Controlling the supply of dollars was assigned to the Federal Reserve System in 1913; the Fed is charged with maintaining stable prices and a vibrant economy. In the 99 years of the Fed's existence, based on the government-maintained Consumer Price Index (CPI), the buying power of a dollar has shrunk by 3.23% per year.

That means that the current buying power of a 1913-dollar is only 4.3 cents! Said another way, a basket of consumer goods and services that cost $100 when the Fed first came into existence would cost $2,300 today because of the gradual erosion of the purchasing power of the dollar! This is why we believe retirees need a game plan for offsetting inflation with investment gains.

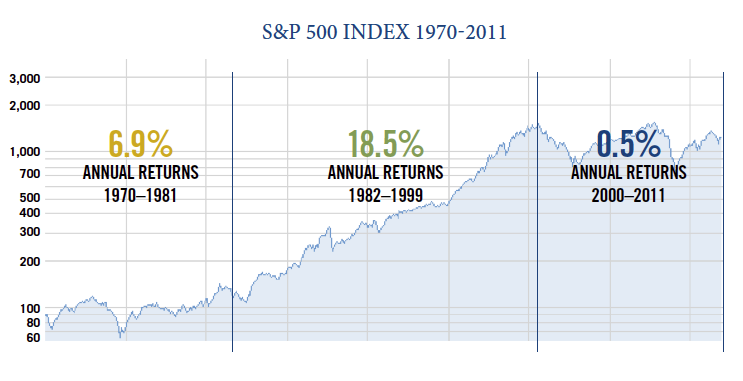

In the four most recent calendar years, CPI inflation has averaged just 1.8% a year in the United States. Some commentators have suggested that this indicates a reduction of the long-term inflation risk. We do not share that opinion. As a matter of fact, we think that longer-term inflation risk (the debasement of paper currencies throughout the world) has increased since the 2008-09 "credit crisis" because central banks around the world have dramatically expanded the money supply in a misguided and failed effort to "stimulate" economic activity.

What central banks have done is facilitate an unprecedented increase in the burden of sovereign debt on the private economy, thus increasing governments' motivation to devise inflationary monetary policies around the world.

The speed at which available dollars circulate through the system (velocity) has dropped to historic lows since the residential real estate bust; this has muffled the impact of loose monetary policies on the general level of prices. When velocity begins to revert to its historic mean, as most financial data series eventually do, we believe inflation will move higher. This is surely the will and intent of the powers that be.

But it's important to note that the modern credit boom could end, instead, in widespread defaults and a massive credit contraction. If that should be our lot, the world would probably experience deflation (falling price levels), not inflation. Our position is that a wave of modest deflation could surface temporarily in a recession as excess inventories clear ... but that political forces are clearly arrayed on the side of inflation; the ultimate risk here, of course, is that their efforts get out of hand and produce hyperinflation. This is a very serious investment issue; to remain watchful and adaptable will be critical ... for businesses and for investors.

FAI Discipline For Managing Inflation Risk

1) Invest in businesses with above-average pricing power due to competitive advantages and/or because their products or services are essential. (Adaptive companies should also be able to cope with deflation if that develops.)

2) Invest in "Hard Assets" that tend to rise in price during periods of rising inflation. Our positions include gold bullion and gold mining, energy pipelines, timberland and politically-secure oil and gas reserves.

3) In our fixed-income portfolios:

a) Emphasize shorter maturities that can roll into higher-yielding replacements as interest rates rise

b) Make use of adjustable rate securities such as TIPS and Bank Loans

ISSUER RISK

From time to time, any company can become the subject of news, opinion or rumors that might influence the market value of its securities, for good or for ill. A headline could be about the company itself, about an aspect of the economy that affects its business outlook, about developments at a competitor, and so forth.