If you want to know why U.S. investors are down on value stocks, just consider junk bonds.

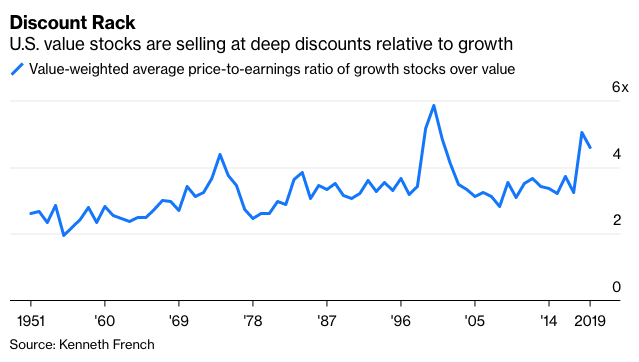

Last year was another miserable one for value investing. The Russell 1000 Growth Index outpaced the Russell 1000 Value Index by 9.8 percentage points, including dividends. It couldn’t have come at a worse time because value investors were already reeling from a multiyear drought. Growth beat value in eight of 12 years from 2007 to 2018, more than doubling the return from value during the period.

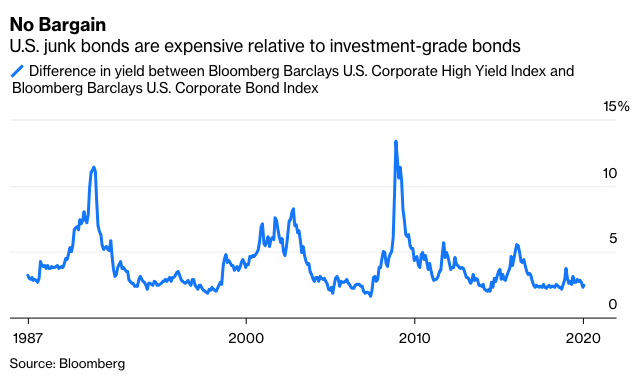

By the summer of 2019, investors began wailing about the death of value investing even as their faith in junk bonds remained unshaken. It’s a striking contrast because value stocks and junk bonds are essentially the same investment in different parts of the capital structure. Bond investors buy junk because they expect to be better compensated for lending to troubled companies than they do for stable ones, as do stock investors when choosing beaten-down value companies over those with highflying growth. Both expectations are supported by decades of data. Junk bonds have historically paid a premium over investment-grade bonds, but with more volatility. The same has been true for value versus growth stocks.

If you doubt that value and junk are two sides of the same coin, consider that companies whose bonds are in the junk bin are also likely to find their shares on the discount rack. Of the roughly 1,200 companies in the Russell 3000 Index for which a long-term credit rating from S&P Global Ratings is available, the median price-to-book ratio of firms rated junk (BB or lower) is 17% lower than that of those rated investment grade. Other valuation measures tell a similar story. The median price-to-sales ratio of companies rated junk is 63% lower, price-to-earnings is 15% lower and price-to-cash flow is 35% lower.

Companies rated junk are also bigger targets for short-sellers, or investors betting that share prices will decline, another sign that trouble tends to spread across the capital structure. The median short-interest percentage of companies rated junk, or the number of shorted shares relative to outstanding ones, is three times greater than that of firms rated investment grade.

Which raises the question: If the value premium is dead, why should the junk premium persist?

You won’t find a satisfying answer in theories about value’s purported end. The two I hear most are that the popularity of value investing killed it, mostly because of the proliferation of value funds, and that value companies can’t compete with the innovation, technology and scale of growth firms — the classic new beats old, Amazon beats Walmart, Tesla beats Ford, Netflix beats Walt Disney and so on.

But if those theories have merit—and I’ve already expressed my doubts—then junk bonds should be no more appealing. For one, junk appears to be far more popular than value. Value has rarely been as cheap relative to growth as it is today, while junk has rarely been as expensive relative to investment-grade bonds. Also, buying junk is likely to land investors in many of the mature companies that dominate value, as the overlap between value and junk shows. If anything, investors ought to be more worried about junk than value.