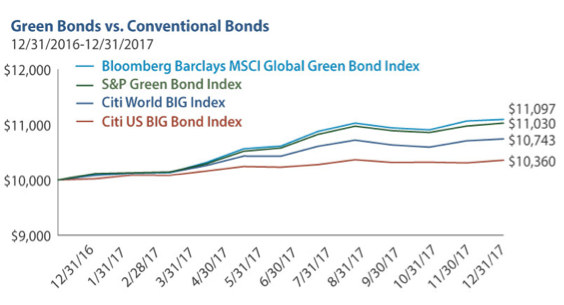

Second, academic research points to green bond investors paying higher prices than conventional bond investors. Barclays research from 2015, for example, found that green bond returns have historically tracked conventional bond returns, though green bond prices trade with statistically tighter spreads, or lower price variance. The study's authors note that if the spread divergence between green and conventional bonds continues, future green bond investors and sponsors will be forced to decide what price differential they will pay to be green (Preclaw, R and Bakshi, A, 2015).

Additional academic research found that green bond investors accept a lower yield—by as much as 0.28 percent—to pursue socially responsible investments. The study examined the prices of 92 green bonds against 258 conventional bonds over the period from November 2013 to October 2016 and found a statistically and economically significant price premium associated with investment-grade green bonds versus investment-grade conventional bonds (Aalto University School of Business Department of Finance).

Lastly, an important distinction between green bonds and high ESG ratings is paramount. Issuing a green bond does not mean that the company scores well on ESG characteristics. Some green bond issuers have strong ESG characteristics and some don’t. Again, a green bond label simply identifies that a bond’s proceeds will be applied toward environment-related projects.

The upshot is that bonds issued by companies with high ESG ratings exhibit measurable positive return characteristics, while similar return enhancements cannot yet be attributed to green bonds. While this segment of the fixed-income market is promising and growing, it does not yet have the maturity to be a properly investable asset class, particularly for nonprofessional investors. The return histories of both green bonds and the more robust ESG fixed-income universe suggest that most investors would be better off with the latter approach at least until green bonds can establish sturdier roots.

Green bonds’ intrinsic value arises from their explicit consideration of environmental impact. Not only can green bonds help investors understand how companies are prioritizing their capital allocation and operational activities, they assign great importance to issuers’ consideration of externalities, such as the risk of environmental detriment. This is an enormous departure from past practices and is worthy of acknowledgment.

Patrick Drum is securities analyst and portfolio manager at Saturna Capital. He is also a member of the United Nations Principles on Responsible Investing (UNRPI) Fixed Income Outreach Subcommittee.