Expectations are very low for this earnings season. The challenges are many, with intense cost pressures and slowing economic growth at the top of the list. The chorus of analysts and strategists calling for big cuts to estimates has gotten louder. Expect estimates to come down, but not collapse. Here we take a look at whether expectations are low enough as we preview third quarter earnings season.

Numerous Headwinds

Corporate America has a lot working against it this earnings season. These headwinds include slower economic growth, cost pressures amid high inflation, ongoing supply chain issues, geopolitical instability in Europe and Asia, and significant currency drag from a very strong U.S. dollar. None of this is new news, but it has brought expectations for third quarter earnings growth down by nearly 7% to achievable levels in the 2% range [Figure 1].

That level of earnings growth isn’t very exciting, but thanks largely to the energy sector’s likely more than doubling of earnings on higher oil and gas prices, overall earnings are still likely to grow. The energy sector is expected to add more than six percentage points to overall S&P 500 earnings per share growth for the quarter. That means that the other 10 S&P sectors will likely see an earnings decline even if numbers come in better than expected, as they almost always do. With expectations so low coming into this reporting season, markets could get a boost if earnings were just flat without energy.

There Are Some Positives

While the pundits are mostly focused on what can go wrong this earnings season, there are several reasons to expect the numbers for this quarter to be decent. First, companies typically generate about three percentage points of upside, even in challenging profit environments, as they bring expectations down low enough to beat them. During the worst of the Financial Crisis (Q3 2008 through Q1 2009), more than 50% of S&P 500 companies hit their earnings targets each quarter. And during the first quarter of 2020, which included the sudden and unprecedented lockdown of the U.S. economy in mid-March, 62% of S&P 500 companies beat estimates, and aggregate earnings were within one percentage point of expectations.

In addition, it appears that economic activity picked up in the third quarter. After GDP contracted in the first two quarters, GDP growth may approach its pre-pandemic 2% trend for the third quarter—consensus forecasts tracked by Bloomberg call for 1.8%, while the Atlanta Fed’s real-time GDP “nowcast” is tracking to a solid 2.9%.

Finally, generating earnings growth in a tough economic environment is a little easier when inflation is the source of the weakness. The consensus estimate for year-over-year revenue growth for the S&P 500 in the third quarter is 8.5%. Higher prices mean more revenue for companies. Results from companies that are able to maintain pricing power and pass higher costs along to their customers are likely to be well received.

Here’s What’s Worrisome

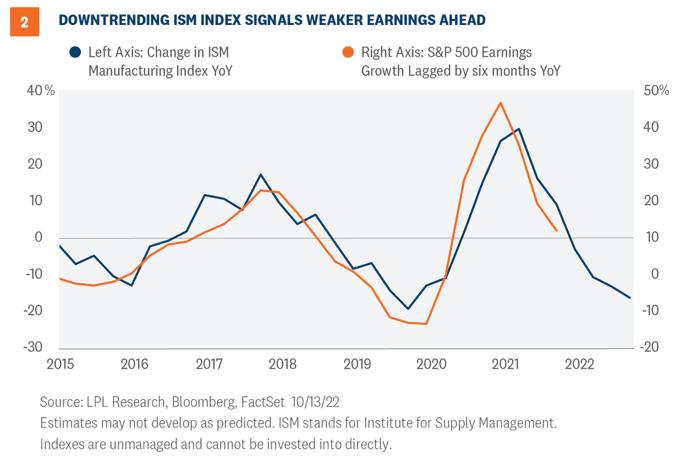

With many corporate executives preparing for recession as the odds have increased, it’s prudent to look at potential downside. One way to assess downside is to look at the historical relationship between the Institute for Supply Management (ISM) Manufacturing Index and earnings growth. The S&P 500 is more manufacturing-heavy than the U.S. economy, as measured by gross domestic product, so the ISM index tends to have some predictive power when it comes to earnings.

As shown in Figure 2, the direction of this index is pointing to a potential double-digit decline in earnings per share over the next six to 12 months. That is more pessimistic than our current house view, but it is certainly possible. That level of earnings weakness, which would put S&P 500 earnings per share in the $200 to $205 range next year, would align with historical earnings declines during the inflation driven recessions of the 1970s.