"On the eve of the signing of the Revenue Act of 1951, which lifted the top marginal rate to 91% from 84.4%, George B. Haynes of Evanston, Ill., wrote a letter to the editor of Barron's excoriating the Truman administration. 'I am a bear on America for at least the next 10 years,' Haynes declared. 'The financial ignorance and recklessness of Congress and the administration, the willingness to sacrifice the country to continue the Democratic Party in power, the enormous Federal debt, the high taxes, the readiness to give billions of taxpayers' money to foreign countries can have, in my opinion, but one result, i.e., the worst collapse this country has ever experienced, though I do not know when'."

- Jim Grant, Grant's Interest Rate Observer

I revisit Jim Grant's elegant prose this morning due to overwhelming requests to put in writing what I said in my verbal strategy comments recently. Manifestly, the country has been going to "hell in a hand basket" for years, but the question is-when will it get there? This year, investors' moods have been particularly dour as most missed the bottoming process of October 2008 through March 2009 and only began to tiptoe back into equities late last year. That strategy left participants pretty disgruntled as Mr. Market has violently see-sawed his way through 2010 with the result being no upside progress. Combine that with a vicious political environment, and a decelerating economic backdrop, and is it any wonder investors don't want to hear about stocks? In fact, it has not been since the end of 1974 I can recall investors being so unwilling to discuss equities!

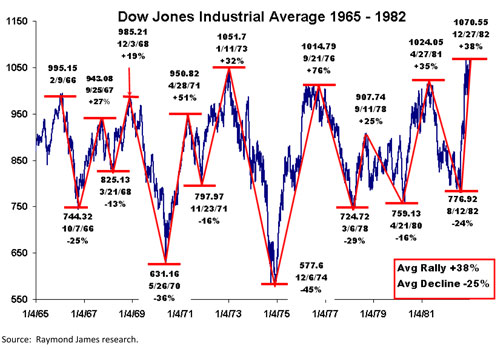

In December of 1974 the D-J Industrial Average (DJIA/10447.93) was changing hands at 577.60. That price-point turned out to be THE nominal "price low" for the senior index. Nevertheless, the DJIA remained mired in the same trading range it had been in since 1966 for another eight years. Interestingly, while the "price low" occurred in December of 1974, the "valuation low" did not arrive until 1982 with the DJIA trading below book value, a P/E ratio around 7x, a dividend yield of 6%+, and an earnings yield (earnings ÷ price) approaching 14%. Importantly, however, the December 1974 "price low" of 577.60 was never violated, as can be seen in the nearby chart. Readers may recall that following the Dow Theory "sell signal" of September 1999 I suggested the Dow might be in for a similar pattern to that of the 1966 - 1982 experience. I still feel that way; and so far it's been a pretty good "call." If that déjà vu script continues to play, I think that while the DJIA made its current-cycle nominal "price low" in March 2009 (at 6547.05), the "valuation low" won't happen any time soon.

Accordingly, burned by a manic Mr. Market since 2000, investors have been checking out of the stock market, as from 2007 - 2009 U.S. investors took more money out of stock mutual funds than they put in, the first such three-year skein since the 1979 - 1981 bottoming process. Indeed, faith in equities has all but been lost with investors on track to pull more money out of stocks in 2010 than in any year since the 1980s with the exception of the 2008 "financial melt-down."

As my friend Craig Drill, eponymous captain of Craig Drill Capital, writes: "Investors have continued to flee equities to embrace the (alleged) 'safe haven' of debt instruments. Although the return is low, the probability of the return of capital is high (if held to maturity) ... The S&P 600 (the small capitalization stock index) fell 10% from (its) peak in late July to August's close. At the same time, 10-year Treasury yields fell to below 2.5%; Norfolk Southern sold 100-year bonds at 5.95%; and IBM issued 3-year notes at an interest cost of 1%. (It appears) investors are willing to take duration and credit risk, but not equity risk."

To be sure, Mr. Market is a manic depressive fellow. As Warren Buffett elaborates on Benjamin Graham's famous Mr. Market analogy:

"An ever helpful fellow, Mr. Market stands ready every business day to buy or sell a vast array of securities in virtually limitless quantities at prices that he sets. He provides this service free of charge. Sometimes Mr. Market sets prices at levels where you would neither want to buy nor sell. Frequently, however, he becomes irrational. Sometimes he is optimistic and will pay far more than securities are worth. Other times he is pessimistic, offering to sell securities for considerably less than underlying value. Value investors, who buy at a discount from underlying value, are in a position to take advantage of Mr. Market's irrationality."

Clearly that is well said; and speaking to valuations, there was a terrific article on Seeking Alpha's Web site recently titled "Mr. Market's 10% Opportunity." Said article was written by Kendall J. Anderson and read: "Not all securities are being sold cheaply. But enough are that an enterprising investor can profit with the passage of time. One of the more popular measures of common stock valuation is the comparison of earnings per share with the current price of each share: what many of you know as the Price to Earnings ratio (P/E). If you just reverse the equation and divide the per share earnings by the current share price, you are given the earnings yield (E/P). The earnings yield gives you an easy way to determine how much the company earns on every dollar you pay for your shares. It also gives you an easy way to compare what your company is earning for you relative to the amount you would earn if you loaned your money at interest. Of course, the highest earnings yields for quality stocks only come about when Mr. Market is pessimistic.

Here are a few points to ponder:

Based on trailing 12-month earnings, there are 71 companies in the S&P 500 with an earnings yield greater than 10% (P/E less than 10). The range of these stocks' earnings yield is 31% to 10.05%.

Based on current fiscal year estimated earnings per share, there are 80 companies in the S&P 500 with an earnings yield greater than 10% (P/E less than 10).

Finally, based on estimated earnings over the next four quarters (12-month forward earnings estimates), there are 112 companies in the S&P 500 with an earnings yield greater than 10%.

Given the number of companies you can buy with an earnings yield of greater than 10%, you should be able to create a long-term portfolio that has a better than average probability of rewarding you with a higher return."

Using FactSet I replicated that list of stocks referenced in the first bullet point. It reads like the Who's Who of blue chip stocks and many of them possess decent dividend yields. From Raymond James' universe of companies names like Allstate (ALL/$29.42/Strong Buy) and Chevron (CVX/$78.00/Strong Buy) made the grade. The list can be retrieved by contacting the Retail Liaison office - ([email protected]).

In conclusion, I leave you with yet another "hell in a hand basket" quip, from a 1991 edition of Time Magazine:

"The US economy remains almost comatose. The slump already ranks as the longest period of sustained weakness since the Depression. The economy is staggering under many 'structural' burdens, as opposed to familiar 'cyclical' problems. The structural faults represent once-in-a-lifetime dislocations that will take years to work out. Among them: the job drought, the debt hangover, the banking collapse, the real estate depression, the health-care cost explosion, and the runaway federal deficit."

The call for this week: There have been two 90% Upside Days in the past few weeks combined with new highs in Lowry's Buying Power Index and new reaction lows in the Selling Pressure Index. Ladies and Gentlemen, since 1940 there has never been an instance when such a configuration existed five months into a bear trend; and note that we are now five months from the April highs. Additionally, over the last 16 mid-term elections the stock market has never made a new reaction low post election day. This week I will be watching the Labor Day indicator. If over the next four days stocks rally, the odds the rally will continue are high. If stocks fall, history suggests caution into October is warranted.