Love him or loathe him, Donald Trump is the president come January 20. That’s yuge for the affluent and their advisors when you layer in the GOP’s control of Congress. The most successful Americans would benefit handsomely under either Trump’s tax proposals or those promulgated by House Republicans in their “Better Way” tax-reform blueprint pushed last summer.

Individual Income Tax Proposals

Tax Bracket Opportunities And Anomalies

“For advisors, the biggest opportunity is starting the conversation with a client or prospective client,” says CPA-planner Greg Lane, a principal at WellFit Financial P.C., in Phoenix. “These proposals are of interest to people, they’ll want customized advice, and that’s how advisors provide value. We’re customizers,” Lane says.

But advising about taxes can be “like advising about the capital markets. One of the biggest struggles is to help clients make decisions based on logic versus emotion,” says Moss Adams’ National Tax Director Gary Stirbis, in Tacoma, Wash. “Clients may try to rush through transactions based on a potential change.”

Making sure clients sit tight right now is important because at this juncture, no one really knows what changes could occur. Part of the problem is that on the campaign trail, Trump’s contradictory remarks launched the greatest search for hidden meaning since the Beatles released Sgt. Pepper. Post-election, the inconsistencies have continued apace.

So we can’t know whether to take seriously what Steve Mnuchin, the Goldman Sachs alum picked for Treasury secretary, told CNBC on November 30. “Any tax cuts for the upper class will be offset by less deductions that pay for it. There will be no absolute tax cut for the upper class,” he said. That certainly doesn’t square with the promise on his would-be boss’s website that “every income group receives a tax cut.” Nor does it toe the line of the GOP blueprint.

Which raises another question. Which plan will be the starting point for legislation, Trump’s or the Republican party’s? Technically, tax legislation comes from the House of Representatives.

From a planning perspective, it’s important to know when these new tax laws might actually take effect. It could be soon given how, even before taking office, Trump racked up an impressive set of accomplishments, from saving American jobs (and simultaneously cutting corporate taxes!) to reaching out abroad.

Then again, moving a once-in-a-lifetime tax-reform bill through both chambers of Congress could prove to be a long slog. If a law isn’t enacted until autumn, “at that point it may be likely to take effect in 2018,” says Mark Luscombe, a federal tax analyst at Wolters Kluwer Tax & Accounting, an information company in Riverwoods, Ill.

Of graver concern for planners is the possibility that new legislation could self-terminate after 10 years. Remember the 2001 tax act? If Republicans lack the 60 Senate votes needed to avoid a Democratic filibuster, they would have to pass a budget reconciliation bill with at least 51 votes. Such a bill must expire after a decade if, like the 2001 law and the Trump plan, it’s projected to have a negative impact on government revenues beyond then. As for the GOP blueprint, “according to its authors [it] is largely revenue neutral using dynamic scoring,” an Ernst & Young report says.

Both the presidential and congressional plans would axe numerous items from the Internal Revenue Code, including the notorious alternative minimum tax. Abolishing the AMT would aid clients with incentive stock options, says Boston CPA Michael Antonelli, a partner at Edelstein & Company LLP. Exercising these options triggers AMT consequences that can prove disastrous if the stock’s value subsequently drops. “Eliminating the AMT would allow holders of incentive stock options to exercise them and start the holding period for long-term capital gains treatment without fear of being hit with a large AMT bill,” Antonelli says.

Repealing Obamacare’s 3.8% net investment income tax, as both plans intend, would ease planning for many clients. For those in real estate, a common strategy for avoiding this tax is to try to qualify as a real estate professional. But in audits, the IRS often challenges taxpayers’ documentation of their time spent in real estate-related activities, according to Moss Adams’ Stirbis. “Therefore, to avoid having to defend it, some clients choose not to be treated as a real estate professional.” Instead, they suffer the surtax. If the tax were killed, that would extinguish this planning conundrum, Stirbis says.

Deductions are on the chopping block, too. The GOP blueprint jettisons all itemized deductions except mortgage interest and charitable contributions. Trump wants to cap itemizations at $200,000 for joint filers and $100,000 for singles. These approaches to deduction reduction are different from what the current law follows. It phases out itemized deductions based on the client’s adjusted gross income, starting at $313,800 for joint filers in 2017 and $261,500 for single clients.

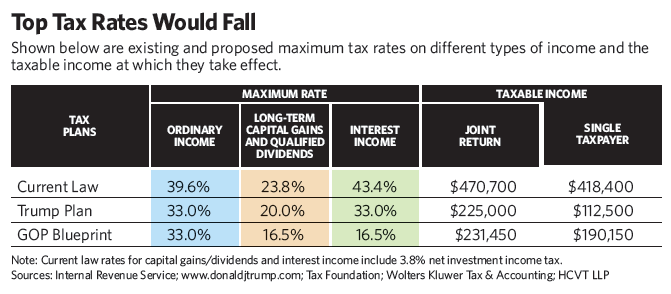

Clients with the highest incomes would benefit under both sets of proposals. For example, the top ordinary bracket’s slide of more than 6 percentage points, from the current 39.6% to 33%, would make Roth conversions less costly. So more clients might convert those accounts, Stirbis says.

Although it hasn’t received much publicity, the GOP blueprint proposes to tax interest income preferentially, the way long-term gains and dividends are.

Meanwhile, under the new president’s proposed structure, a few clients would actually pay higher rates. “That’s the sneaky part of Trump’s plan. Taxpayers jump up to the maximum rates more quickly than in the current system,” says Blake E. Christian, a CPA and tax partner at HCVT LLP, in Park City, Utah.

Make Taxes Great Again

January 2017

« Previous Article

| Next Article »

Login in order to post a comment