“All models are wrong. Some are useful.”

“All models are wrong. Some are useful.”

—George E.P. Box

As financial practitioners, we know that all models we use to analyze portfolios, retirement success probabilities and any number of other attributes important to clients have flaws. Generally, advisors try to communicate these limitations to clients, but it’s likely that most advisors sometimes gloss over those drawbacks—whether due to lack of knowledge, time or perceived client interest.

One reality: No model can predict the future. We have to make sure we don’t delude ourselves or our clients about this.

A key purpose of this article is to discuss the implications of the fact that all models have flaws in analysis, communication of results or both. The most appropriate way for a client to view progress is through the lenses of both resources and claims: The difficult part is how to work with and make use of expected future cash flows and current investment assets under conditions of uncertainty.

Increasing client longevity and developing fintech both demand and enable the continuing extension of financial planning techniques. By including the use of the Personal Funded Ratio (PFR), an advisor can broaden the range of questions addressed in client meetings, deepen a client’s understanding of how her current position relates to where she wants to be, and give greater confidence through the intersection of methodologies. Among the more important and widely used financial models is the Monte Carlo simulation (MCS) in assessing the probability of success in meeting retirement goals. Adding the PFR to the practitioner’s toolbox can help address the shortcomings of standard Monte Carlo analysis and provide a framework for more meaningful client conversations.

The PFR is a concept borrowed from the defined-benefit pension world. More discussion can be found in two articles I wrote with Sam Pittman, director of asset allocation at Russell Investments, in the February and April issues of Financial Advisor addressing the PFR and rethinking retirement liability.

Combining Future Cash Flow Apples With Investment Asset Oranges

Financial planning, no surprise, requires hard work. Clients are typically unaccustomed to creating detailed budgets and assiduously tracking their expenses. Standard financial statements can make it difficult to equate asset balances with cash flows. Cash flows themselves may have different degrees of certainty—and even discontinuities in the case of default on inflows or contingent expenses on outflows. Both MCS and PFR use expected cash flows to arrive at their respective conclusions.

More granular treatment of cash flow expectations, to a degree, can be useful in planning and creating flexibility for future action. But the old joke about economists is relevant: How do you know an economist is joking? She uses a decimal point.

MCS shows the odds of achieving financial goals assuming outflows follow an expected pattern and portfolio returns fall comfortably within historical averages; PFR has the same limitation regarding outflows, but it prices coverage of those outflows with today’s interest rates and mortality assumptions to provide a check on plan feasibility through anchoring to current conditions.

It’s part of the role of the financial professional to determine what type of information is most relevant and understandable to a client at each stage of the client’s financial life and at each reporting period.

Monte Carlo Simulation: Vulnerabilities

MCS is widely used in financial planning software. The result is often an impressive and colorful set of reports, but the output can mask a number of limitations about which the financial professional, at least, should be well aware:

• Investment returns are generally simulated over a long period of time, usually without the constraints imposed by current conditions. Long-term stock returns, including many periods beginning with much lower valuations than currently are the case, could well overstate the probability of high investment returns in the future period that’s most relevant to a particular client.

• There are many non-financial and generally uncorrelated elements of income and expense in a client’s complex life whose importance can dominate investment performance. And it’s not clear that clients will be satisfied by “pretty good odds” of avoiding retirement ruin.

• In general, clients don’t really understand probability. Googling: “Why don’t clients understand probability?” will generate more than 10 pages of response. In any event, the probability of success is likely not as relevant as the magnitude and effect of any shortfall.

• The usual expression of 1,000 or more simulations is likely to leave the client with the belief that all options are covered; the reality is we are dealing with uncertainty, not risk, and we cannot be certain which distribution of outcomes is the most valid.

• Downside risk is often understated, and the probability of success is thus overstated with MCS. For example, eMoney states: “Serial correlation is not supported in our simulation. Each year’s variable returns are totally independent from previous years.” This is the “trunk of the tree” problem; down markets can continue for several years—more than relevant to the plans and emotional responses of a client—and the serial correlation unloved by academics is all too prevalent in the investment world.

• While MCS is useful in showing the effects of portfolio choice upon probability of success, it’s a bit of the cart before the horse. Portfolio allocations should be determined based on the client’s PFR and stage of financial life. Increasing the riskiness of a portfolio is, or should be, the last lever to be pulled in attempting to improve odds of success or the next calculation of the PFR.

The Personal Funded Ratio: Features and Benefits

It’s somewhat surprising that a tool like the PFR is not widely used in financial planning. In contrast, the calculation and general reality of funded ratios drive most defined benefit plan discussions, including the politics around assumptions and funding. The observations below are all aspects of the PFR’s assumptions, methodology and benefits.

• To determine one’s PFR, all expected future cash inflows are discounted by market-available interest rate curves to reflect the riskiness of the particular cash-flow assumption. This encompasses Treasury curves for government guarantees down to “BBB” (or even lower) for increased uncertainty of payment. These present values are then added to current investment assets (“resources.”) Mortality discounts may also be used for mortality-related inflows.

• Similarly, expenses (“claims”) divided among those clients consider essential and those they consider discretionary are discounted by a combination of Treasury curves and mortality assumptions reflecting single or joint mortality. Some of the projected expenses will be actual liabilities. Some will not, which is why we call this category claims rather than liabilities (just as not all resources are actual assets—Social Security for example).

• Dividing resources by claims yields the PFR. This exercise is most directly relevant for clients with a PFR from about 90% to 130% at or close to retirement. Below 90, there is usually little the planner can do to assist the client beyond counseling reduced spending; above 130, there is not much chance the client will fail to reach his financial goals. We have found, however, that many wealthy clients, at least those with restrained spending, also find the PFR useful to understand their current capacity for fulfilling various legacy goals.

• Use of mortality discounts is a nod toward the idea that asking the right questions can trump the precision of the answers. This suffers from a defect similar to MCS in that the lack of pooling means that actual mortality can differ materially from expected mortality. One benefit of the methodology of calculation, though, is that a PFR of about 100% to 105% generally indicates that a life or joint life annuity covering claims could be purchased. The PFR is calculated very much like an actuary would price an annuity; any extra is for expense loading and profit. Given the uncertainty around expenses and contingencies, we’d not recommend this in most cases, but it does provide a fallback position.

• Because the PFR is calculated with current interest rate curves and mortality assumptions, it is grounded in appropriate beginning conditions. This can also inform portfolio construction by helping to determine the necessity to bear risk and the appropriate amount of risk to incorporate. This same feature, in periodic reporting, allows for the clear exposition of the benefits of increasing interest rates, as interim portfolio losses caused by rate increases are usually dominated by the effect of increasing discount rates on claims. The PFR’s emphasis on current conditions highlights the need to use the same methodology over time, so that reported results are actually the result of both external market changes and spending/saving patterns.

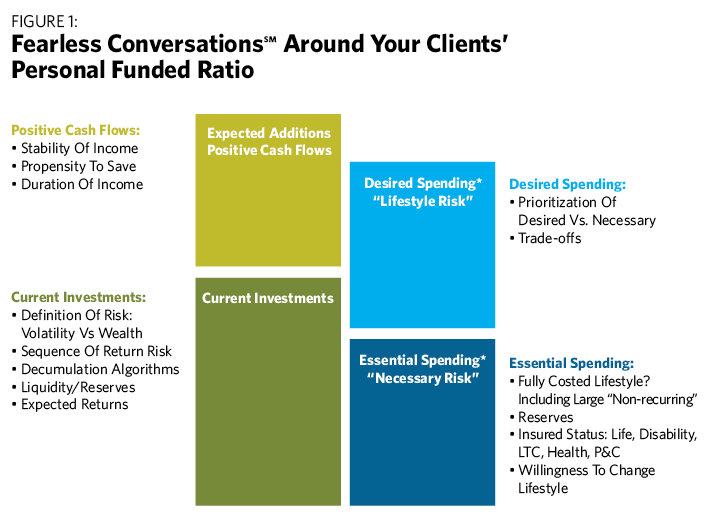

Using The PFR In Fearless Conversations With Clients

So far, we’ve briefly described two methodologies for financial modeling: MCS tries to incorporate the best current expectations of probable portfolio growth; PFR tries to incorporate current interest-rate and mortality expectations into both the feasibility of a plan and its use as a reporting mechanism. How can these work together? To answer, we’ll not spend time on the MCS output of any given reader’s chosen planning software, but rather on how two PFR elements might be used.

While PFR analysis can generate just as many colorful pages as MCS reports, a critical element for success—defined as the client’s understanding and impetus to take corrective action when needed—is to keep things simple. As well, all planning techniques may have to adapt to rapidly, perhaps discontinuously, extending life spans. This makes ongoing analysis and reporting even more important. Clarity is vital to client understanding.

A critically important component of the ongoing dialogue with clients is a deep and shared understanding of spending priorities—divided here between essential needs for daily living and lifestyle needs (or “wants.”) If spending trade-offs become necessary, the first place to look in contemplating changes is in the lifestyle space.

Thus, Figure 1 is derived from each client’s data set.

The aptness of the term “fearless” can be easily inferred from the topical choices example above: These are not often easy questions and trade-offs. They are freighted with often-conflicting emotions between spouses. Techniques for dealing with behavioral issues are far beyond the scope of this article. Suffice it to say, many of these conversations can be tough ones. But they are aided by a simple visual, easily understood, backed by as much analytical data as may be needed.

It is often said that there are four levers that can be pulled to affect the PFR: working longer, saving more, spending less and/or accepting more portfolio risk in hopes of higher returns. It is clear among upper-income quintile earners that working longer/saving more is a strong trend. But this is often not within the client’s discretion because of employment opportunities or health. If there is expected time to retirement to contribute additional savings, the effect can be powerful.