw in print. Ask yourself how often you engage a company because of an internet advertisement. Now that the pioneering tech period is coming to an end, there could be a much bigger effort to determine the return on investment for those commercials.