A direct inflation hedging portfolio should generally be designed with similar portfolio construction techniques as a broader asset allocation, adhering to the principles of diversification, risk budgeting and cross-asset correlations. An effective inflation hedging portfolio may utilize multiple asset classes in proportion to their overall expected inflation hedging characteristics, portfolio risk contributions and target returns. In general, the greater the desired certainty of inflation protection, the lower the expected return will be (and in fact will be negative for a pure inflation breakeven strategy). However, the inclusion of additional strategies that have generally good inflation hedging properties with varying risk factors, such as those studied in this analysis, can potentially mitigate the expected costs of an inflation protection strategy since these risk factors may have positive expected returns.

Conclusion

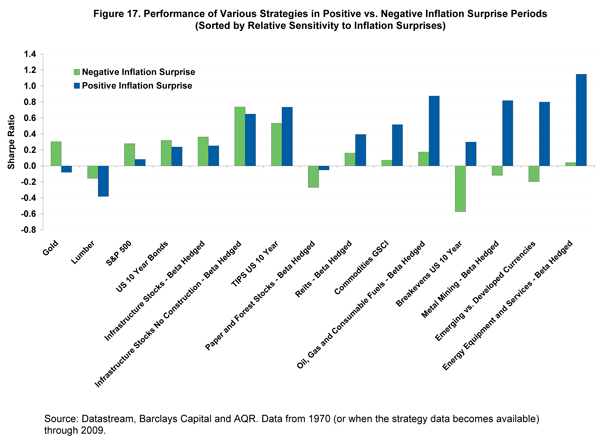

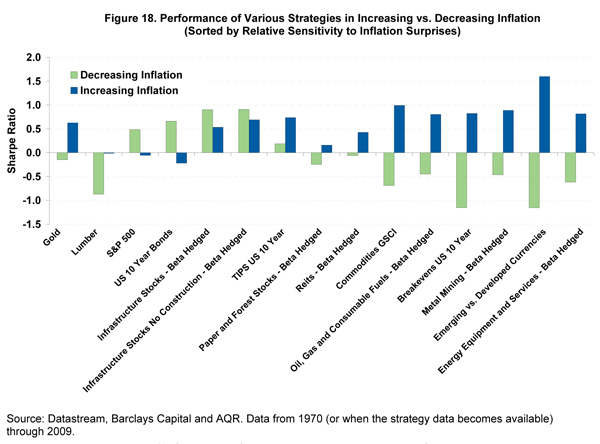

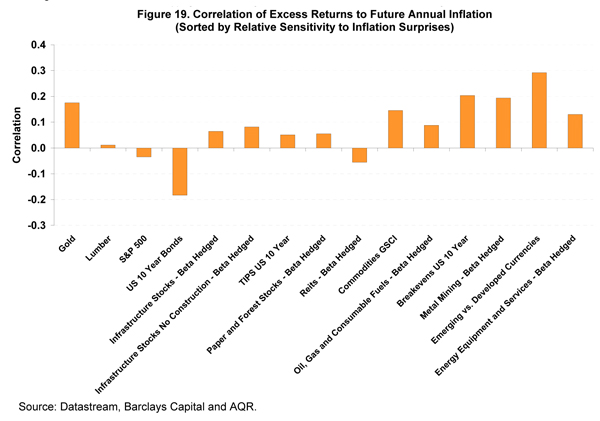

We have studied both four primary asset classes - stocks, bonds, commodities and TIPS as well as four overall asset allocations to assess their performance in inflation regimes and in response to unexpected inflation. As discussed, we believe the inclusion of asset class performance in response to unexpected inflation is more robust than simply analyzing inflation regimes, which is the traditional analysis used by practitioners to evaluate inflation sensitivity of assets and strategies. The advantage of using surprise data is that it is has multiple observations available for each inflation and growth scenario and that it directly measures the main aspect of inflation that requires hedging (unexpected inflation). We have also studied other liquid strategies for investors seeking pure exposure to inflation protection without altering their core strategic asset allocations.

Our results have shown that stocks are far from an effective short- or medium- term inflation hedge. Government bonds also tend to suffer in periods of increasing inflation. However, commodities and TIPS benefited during periods of increasing inflation. Perhaps the most interesting result of our analysis is the performance of the equal risk-weighted portfolio which performed better on average and is less dramatically affected by each individual inflation and growth scenario. Since the equal-risk weighted allocation has exposure to each asset in proportion to its contribution to overall risk, the portfolio represents less of a "bet" on the future direction of inflation and growth and should theoretically serve investors well both on average and in each potential economic environment. This is not to suggest that the equal-risk weighted portfolio across equity, government bonds, inflation-linked bonds and commodities is the optimal portfolio as indeed we believe it is possible to build more efficient portfolios with the inclusion of additional assets and strategies; the equal-risk weighted methodology across the four core assets serves to simply illustrate the comparative benefits of diversifying across asset classes to prepare for differing potential economic environments. Moreover, the higher relative performance historically of the equal-risk weighted portfolio in positive inflation surprise periods (Figure 14) suggest that it may over-emphasize inflation protection unless investors attribute a higher probability of positive versus negative inflation surprises.

We show multiple liquid strategies with strong inflation hedging properties. However, as we have pointed out, asset prices adjust to unexpected inflation and changes in inflation expectations. Because investors are forward looking, inflation expectations may change early in an inflationary cycle. Therefore, an investor who tries to time the purchase of inflation protection may fail to realize the value of the asset's hedging properties if its price has already begun to adjust. This argument favors a long-term strategic allocation which prepares for various economic environments including the possibility of higher inflation or, at the very least, a tactical strategy which acts before the market begins to price in changing expectations or increasing inflation uncertainty.

Disclaimers:

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of AQR Capital Management, LLC its affiliates, or its employees.

The information set forth herein has been obtained or derived from sources believed by author to be reliable. However, the author does not make any representation or warranty, express or implied, as to the information's accuracy or completeness, nor does the author recommend that the attached information serve as the basis of any investment decision. This document has been provided to you solely for information purposes and does not constitute an offer or solicitation of an offer, or any advice or recommendation, to purchase any securities or other financial instruments, and may not be construed as such. This document is intended exclusively for the use of the person to whom it has been delivered by the author, and it is not to be reproduced or redistributed to any other person.

Diversification and inflation hedging does not eliminate the risk of experiencing investment losses. Past performance is not an indication of future performance.

There is a risk of substantial loss associated with trading commodities, futures, options, derivatives and other financial instruments. Before trading, investors should carefully consider their financial position and risk tolerance to determine if the proposed trading style is appropriate. Investors should realize that when trading futures, commodities, options, derivatives and other financial instruments one could lose the full balance of their account. It is also possible to lose more than the initial deposit when trading derivatives or using leverage. All funds committed to such a trading strategy should be purely risk capital.