The independent broker-dealer space has all the elements of a high-adventure video game this year, and only the most advanced players may be up for the challenge.

Anticipating and navigating regulations is growing more daunting while shrewder strategies are needed to prevent profits from imploding under mounting costs. B-Ds must also have quicker reflexes to gobble up and retain financial advisors who can help score revenues for the firms.

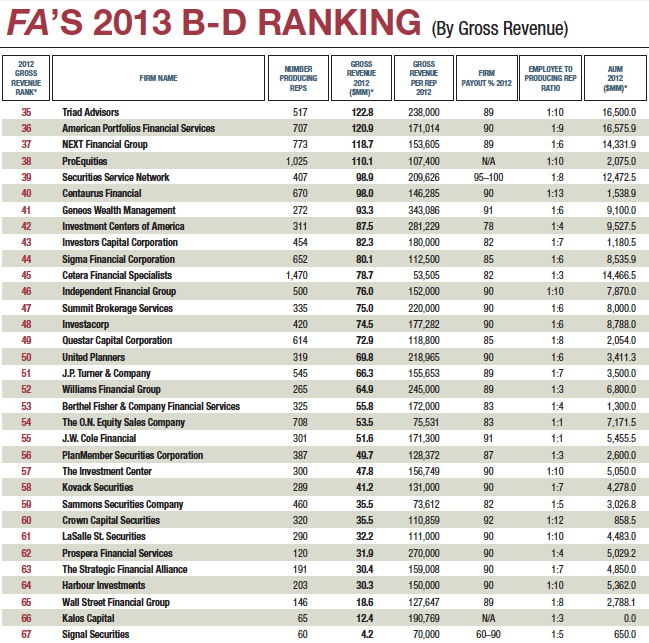

Click here to view the pdf of the survey.

Fewer independent B-Ds are present for this latest round. Finra counted 4,289 member firms in December 2012, versus 4,456 in 2011. Larry Papike, president of Cross-Search, a Jamul, Calif.-based independent B-D advisor and executive placement firm, expects more smaller firms to seek exit strategies and alliances amid rising compliance costs, an aging advisor population and stiffening competition to attract younger advisors. “I think consolidation is inevitable,” he says.

Independent B-Ds are trying to squeeze out net profit margins in the 5% to 8% range, says Papike. If new regulations require firms to add technology and compliance people, they will likely have to eat these costs because it’s hard to cut advisors’ pay without losing them, says Jodie Papike, an executive vice president at Cross-Search. The majority of firms are providing advisors with 85% to 91% payouts, according to Financial Advisor’s 2013 B-D Ranking survey.

For their part, larger independent firms are working harder to revamp their tool kits in an effort to woo and retain advisors in the increasingly competitive market. New offerings include a greater choice of practice channels, stepped-up training and technology, and more assistance in succession planning efforts for those advisors approaching the “game over” stage.

The Financial Services Institute, a Washington, D.C.-based trade group representing independent financial services firms and independent financial advisors, is pushing for adoption of federal legislation that will allow independent B-Ds to classify registered representatives as independent contractors. Another top priority for the group this year is opposing the U.S. Department of Labor’s proposal to expand the definition of fiduciary. FSI says this would eliminate advisors’ ability to be compensated through commissions on retirement advice they provide to IRA holders and participants in ERISA-covered plans.

FSI also filed comment in early March on a proposed rule by Finra that would require advisors to disclose their recruitment compensation to clients. And the institute has expressed concern that the SEC backs a floating net asset value for money market funds. FSI says this would boost tax and record-keeping burdens and could alienate Main Street investors.

Dave Bellaire, general counsel of FSI, is trying to be positive. “The pace of regulatory change and the uncertainty created by Washington, D.C.’s inability to tackle the fiscal challenges facing our country are just some of the issues that make it a difficult time,” he says. “However, there are also great opportunities as investors need financial advice, products and services from a local financial advisor they trust more than ever.”

Chet Helck, executive vice president of Raymond James Financial Inc. and CEO of its Global Private Client Group, which includes its B-D businesses, says his firm always operates at a fiduciary standard, so he doesn’t expect that would be so different. What does trouble him is how the rule may be reproposed. “There are all sorts of moving parts to that story,” he says.

Helck, chairman of the Securities Industry and Financial Markets Association (Sifma), says he is also concerned that no attempt has been made to coordinate Labor Department and SEC rule-making. “It’s very complex to build a different structure for clients with money in multiple buckets governed by different rules,” he says.

Raymond James Financial Services (RJFS) is the company’s broker-dealer unit supporting independent financial advisors, more than 3,200 nationwide. It tries to avoid classification issues by reporting to the Internal Revenue Service the earnings of all its affiliated independent contractors for any activity that flows through the firm. “The general topic concerns us, but we have a certain level of comfort from our talks with FSI and Sifma,” says Scott Curtis, the president of RJFS.

Raymond James has had to spend a lot of money on hiring people and creating new systems in order to comply with regulations. The company has also invested heavily in technology to improve client services and operating efficiencies. “Over the past couple of years, we’ve almost doubled our technology spend from around $110 million a year to well over $200 million,” says Helck. More revenues are needed to absorb rising costs—which is why he says recruiting and acquiring advisors has been so important for the firm.

The 2012 acquisition of Morgan Keegan added 900 advisors to Raymond James & Associates, the traditional employee B-D subsidiary. Morgan Keegan has helped the firm expand into new markets and become a leader in the fixed-income markets after the big banks, says Helck.

Curtis says RJFS has seen 14.5% year-over-year growth in client assets under administration—from $143.6 billion in 2011 to $164.4 billion in 2012. He says the growth has come from existing advisor affiliates growing their practices, but also from the company’s strong advisor retention and its new advisor affiliations. RJFS has also benefited from favorable equity and bond markets. “Interest, traffic and conversations continue to be strong,” he says.

Rebranding and integration were the two overriding goals at Cetera Financial Group, which changed the name of Multi-Financial Securities to Cetera Advisors and rechristened its recently acquired Genworth brokerage firm, which caters to CPAs, as Cetera Financial Specialists. According to Valerie Brown, CEO of the Cetera network, Cetera Advisors enjoyed a record year, with fee and commission revenue exceeding $250 million. Cetera advisors also saw a surge in attractting new advisors.

“The overarching theme at Cetera is that one size doesn’t fit all,” Brown says. “The regulatory environment is getting more expensive while the cost of technology keeps rising.”

Changing Channels

Hybrid models—which enable advisors to be dually registered as RIAs with the SEC and as brokers with Finra—have been around for years. But more frequently, the best advisors jump ship for dedicated RIA firms. Now B-Ds are starting to become more hybrid-friendly to be more competitive and flexible in the fee space, says Jodie Papike. More firms are offering multiple channels to accommodate advisors who have their own RIA firm, who want to establish one or who prefer to use a corporate RIA.

Starting in the second quarter of 2013, advisors with Waltham, Mass.-based Commonwealth Financial Network will be able to drop their Finra registration and either use Commonwealth’s corporate RIA or operate exclusively as their own RIA. Or they can remain dually registered with or without their own RIA.

Joni Youngwirth, a managing principal and head of practice management at the firm, says the firm is responding to advisor demand with the new RIA options.

Last year, the channel of dually registered advisors captured the largest growth in both assets and advisors, according to Boston-based research firm Cerulli Associates. “It was initially thought of as a stopover, but more firms are choosing this as permanent,” says Tyler Cloherty, associate director of research with Cerulli.

For the better part of a decade, LPL Financial has operated a custodial platform for advisors who don’t want to retain their securities license, though it has only promoted the unit since 2008. But the giant brokerage’s hybrid platform is still driving much of its growth and the combined RIA/custodial platform had $42 billion in assets at year-end.

Among them is Sun Group Wealth Partners of Irvine, Calif., a hybrid RIA with approximately $160 million in assets under management and is affiliated with LPL, which had 13,336 advisors at the end of 2012. “The cost of doing business is increasing, so we think it’s very important to be aligned with a firm with deep pockets and results,” says Winnie Sun, a founding partner of Sun Group and a former broker with Morgan Stanley Smith Barney. “LPL is there from a regulatory and cost standpoint to support our business so we can build relationships.”

She says the affiliation also gives her clients, primarily self-made, high-net-worth individuals from Generations X and Y, a feeling of stability. Particularly helpful has been the support LPL provides in her expanding efforts to communicate via social media with clients and prospects.

Robert Moore, president of advisor and institution solutions at LPL, notes that the advisor universe isn’t expanding very fast but the number of pre-retirees and retirees is. “That is a huge level of opportunity,” Moore says. “At the same time, retirees are going to need to live in an era of modest returns on traditional fixed-income investments.”

James Poer, the president of NFP Advisor Services Group, a business segment of National Financial Partners Group, says the vast majority of his firm’s 1,700 registered reps (producing plus non-producing) are dually registered and use the corporate RIA. “Once they start peeling back the onion,” he says, “a lot of advisors who think they want their own RIA hop aboard our corporate one.” Why? It enables them to shift responsibilities and focus more on clients.

A study commissioned by the firm found that advisors who use an integrated technology program to outsource their back office can generate 30% more in revenues. Poer expects to see more advisors adopt this approach.

Practice, Practice, Practice

NFP Advisor Services Group uses practice management to empower advisors, says Poer. Its business consulting team visits offices twice a year to show staff how to better leverage tools and resources.

Software upgrades are rolled out two to three times a year to deepen integration. The firm is educating and training advisors on the role they can play as client demographics shift. “Boomers are far more entrusting and empowering of FAs,” he says, “where younger ones want to be more involved in the process and decision-making.” The firm is also helping advisors expand investment offerings as money transfers between the generations.

More advisors are personally experiencing this shift. Fiscal cliff jitters helped fuel the recent flurry of activity at RJFS, which assisted with 22 practice acquisitions and succession plans involving more than $1 billion of client assets under management during its first fiscal quarter of 2013, says Curtis. But even without the cliff, B-Ds think they can add a lot of value here.

Patrick Jinks, the director of Practice Planning & Acquisitions at RJFS, says about 50% of independent advisors have business succession and continuity plans in place, while only about 24% did in 2006. The firm expanded its practice acquisitions and succession planning department last year and continues to develop ways to make it easier for buyers and sellers to meet each other. It also has a lending program to help advisors buy other practices.

To help get the next generation of advisors up to speed, Commonwealth recently launched a junior-senior mentor program in which pairs of advisors from multiple firms attend workshops. Youngwirth says it has been well-received.

She also leads a yearlong “Power in Practice” business development coaching program that has helped participating advisors outstrip non-participants in production. Topics include business plans and goals, processes and marketing. “It’s lonely out there,” she says. “This gives them focus, and they can share and compare.”

Last year, Commonwealth began making proactive outreach calls to its approximately 650 branches to increase awareness of issues, services and technology. It is starting best practices roadshows for staff that will be held in multiple cities.

Although it may be too early to call this an industry trend, Youngwirth has seen an uptick in seven-figure firms bringing in service advisors to take over existing business, paying them a salary instead of a split. These employees monitor portfolios and make recommendations but are not required to be rainmakers like lead advisors.

Training is also a big focus for Questar Capital Corp. (owned by insurer Allianz). It’s spending $1 million more on its overall training and education umbrella than it was three years ago, says Alex Barned, chief distribution officer. It recently added a customer relationship management system to help boost efficiency and organization. It is also gearing up for stiffer regulations, as “a lot has already begun to get baked in,” he says.

Barned says 2012 was Questar’s best recruiting year ever in terms of the number of representatives and the verifiable gross dealer concessions. Its 2013 recruiting goal is 20% more verifiable GDC. The firm recently hired three additional field personnel to assist with recruiting, training and coaching. “[But] you cannot have head count for the sake of head count,” says Barned, who notes it must be a cultural and business fit. Questar assumes that 3% to 4% economic growth is probably “the new normal” and is modeling everything appropriately, he says.

Cambridge Investment Research Inc. of Fairfield, Iowa, didn’t realize until the Labor Department rolled out its retirement plan disclosure rules last summer that most of its advisors who manage a retirement plan have multiple participants. Approximately half of Cambridge’s 2,200-plus advisors are the primary rep on a retirement plan account, and more than 100 advisors manage more than 20 plans. “It was a lot of work,” says first executive vice president and chief marketing officer Jim Guy. Fortunately, the firm’s retirement center, launched in early 2010, was able to help its compliance team communicate the regulatory developments.

This year, Cambridge is introducing a branch-focused practice management program to help advisors who want to build or grow a branch. “Ten, 15, 20 years ago, people didn’t want to be part of a branch, but now they do,” says Guy, because regulations have gotten more complicated.

Being privately owned has given Cambridge flexibility to grow and compete. “We can focus on what advisors need. If they say ‘I need x,’ we don’t have to ask the Street for permission,” says Guy. “Of course, it has to make sense.”

Cambridge has greatly expanded its alternative products offerings, and many of its advisors are using them. But the firm maintains a guideline that no more than 10% of a client’s investable assets may be allocated to alternatives because of liquidity issues.

Other firms are also doing more to protect client investments. Raymond James is educating advisors about finding the right proportion and duration of fixed income and encourages them to explain to clients how a “flight to safety” can be risky if interest rates rise, Helck says.

Sun, who advocates diversified portfolios and long-term investing, is pushing clients to do dollar cost averaging. She is also trying to quietly handle regulatory complexities without burdening clients. “There is so much political noise and stuff going on that clients have enough stress,” she says. “My job is to make them invest even when they’re scared.”