Common Cold

The five economies that came to define Europe’s most troubled economies—Portugal, Italy, Ireland, Greece and Spain—vary significantly in terms of core sectors that drive their economies. The largest company by market cap in Ireland is CRH (a construction supplier); in Spain it’s Santander (a global bank); in Greece it’s Coca-Cola HBC (a bottler that relisted in London last year to minimize its home country stigma).

But these economies do share three common ailments. One, they all got drunk on instant cheap money that came with euro zone membership. The profligate Greeks and Italians were able to borrow at close to the same rates as highly disciplined Germans.

Two, peripheral economies and the ECB lacked the regulatory discipline and oversight to identify and respond to excesses fueled by access to cheap money. And three, domestic and foreign investors (being short-term profit focused) failed to note rising systemic risks.

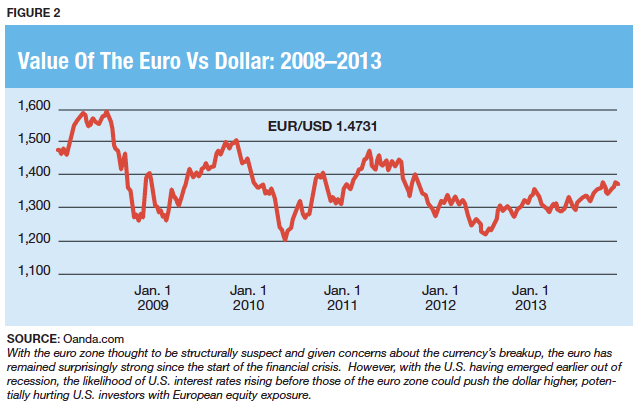

In early March 2014, Spain, Italy and Ireland 10-year sovereign yields were within 200 basis points of German bunds, reviving the question: Is risk again not being accurately assessed today among the euro zone’s diverse economies?

Not an issue to Barry Norris, portfolio manager of the London-based Argonaut European Alpha fund with £255 million in assets, which has been averaging gains of more than 13% a year since starting up in 2005. He sees opportunities across Southern Europe over the next several years because of the significant gap he sees between near-term consensus market earnings and what he expects will be made as economies emerge from recession.

Accordingly, he has boosted the fund’s exposure to the region from nil as of the end of 2012 to 30% in February with positions in leading regional banks and industries.

“This is not much different from what was happening in the emerging markets in the late 1990s,” explains Norris, “when we saw the collapse in growth and corporate profits and deep cost cuts. A key difference: Southern Europe has had to do this not through the currency devaluation but through the devaluation of labor and production costs.” He sees the region as more competitive and ripe for earning surprises, far more so than Germany and Switzerland, whose exposure he has ratcheted back from 60% as of the end of 2013 to just 12% this past February.

However, the more skeptical Andrew Parry, chief executive officer of Hermes Sourcecap, a £1.7 billion high-alpha European strategy, isn’t quite so sanguine. In labeling the current rally as a “rush for trash,” he thinks investors may be “forgetting the lessons of the past and failing to ensure these cheap companies have the fundamental strength to keep delivering the goods over various economic cycles.”

To Parry, absolute values are now looking quite high, so investors will have to be selective because he doesn’t think the recovery will float all boats. Specifically, he needs to see evidence of earnings power that justifies the re-ratings and higher prices.

If Parry is right, then advisors who may opt for simple, easy exposure through ETF country funds may find more risk in such broad diversification than through selective exposures to sound companies with proven management and healthy sales diversification.

More Than Lipstick?

June 2, 2014

« Previous Article

| Next Article »

Login in order to post a comment